The Overlooked Gem in Consumer Stocks

As an investor, it’s natural to feel anxious about consumer stocks, with their fierce competition and narrow margins. However, a closer look at Tractor Supply Company reveals a rural gem in the consumer industry – an underappreciated long-term dividend growth stock that mirrors the growth in America’s private consumption.

The resilience and unique profile of Tractor Supply Company make it a compelling investment opportunity, and recent economic developments only serve to strengthen this conviction.

The Power Of The Rural Consumer

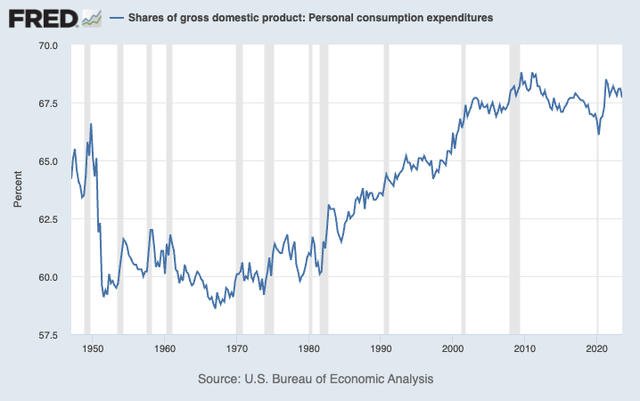

Tractor Supply Company, often likened to a rural mini-Home Depot, caters to the specific needs of the rural consumer, reflecting a robust 68% contribution of private consumption to America’s GDP. Its strategic presence in smaller towns and focus on outdoor lifestyles position it as a strong contender in the consumer market.

- Size: Unlike the expansive Home Depot stores, Tractor Supply Company’s smaller, specialized stores cater to the rural consumer.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

|

Livestock and Pet |

5,984 | 47.0 % | 7,102 | 50.0 % |

|

Seasonal, Gift, and Toy |

2,674 | 21.0 % | 2,983 | 21.0 % |

|

Hardware, Tools and Truck |

2,674 | 21.0 % | 2,699 | 19.0 % |

|

Clothing and Footwear |

1,018 | 8.0 % | 994 | 7.0 % |

|

Agriculture |

382 | 3.0 % | 426 | 3.0 % |

- Locations: With its presence in smaller towns and rural areas, Tractor Supply Company strategically serves the needs of a diverse customer base.

Tractor Supply’s focus on the rural consumer and its diverse product segment align with the evolving landscape of private consumption, making it a resilient and appealing investment opportunity.

Furthermore, the company’s strategic approach to targeting suburban, exurban, and rural areas reflects its acute understanding of the evolving consumer landscape.

Tractor Supply Company Shows Strong Economic Resilience

Akin to an oasis in an economic desert, Tractor Supply Company (TSCO) stands resilient against market headwinds, touting its unique business model as inimitable armor. As other businesses grapple with interest rate and price sensitivities, TSCO graciously remains immune. The company’s unwavering stance in the outdoor living and animal care sector has stood firm, even during the tumultuous financial crisis of 2007-2009, as customers clung fervently to their passion for the outdoor lifestyle.

Despite the capricious whims of weather, TSCO’s microeconomic forte brings stability that few other businesses boast. Thriving amid the elements, be it blistering heat, bone-dry drought, or relentless rainfall, TSCO stands resolutely impervious, a companion to livestock and friend to all who cherish the “Out Here” experience.

Solid Dividend Growth and Steady Financial Position

Exemplifying its economic mettle, TSCO recently raised its dividend by a formidable 12% on February 8, 2023. The company currently pays $1.03 per share per quarter, yielding an impressive 1.8%, towering above the S&P 500 yield by a commanding 40 basis points. TSCO’s five-year dividend Compound Annual Growth Rate (CAGR) of 28%, amplified by the pandemic, further underlines its exceptional financial fortitude.

With an anticipated $10.39 in earnings per share (EPS) this year, TSCO’s low payout ratio of 40% stands as a testament to its prudent financial management. Shielding its dividend with a robust balance sheet, the company projects a net leverage ratio of 0.8x EBITDA, safeguarded by an investment-grade credit rating of BBB.

Strategic Buybacks and Market Outperformance

Edging ahead of market competition, TSCO has implemented aggressive stock buybacks, swallowing more than a fifth of its shares in a decade. Combining this tenacious strategy with steadfast dividend growth, the company has triumphantly outpaced the market, delivering a whopping 230% in returns over the past ten years.

