Trump’s Tariff Strategy: Implications for the U.S. Economy and Markets

As of today, here’s the current landscape regarding tariffs…

- Last week, President Trump enacted a 25% tariff on all cars and light-duty trucks imported into the United States.

- The President had previously implemented a 20% tax on all Chinese imports.

- The administration has indicated plans to extend the 25% tariffs on beer imports and empty aluminum cans alongside derivative aluminum products.

At this moment, President Trump has unveiled the specifics of his reciprocal tariff strategy. We are working swiftly to provide you with today’s insights, so here’s a concise overview of our findings.

First, Trump confirmed that the 25% tariff on non-U.S. made vehicles will take effect tomorrow.

Additionally, Trump mentioned that his administration would implement a “discounted reciprocal tariff.” This approach involves assessing the total foreign tariffs on U.S. goods, along with indirect financial pressures such as currency manipulation and trade barriers. The U.S. will then impose a reciprocal tariff set at half of that total amount, which Trump has termed “kind” reciprocal.

Furthermore, Trump specified a minimum baseline tariff of 10% applicable to all countries.

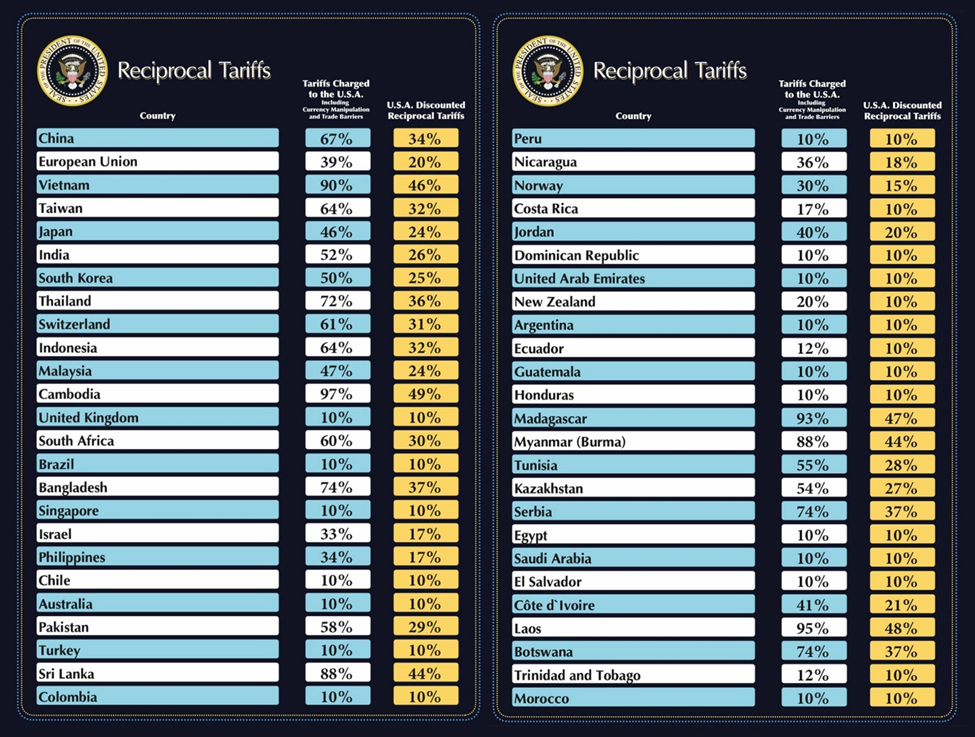

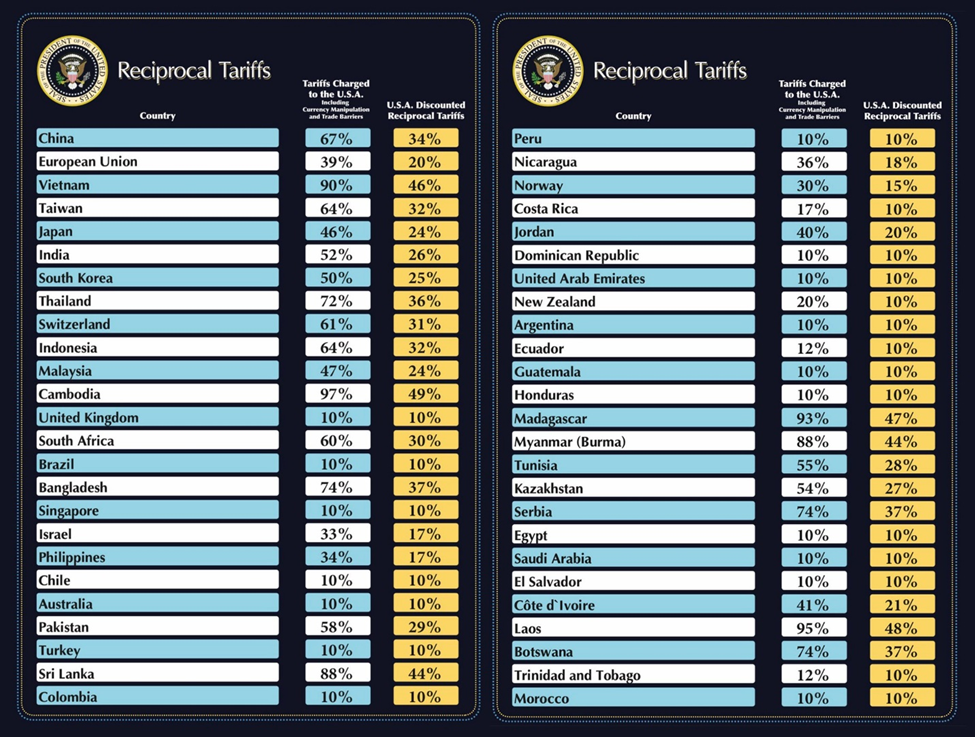

Here’s the “Liberation Day Reciprocal Tariffs” list from The White House:

Source: White House data

After outlining the country-specific tariffs, Trump emphasized his overarching goal with the statement:

If you want your tariff rate to be 0%, build your product here in America.

What Comes Next?

Here’s what Luke Lango, our hypergrowth expert, projected earlier this week in his Innovation Investor Daily Notes:

We anticipate that, despite the current aggressive and confrontational discourse, parties will seek to negotiate new trade agreements in April.

The tense communication is likely to pave the way for resolutions — with the U.S., Canada, the EU, and others expected to engage and finalize multiple trade agreements in the near future.

