The Property and Casualty Insurance (P&C) industry is facing pricing softness but is expected to benefit from prudent underwriting and increased digitalization. Key players such as RenaissanceRe (RNR), Axis Capital Holding (AXS), First American Financial (FAF), Mercury General (MCY), and Palomar Holdings (PLMR) are projected to grow despite challenges, with the policy renewal rate anticipated to accelerate due to an active catastrophe environment. According to Swiss Re, insured losses from natural catastrophes reached approximately $107 billion in 2025, impacting underwriting profitability.

The Federal Reserve has been reducing interest rates, influencing investment income positively despite presenting headwinds. The combined ratio for the industry is estimated to deteriorate slightly to 99% in 2026, while global premiums in the sector could grow nearly sixfold to $722 billion by 2030, driven primarily by regions like China and North America. In 2025, the global commercial insurance rates experienced a decline of 4%, marking continued competitive pressures.

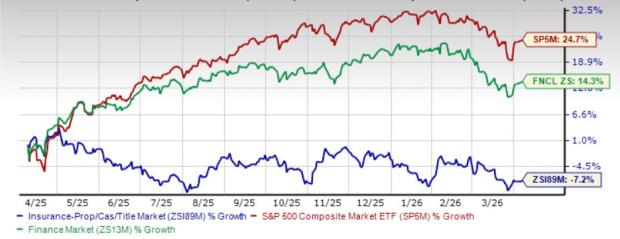

The Zacks Property and Casualty Insurance industry ranks #41 out of over 250 sectors, indicating favorable earnings outlooks, with 2026 earnings estimates trending upward. However, the industry has underperformed the broader market, with a 7.2% decline in the past year compared to a 14.3% gain in the finance sector. Currently, the industry is trading at a trailing price-to-book ratio of 1.4X, significantly lower than the S&P 500’s 7.75X.