A Bump in the Road

Truist Financial Corp. (NYSE:TFC) witnessed a sharp sell-off following the collapse of SVB Financial Group (OTC:SIVBQ) in March 2023. While concern about the significant unrealized losses in Truist’s held-to-maturity (HTM) portfolio was rife, subsequent rebounds and impressive Q4 performance failed to sway my decision to part with TFC stock, as I shared in my December follow-up.

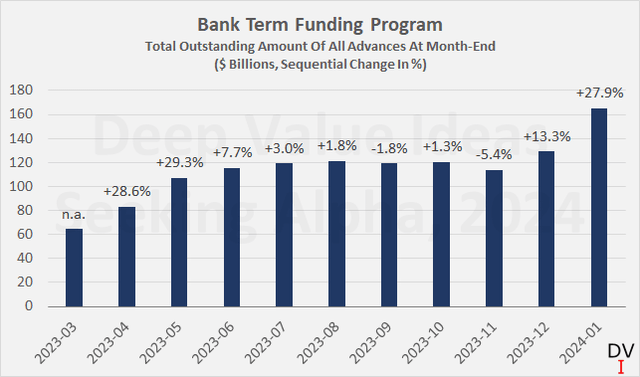

As an avid observer of U.S. banks, I closely monitor the Federal Reserve’s Bank Term Funding Program (BTFP) – a measure announced in response to the March 2023 banking crisis. The BTFP’s utilization is of paramount interest to me for two key reasons.

Firstly, the Federal Reserve is set to halt loans under the program on March 11, 2024, leaving banks reliant on borrowing from the Discount Window. Secondly, the BTFP’s usage serves as an indicator of bank stress, particularly for banks facing disproportionately high unrealized losses in their HTM portfolios. Consequently, the recent surge in emergency liquidity provided under the BTFP hasn’t dented my confidence despite Truist’s likely perpetually elevated unrealized losses.

The recent surge in emergency liquidity provided under the BTFP hasn’t dented my confidence despite Truist’s likely perpetually elevated unrealized losses.

The Weight of Unrealized Losses

Upon unveiling its results for Q4 and full year 2023 on January 18, 2024, Truist Financial announced a goodwill impairment charge of $6.1 billion. This non-cash write-down was primarily attributed to interest rate-related changes in asset valuation discount rates, with additional impetus from potentially unrealizable synergies between BB&T and SunTrust – a result of their late 2019 merger.

The impairment had been expected to drive a decline in Truist’s equity ratio, thereby inflating relative equity-related unrealized HTM losses. However, the impairment did not actually impact Truist’s equity ratio, which stood at 11.1% as of December 31, 2023, owing to more notable changes in other asset and liability accounts.

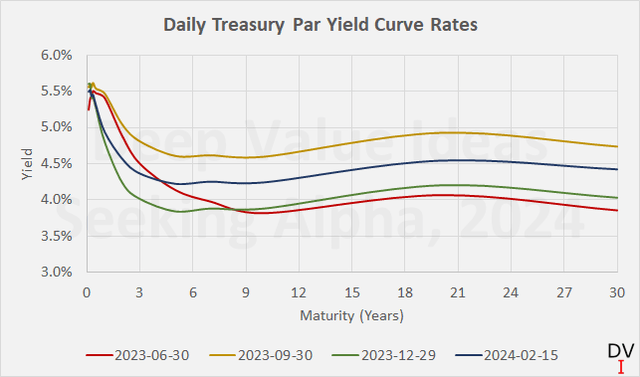

As of the close of Q3 2023, Truist’s relative unrealized losses had surged, primarily due to higher long-term interest rates. Given the subsequent significant decline in long-term interest rates by year-end, the pending release of Truist’s upcoming 10-K filing is anticipated to reflect a drop in unrealized losses. Nonetheless, notwithstanding this decline, the existing unrealized losses are expected to still represent over a third of tangible book value.

With Truist’s HTM losses remaining at elevated levels, concerns may arise regarding the risk of bank collapse triggered by widespread bank runs, especially with the sunset of the BTFP facility looming. However, I argue that this is more of a theoretical risk.

The Federal Reserve’s swift response during the March 2023 crisis, coupled with well-collateralized emergency liquidity loans through the BTFP, managed to boost depositor confidence, mitigating the risk of widespread bank runs. Notably, Truist, being one of the largest banks in the U.S., sits at 8th position in terms of consolidated assets – a factor that may lead depositors to regard it as “too big to fail”.