Paving The Road For Prolonged Growth

Battling against market headwinds, TSCO reported a slight blip in its third-quarter comparable sales, dampened by a diminutive 0.4% contraction. Despite this, the company achieved an 11% surge in diluted earnings per share, cementing its stature in the economic arena.

Enduring unfavorable weather conditions, TSCO’s sales performance weathered the storm, persevering through bouts of extreme heat, drought, and relentless rainfall, which chipped away at sales expectations.

In the face of macroeconomic shifts, TSCO anticipates maintaining flat comparable store sales for the full year of 2023, underscoring its resilience amid economic turbulence.

To sow the seeds for prolonged growth, more than 35% of TSCO’s stores have adopted the Project Fusion layout, with over 420 Garden Centers undergoing an active transformation. The ongoing acquisition of Orscheln Farm and Home fortifies the company’s footing in the Midwest, casting a wider net over a customer base synonymous with TSCO’s product offerings.

The company’s enterprising spirit is further embodied in its strategic real estate endeavors, opening 51 new stores, engaging in successful sale-leaseback transactions, and preserving a robust pipeline for future store openings. The company’s shrewd use of sale-leaseback deals stands as a testament to its efficient growth strategy, freeing up cash without straining its balance sheet.

Tractor Supply Co: A Promising Investment Opportunity in 2024

Tractor Supply Co is revving up its engines, leaving investors eager to jump on board the fast lane to financial gains. Recent strategic moves and growth initiatives by the rural lifestyle retailer signal a promising investment opportunity, with its unique market positioning and resilient performance displaying an uncanny ability to navigate economic downturns while sustaining above-average returns.

Growth Initiatives

Tractor Supply Co’s drive for growth has found an emphatic ally in its Neighbor’s Club loyalty program, which boasts a massive 32 million-strong membership base, representing a staggering 77% of sales. This loyalty powerhouse is set to fuel the company’s growth further, fostering improved customer retention and loyalty, signaling an exciting trajectory for potential expansion and enhanced patronage.

Beyond mere customer retention, the company is focused on enhancing customer satisfaction through last-mile deliveries, leveraging third-party services and in-house delivery teams. Additionally, the emphasis on bulk delivery options serves customers requiring larger quantities of products for their ranches or properties, further solidifying the company’s commitment to convenience and customer-centric services.

Furthermore, the company’s concerted efforts to expand its distribution network and implement AI-driven solutions exemplify a progressive approach to enhancing operational functionalities, seeking to fortify margins and optimize its supply chain, ensuring a robust framework to support future growth with a harmonious synergy between same-store sales, new stores, and e-commerce.

Valuation

Analysts are aligning their outlook with the company’s ambitious growth plans, projecting a 4% EPS growth in 2023, followed by a 3% spike in 2024, which would be tempered by slow economic growth. However, the outlook brightens for 2025 and 2026, with anticipated double-digit EPS growth.

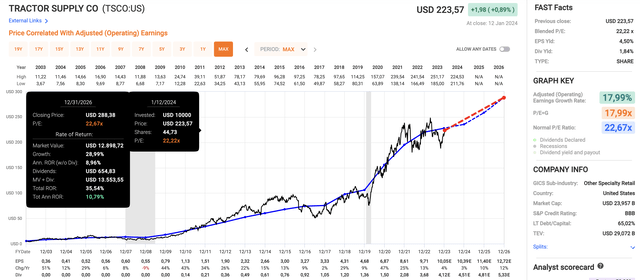

- TSCO currently trades at a blended P/E ratio of 22.2x.

- Its normalized valuation stands at 22.7x earnings per share.

According to these figures, the company charts a course for annual returns of 10%-11%, including dividends, with a remarkable historical return of 21.4% per year since 2003. This trajectory positions TSCO as a compelling investment prospect, especially poised to capitalize on economic growth and a resurgence in consumer sentiment, warranting a closer watch or even augmentation to one’s investment portfolio.

Takeaway

In a sector dominated by mainstream consumer-focused corporations, Tractor Supply Co distinguishes itself by catering to the rural market—often overlooked and underserved. With strategically located smaller stores appealing to outdoor-living enthusiasts and animal owners, TSCO has cultivated a fiercely loyal customer base that resiliently weathers economic storms.

Moreover, the company’s strategic initiatives, such as the Neighbor’s Club loyalty program and advancements in supply chain management, underscore its unwavering dedication to customer satisfaction and future growth, accentuating its status as a standout contender for a core position in investment portfolios seeking sustained, above-average returns in 2024 and beyond.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.