Uber Technologies (NYSE:UBER) has exhibited substantial gross booking and revenue growth. Their relentless focus on operational efficiencies and expense management has not only bolstered the take rate but also enhanced the operating margin. This prompts me to initiate coverage with a ‘Buy’ rating and a fair value of $90 per share, an estimate indicating a 40% undervaluation than the current price.

Steady Growth in Mobility Business

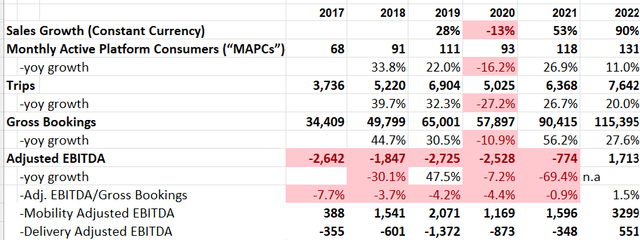

The growth trajectory of Uber’s mobility business has been nothing short of remarkable, as evidenced by robust booking growth and adjusted EBITDA expansion over the past few years.

Evidently, the core UberX business has seen a staggering 20% year-on-year growth, attributed to the continuous influx of drivers into their platform. Moreover, their strategic introduction of additional offerings such as hailable products, taxis, three-wheelers, and Uber for Business products has collectively bolstered revenues to $9 billion, marking an impressive 80% year-over-year growth.

With a promising outlook, Uber foresees ample growth prospects in international markets and has successfully entrenched itself as the market leader in the Mobility sector, experiencing substantial growth in both the number of drivers and riders. The supplementary services offered on their platform add to the revenue stream with minimal incremental costs.

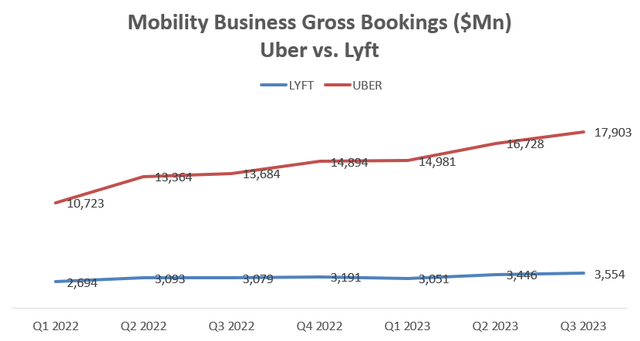

Comparing the gross booking growth in the ride-sharing business for both Uber and Lyft (LYFT) makes it evident that Uber has significantly outperformed its competitors in the Mobility business.

Delivery Business Gaining Profits

Uber’s delivery business now contributes over 34% of its total revenue, achieving positive adjusted EBITDA profits in FY22. Despite facing intense competition in the delivery sector, I am optimistic about Uber’s ability to grow its business profitability for several reasons.

Primarily, their capitalization on network efficiencies as they scale their operations has led to a notable decrease in the cost per trip, reaching an all-time low in the US marketplace business. Additionally, Uber strategically leverages the technology platforms of both Mobility and Delivery, resulting in the sharing of engineering resources that unlock synergies at the group level, ultimately reducing operational and research and development expenses for the Delivery business.

Moreover, Uber’s diversification of its Delivery business into new vertical markets such as grocery stores, convenience stores, and alcohol holds the potential to expand their distribution network and improve operational efficiencies. For instance, their partnership with Albertsons (ACI) grocery chains, serving their 1,200 stores, exemplifies this expansion.

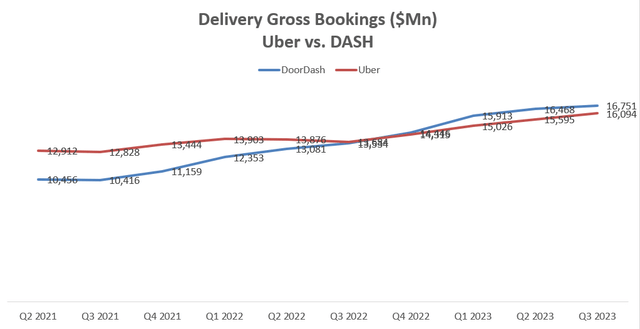

It’s essential to note that Uber’s Delivery business faces direct competition from DoorDash (DASH), which has been witnessing rapid growth. Thus, it is imperative for Uber investors to closely monitor DoorDash’s performance in the future.