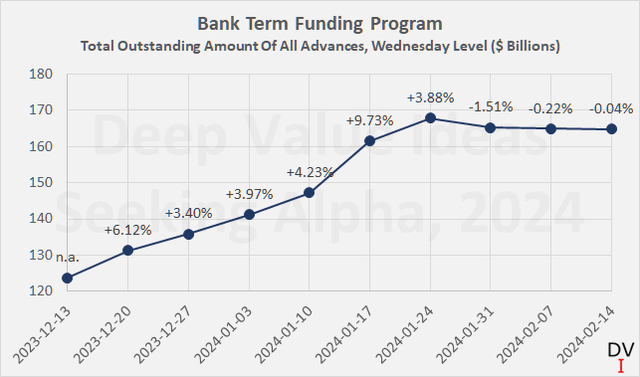

Therefore, the recent surge in BTFP utilization, characterized by a new all-time high, is no cause for concern. In fact, it’s likely that Truist even profited from the process.

The Banking Arbitrage Opportunity: An In-Depth Analysis

The Spike in BTFP “Emergency” Lending

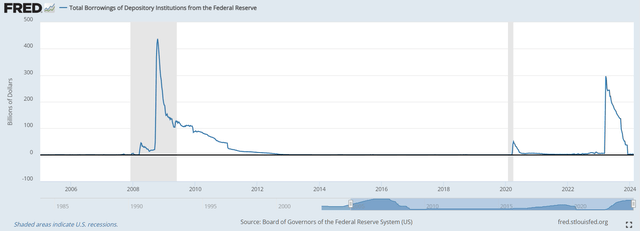

Banks often turn to the Federal Reserve to borrow through the Discount Window to meet short-term liquidity needs. This Practice aids depository institutions manage liquidity risks efficiently while protecting their customers from any negative consequences, such as withdrawing credit during stressful market periods.

The graph illustrating depository institutions’ total borrowings from the Federal Reserve, notably excluding advances under the BTFP, portrays the utilization of this important and effective policy tool.

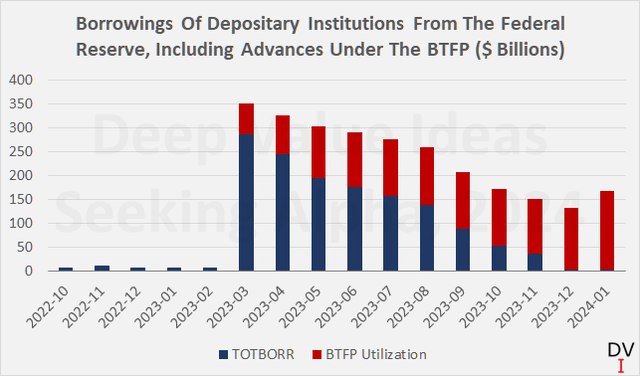

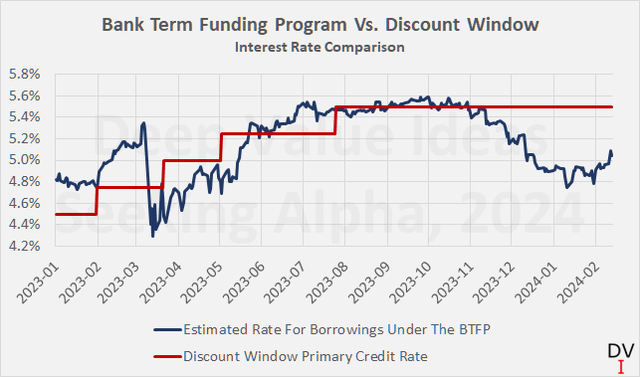

However, the recent sharp increase in BTFP utilization, in contrast to the almost unused Discount Window, initially seems perplexing. However, delving deeper into the interest rate for borrowings under the Bank Term Funding Program uncovers an interesting development.

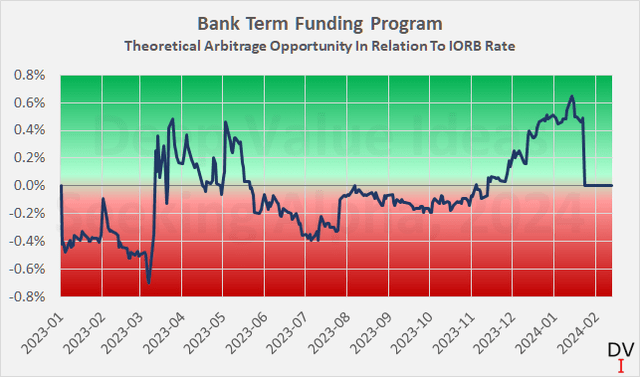

Following a significant decline in the interest rate for borrowings under the Bank Term Funding Program since November 2023, it is evident that short-term loans under the BTFP have become markedly cheaper than under the Discount Window. This development has led to an intriguing arbitrage opportunity for banks.

