UiPath (PATH) reported a significant financial advantage, ending fiscal Q4 2026 with $1.47 billion in cash and equivalents and no debt. This positions the company favorably within the automation sector, particularly amid rising interest costs and refinancing risks affecting many tech firms.

With a current ratio of 2.48, exceeding the industry benchmark of 2.1, UiPath can confidently manage near-term obligations while pursuing opportunities in AI and geographic expansion. This financial stability allows UiPath to navigate economic uncertainties without compromising strategic initiatives, setting it apart from competitors like Microsoft and ServiceNow, who face different financial pressures.

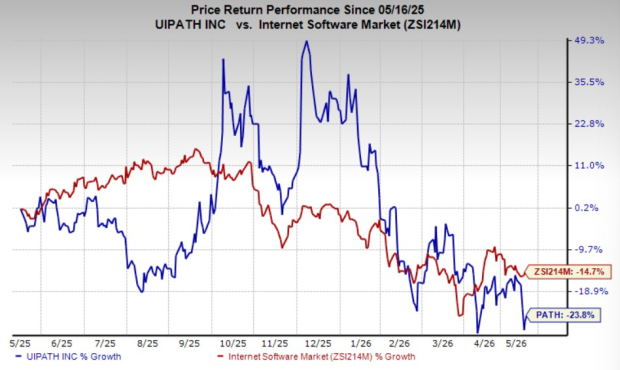

Despite a 24% stock decline over the past year compared to the industry’s 15% decline, UiPath’s forward price-to-earnings ratio stands at 12.01, significantly lower than the industry average of 26.52. The Zacks Consensus Estimate for fiscal 2027 earnings remains unchanged, and UiPath currently holds a Zacks Rank #3 (Hold).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.