Recent Results and FY24 Outlook

Excluding the impact of the pandemic period, Uber has demonstrated rapid growth over the past few years. The company has shown improvement in cash flow and operating margin, with positive free cash flow achieved starting from FY22. Furthermore, Uber maintains a robust balance sheet with a net cash position.

In Q3 FY23, Uber achieved an outstanding 10% growth in revenue in constant currency, accompanied by an impressive 111% growth in adjusted EBITDA. Ending the quarter with $5.2 billion in cash and cash equivalents, Uber boasts a robust balance sheet. The remarkable profit surge and topline growth were reflected in their free cash flow, which witnessed a sensational 153% year-over-year increase.

For Q4 FY23, Uber anticipates a substantial 18%-21% gross booking growth on a constant-currency basis, with adjusted EBITDA expected to be in the range of $1.18-$1.24 billion. This guidance indicates a continuation of strong topline growth and notable margin expansion. Considering their impressive year-to-date results, I foresee no surprises in their Q4 earnings. The market’s primary focus is likely to shift towards Uber’s FY24 guidance.

I project that Uber can maintain approximately 20% revenue and gross booking growth in FY24, coupled with ongoing margin improvement. A potential interest rate cut by the Fed would be positive for Uber, enhancing affordability. The robust gross booking growth demonstrated in their Q3 FY23 results indicates sustained strength, and I foresee no immediate reasons for a slowdown. Moreover, Uber’s commitment to operational efficiency and disciplined expense management makes it highly likely for them to continue delivering margin expansion.

Valuation

I am confident that Uber can sustain margin expansion over the next decade. With the current stock price undervaluing Uber by approximately 40%, there is an opportunity for investors to benefit from the company’s long-term growth prospects.

The Road Ahead: Projecting Uber’s Revenue and Margin Growth

Uber, the ride-hailing giant, has been navigating the tumultuous landscape of the modern tech industry with a strategy deeply rooted in capitalizing its operating leverage and scaling operations. A forecast of a 20% normalized revenue growth over the next two years, gradually moderating to 8% by FY32, showcases the company’s ambition amidst a higher revenue base. The incorporation of a 1.2% acquisition growth assumption highlights Uber’s penchant for strategic business expansions. Moreover, leveraging operating leverage is expected to propel the company towards a projected 12.6% operating margin by FY32.

A meticulous financial model, crafted with a 10% discount rate and a 4% terminal growth rate, has culminated in the estimation of Uber’s fair value at $90 per share. The stock’s current trading position at 37 times FY24’s free cash flow, as determined by the model, portends a promising trajectory. It is anticipated that Uber’s margin expansion and top-line growth will pave the way for a substantial surge in its free cash flow in the coming years.

Potential Pitfalls

Leadership Impact: Dara Khosrowshahi, Uber’s present CEO and former head of Expedia (EXPE), has been under scrutiny owing to his aggressive acquisition approach during his stint at Expedia. The aftermath indicates a loss of competitiveness against rivals, portraying a cautionary tale of unchecked ambition.

Drizly Acquisition: Uber’s acquisition of Drizly for $1.1 billion in 2021, followed by the decision to phase out the alcohol delivery app by March 2024, raises questions about the strategic wisdom behind the move. While not an abandonment of the alcohol delivery business, the closure of the Drizly app has cast a shadow on the rationale behind the $1.1 billion investment.

Insights Ahead

Despite impediments, a hopeful narrative emerges; Uber’s potential for remarkable revenue and gross booking growth in the near future holds promise. The pivotal importance of margin expansion in influencing stock price is evident. An assessment indicating the stock’s undervaluation by over 40% has prompted a ‘Buy’ rating with a fair value target of $90 per share.