It appears that banks have grasped the opportunity to borrow inexpensively from the Federal Reserve under the BTFP and generate risk-free profits by re-depositing the proceeds with the same institution. However, this opportunity was short-lived, as policymakers swiftly responded by announcing an interest rate floor at the prevailing IORB rate. This move was a clear acknowledgment of the use of the BTFP facility for arbitrage purposes.

Upon careful consideration, it is clear that the recent spike in BTFP utilization is not indicative of a banking crisis resurgence but rather a result of banks seizing an arbitrage opportunity. The subsequent decline in the drawdown of the program following the Federal Reserve’s rate floor announcement further supports this hypothesis.

Quantifying Truist’s Potential Arbitrage Profit

At the end of the fourth quarter of 2023, Truist had approximately $54 billion (book value/amortized cost) of HTM assets on its balance sheet. Estimating the potential arbitrage profit for Truist involves considering the book value as a proxy of the potential loanable volume. However, given that the Fed reported only about $169 billion in related collateral, TFC’s responsibility for almost a third of the volume seems unreasonable.

Consequently, the potential arbitrage profit for Truist has been calculated, assuming it had borrowed an amount equal to a certain percentage of the book value of its HTM assets for the maximum one-year period allowed.

Assessing Truist’s Financial Maneuvering and Market Impact

Truist appears to have taken advantage of a situation, pulling a financial rabbit out of its metaphorical hat, which could potentially lead to significant profits. Analysis suggests that by allocating only a percentage of its high-quality liquid assets as collateral, the financial corporation could have reaped a profit ranging from $35 million to $352 million. This maneuver was facilitated through the Bank Term Funding Program (BTFP) without incurring fees.

Notably, such potential arbitrage profit, while substantial at first glance, would only amount to a fraction of Truist’s 2023 net interest income, ranging from 0.24% to 2.37%. These figures, even at their highest, underscore the modest impact relative to the corporation’s overall income. In comparison, U.S. Bancorp could have generated profits between $55 million and $550 million, representing approximately 0.3% to 3.1% of the bank’s net interest income in 2023.

Implications for Truist Financial and Market Reflections

In light of its financial strategy and market dynamics, Truist Financial also reported a goodwill impairment of $6.1 billion. The impairment, largely due to interest rate-related changes and potential unrealizable synergies between BB&T and SunTrust, did not affect the bank’s tangible equity ratio. This impairment, being non-cash, does raise important questions about the corporation’s financial decisions and impact.

Unrealized losses as of December 31, 2023, appear to have decreased in the wake of lower long-term interest rates. However, elevated interest rates continue to pose significant challenges, potentially amounting to around 34% of Truist’s tangible book value. Despite modest shifts in the fair value of Truist’s HTM assets, the noteworthy increase in the Federal Reserve’s Bank Term Funding Program raises eyebrows and market reflections.

A closer look at the Bank Term Funding Program, its interest rate, and comparison with the IORB rate, indicates potential arbitrage opportunities. Truist seems to have utilized this opportunity to garner a risk-free profit from around mid-November 2023. The Federal Reserve’s decision to peg the BTFP rate at the IORB rate, following this realization, led to a prompt decline in outstanding borrowings. This shift in the financial landscape, despite the temporary nature of the opportunity, has left a distinct imprint on market behavior.

The decline in borrowings after the announcement reaffirmed that the increase was due to an arbitrage opportunity, rather than indicating a resurgence of market stress. Despite this acknowledgment, the BTFP balance is expected to diminish slowly due to the extended term of the borrowings. Such market oscillations reflect Truist’s financial maneuvers and their ripple effects.

In essence, Truist’s financial strategy and the consequential market reflections, albeit fascinating, prompt a reexamination of the corporation’s risk management and financial prudence. As the market absorbs these events and recalibrates its expectations, the longer-term impact on Truist’s and broader market performance remains a key area of focus.

Thank you for taking the time to read through my latest assessment. Your insights and perspectives are always appreciated. Whether in agreement or divergence from my conclusions, I eagerly anticipate your engagement in the comments section. Your feedback is invaluable in shaping future discussions on this subject. Remember, this analysis serves as a starting point for your own financial due diligence, allowing you to form a well-rounded perspective on the matter at hand.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.