As a result, we believe these tariffs may last only a few weeks, leading to a resolution of the current tariff tensions by late April.

Once the dust settles, we expect to see an uptick in market performance.

This market downturn is driven more by anxiety than reality; if the anticipated worst-case scenarios do not materialize, market fears will subside, allowing for a rebound in equities.

Trump’s recent announcement presents various facets worthy of analysis. We will provide further insights and recommended actions from our experts in the days ahead.

As I write this, stock futures are significantly down, with the Nasdaq dropping over 2%.

Stay tuned for more updates.

Assessing Recession Risks

This Monday, both Goldman Sachs and Moody’s Analytics increased their recession probabilities.

Goldman now estimates a 35% likelihood of recession, up from 20%. Moody’s assessment rose from 15% at the beginning of the year to 40%.

In comparison, the Atlanta Fed’s GDPNow tool predicts a 3.7% economic contraction in the first quarter.

How concerning is this situation?

Let’s consult legendary investor Louis Navellier, editor of Growth Investor:

The Atlanta Fed’s forecast indicates a potential contraction in the U.S. economy for the first quarter, which has unsettled Wall Street.

A significant factor behind this negative GDP growth forecast is the growing trade deficit, resulting primarily from the influx of imported goods and increased gold inventories.

This trade deficit is now contributing an alarming 4% reduction to first-quarter GDP growth. In essence, barring the trade deficit, the U.S. economy is still on a growth path.

I must also share that no economic indicators currently point toward a recession.

Both Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell have recently asserted that the U.S. economy remains “healthy.”

Additionally, Louis highlights encouraging economic reports, such as a notable increase in existing home sales.

