The energy industry is poised for significant growth as electricity demand is expected to rise, driven by the electrification of the transportation sector and AI data centers. This surge will favor companies involved in the production, transportation, and distribution of natural gas. Master limited partnerships (MLPs), trading at lower valuations than pipeline corporations, offer higher yields and total return potential.

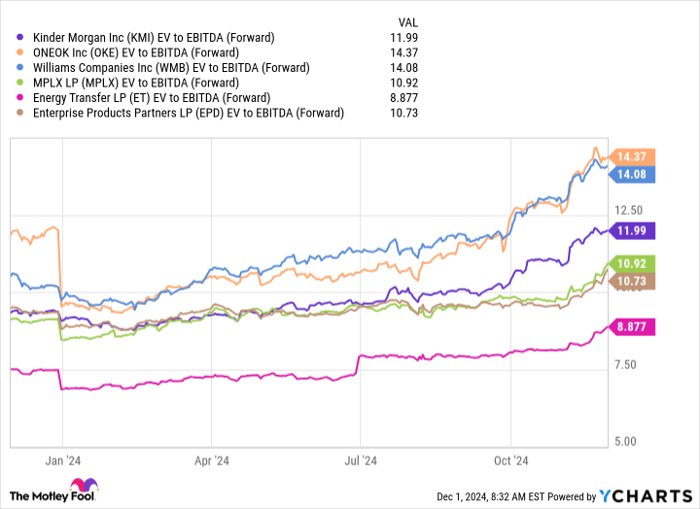

Leading pipeline companies like Kinder Morgan, Oneok, and Williams have seen their shares increase by over 60% in the past year. In contrast, MLPs such as Enterprise Products Partners (NYSE: EPD) and Energy Transfer (NYSE: ET) have grown between 30% and 40%. Current distribution yields for these MLPs exceed 6%, significantly more than the 3% to 4% offered by corporate peers. For instance, a $1,000 investment in an MLP could yield over $60 annually, compared to $30-$40 from a pipeline corporation.

Enterprise Products Partners has $6.9 billion in major projects underway, including natural gas processing plants set to support cash flow growth through 2026. MLPs are expected to continue attracting investment due to their strong growth prospects and attractive tax advantages, despite the complexity of their tax documentation, which includes a Schedule K-1 form.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.