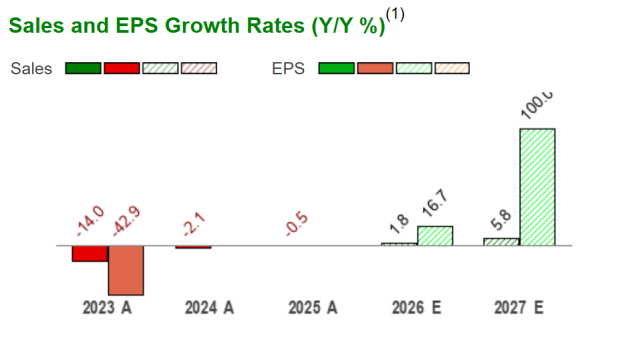

Q4 Earnings Exceed Expectations

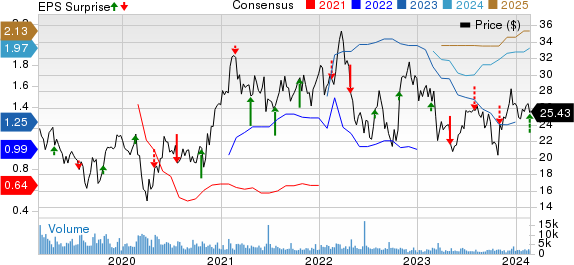

Trinity Industries, Inc. (TRN) has showcased a remarkable performance in the fourth quarter of 2023. The company reported earnings per share (EPS) of 82 cents, surpassing the Zacks Consensus Estimate of 66 cents by a notable margin. Notably, this figure reflects an impressive 86.3% increase compared to the previous year.

Impressive Revenue Growth

The triumph continued with total revenues amounting to $797.9 million, outperforming the Zacks Consensus Estimate of $779.3 million. This indicated a substantial growth of 34.9% year over year. Trinity’s top line was buoyed by higher external deliveries and favorable pricing in the Rail Products Group, reinforcing its market presence and operational efficiency in a competitive landscape.

Strengthened Operating Profit

Trinity also witnessed a commendable growth in its operating profit, which reached $148.7 million, reflecting a 31% jump over the previous year. This impressive feat was primarily supported by increased external deliveries in the Rail Products Group. It’s worth noting that this growth was partially offset by lower lease portfolio sales volume, indicating the company’s adaptability in managing dynamic market conditions.

Segmental Performance Highlights

Notable segmental performances include the Railcar Leasing and Management Services Group, which saw revenues of $221.6 million, registering a strong 12.2% increase year over year. The Rail Products Group also demonstrated resilience with revenues of $674 million, marking a 2.8% growth Y/Y. Favorable pricing and operational efficiencies contributed to the group’s solid results.

Financial Outlook and Shareholder Remuneration

Looking ahead, TRN expects an EPS range of $1.30-$1.50 for 2024, excluding items beyond its core operations. Additionally, in 2023, the company generated $309 million in net cash from operating activities and returned $86 million to its shareholders, reflecting a commitment to creating long-term value.

Peer Performance Comparison

Comparing Trinity’s exceptional performance to peers in the transportation sector, we observe varying results. While some companies like J.B. Hunt Transport Services, Inc. faced challenges with declining EPS, Trinity’s robust growth trajectory sets it apart in the industry.

Future Prospects

Trinity’s consistent growth trajectory, operational excellence, and robust financial outlook position it as a formidable player in the transportation industry. The company’s strategic focus on enhancing shareholder value, coupled with resilient business operations, bodes well for its future performance.

Get a slice of the Trinity triumph, a tale of resilience, adaptability, and growth in a dynamic market landscape.