He points out that the Trump administration is pursuing trillions in onshoring investments, which could further stimulate GDP growth.

In summary, Louis concludes:

The U.S. is not at imminent risk of entering a recession.

Opportunities in AI Stocks Amidst Market Fear

In his recent Digest, Louis expressed:

Keep in mind that market behavior can be irrational. Recent trade issues have overshadowed significant positive developments in the AI sector.

Despite robust AI earnings growth, the focus has skewed negative (primarily due to tariffs). Media coverage often amplifies these concerns, treating every setback as a major crisis.

This situation has driven many top-tier AI stocks into correction territory, resulting in an oversold market where exceptional companies like NVIDIA are now available at remarkable discounts.

To…

Natural Gas Market Shows Promise Amid Tech Stock Struggles

At present, Nvidia (NVDA) has seen a decline of 27% from its peak in January. The broader trend is evident as the “Magnificent 7” stocks, which represent a gauge of major tech leadership in artificial intelligence (AI), have now officially entered a bear market.

Source: Koyfin

The downturn has prompted some market analysts to sarcastically rename these stocks from the “Mag 7s” to the “Lag 7s.” In this climate, Louis, along with global macro strategist Eric Fry and tech expert Luke Lango, encourages investors to view this downturn as an opportunity to invest in the future leaders of AI.

This message holds added significance as technology, particularly AI, continues to exacerbate the wealth gap in the country.

A Strategic Approach to Investing in AI

Last week, Louis, Eric, and Luke shared a strategic framework on how to best invest in AI during what they term “The Technochasm.” This phenomenon refers to the growing wealth divide spurred by advancements in technology and AI.

The presentation offered three key steps investors should consider now to stay ahead in this increasingly fragmented tech landscape, along with a selection of top-tier AI stocks.

Referencing past advice, Luke noted:

In 2020, we identified the Technochasm. Following our guidance, investors had substantial gains, including approximately 1,350% from Freeport-McMoRan Inc. (FCX) over 11 months, nearly 1,000% gain from Nvidia (NVDA), and over 1,200% from Fulgent Genetics Inc. (FLGT) in less than two years.

Such returns could pale in comparison to future opportunities.

This moment presents a once-in-a-generation chance for strategic investors.

If you missed last week’s free presentation, you can access it right here. Please note that today is the final day it will be available.

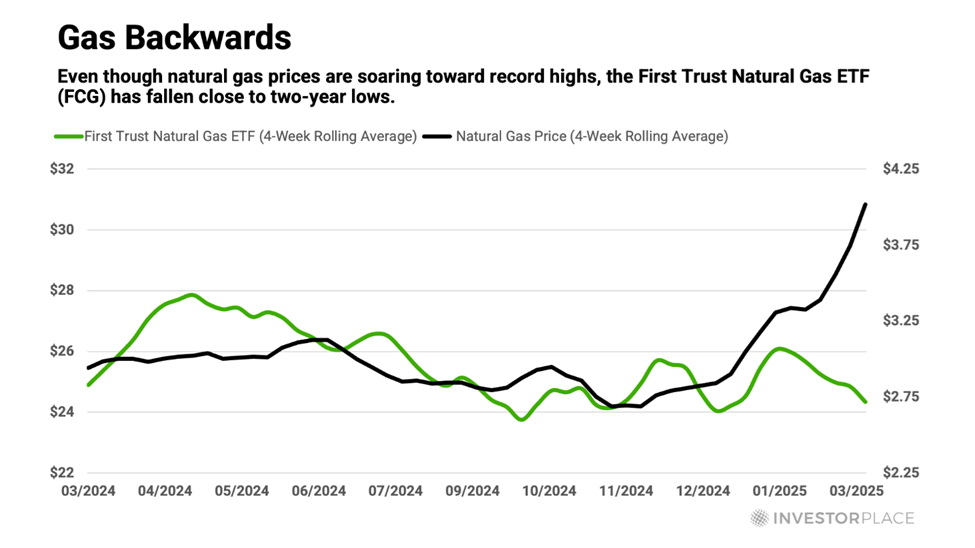

Natural Gas Market Offers Potential Buying Opportunity

In a different sector, we are observing a significant disconnect in the natural gas market, hinting at a potential buying opportunity for savvy investors.

While gas prices are on the rise, natural gas stocks have not reflected this trend, with demand consistently increasing as inventories decline. This discrepancy could lead to a surge in quality natural gas stocks, aligning with the current bullish market dynamics.

Eric, editor of Investment report, emphasized this potential on Monday.

For context, consider the comparison between the First Trust Natural Gas ETF (FCG) and the 4-week rolling average price of natural gas. FCG holds significant oil and gas companies such as ConocoPhillips, Hess, EQT Corporation, Occidental, and Diamondback Energy.

The chart below illustrates how FCG’s price (in green) has remained stagnant over the past two months, irrespective of a 35% increase in the price of natural gas (in black).

This trend underscores the basic principles of supply and demand. Rising natural gas prices fit the current narrative as our domestic supply continues to dwindle against rising demand levels.

As Eric notes:

U.S. natural gas in storage, relative to…

U.S. Natural Gas Demand Expected to Outpace Supply in Coming Years

Natural gas storage levels are currently 14% below the seasonal three-year average and have been declining sharply for almost a year.

With this reduction, U.S. natural gas demand is projected to exceed supply significantly over the next two years, leading to even lower stockpiles compared to historical averages.

Export Growth Drives Inventory Declines

In February, natural gas exports to U.S. export plants reached record levels, with March expected to break those records again.

Looking ahead, forecasts suggest that the supply-demand imbalance will persist, especially when factoring in U.S. exports. According to Eric from Pivot and Flow Daily,:

The U.S. Energy Information Administration (EIA) anticipates that LNG exports will increase by 2.1 Bcf/d in 2026, due to new export facilities.

Unlike spikes in domestic demand that are typical during extreme weather, LNG export demand remains steady. Once established, this demand continually utilizes domestic gas supplies.

This consistent demand exerts upward pressure on natural gas prices, particularly if production does not keep up.

The EIA forecasts that domestic production will grow by 3.6% over the next two years. However, this growth lags behind the predicted demand growth of 5.8%.

These conditions create an environment conducive to increasing stock prices for key natural gas companies.

So why haven’t prices risen yet?

Market Uncertainty Impacting the Oil Sector

Last week, we initiated a new segment called “Uncertainty Watch.” This highlights the lack of confidence in the economic outlook, leading consumers to delay purchases and corporate planners to postpone significant capital expenditures, much of which is influenced by President Trump’s unclear tariff strategies.

This uncertainty affects the oil industry. The Federal Reserve Bank of Dallas recently published the results of its quarterly survey among anonymous oil executives.

One survey response captured the sentiment: As a public company, our investors dislike uncertainty. This has increased the implied cost of capital for our business, causing public energy stocks to decline more sharply than oil prices in the last two months.

This uncertainty stems from the mixed messages from the current administration.

It’s worth noting that while oil and gas are different markets, the decline in oil prices has impacted natural gas stocks too. Eric explains:

Falling crude prices are largely responsible for this trend.

For one, low crude prices cast a negative shadow over the entire fossil fuel sector. Additionally, many major natural gas producers also extract significant amounts of crude oil.

This has caused the shares of several North American natural gas producers to drop, irrespective of their crude output levels.

As the market develops, it’s clear that there is a disconnect between natural gas prices and leading natural gas stocks. Historically, this divergence tends to correct itself.

Eric recently shared his preferred strategy for managing this discrepancy with his Investment Report subscribers. While respecting subscriber confidentiality, it is worth noting that ERic believes:

Trading at less than eight times earnings, this stock appears undervalued compared to both its peers and hidden earnings potential in the Delaware Basin of the Permian.

This indicates a strong buying opportunity.

In summary, U.S. natural gas is classified as a “Buy,” indicating that this natural gas opportunity is a “Strong Buy.”

For more information on joining Eric in the Investment Report, click here.

We will continue to keep you informed on these developments in the Digest.

Have a pleasant evening,

Jeff Remsburg