Ulta Beauty, Inc. ULTA is capitalizing on the favorable beauty industry trends by prioritizing omnichannel strategies. The company’s relentless efforts in driving traffic, enhancing brand loyalty, and expanding its loyalty program are paying off handsomely. These initiatives, combined with robust transformation endeavors, translated into impressive fourth-quarter fiscal 2023 results, surpassing the Zacks Consensus Estimate.

Despite the dynamic macroeconomic environment, Ulta Beauty’s management remains upbeat about the industry’s resilience and growth prospects. The company is doubling down on its transformative initiatives, aiming to cement its leading position while enhancing customer experience and engagement through core traffic and experience enhancement strategies.

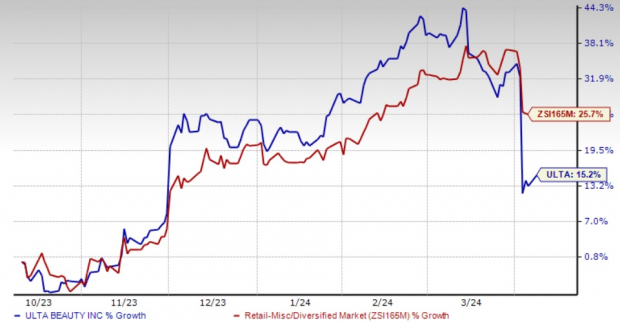

Image Source: Zacks Investment Research

Strategic Drive: Upholding Core Priorities

Ulta Beauty’s strategic priorities revolve around fortifying its omnichannel presence, leveraging both physical and digital realms. The company is employing innovative tools to enhance guest experiences, such as virtual try-on tools and in-store educational initiatives. Moreover, Ulta Beauty focuses on offering curated and exclusive beauty products, prioritizing customer engagement, optimizing cost structures, nurturing organizational talent, and enriching its corporate culture.

Guests seamlessly traverse physical and digital channels, with Ulta Beauty continuously enhancing guest experiences across all touchpoints. The company’s expansion efforts include new store openings, remodels, and relocations, underscoring its commitment to omnichannel growth.

The company’s digital technology modernization is a key enabler for elevating guest experiences and driving digital innovation, leading to notable high-single-digit growth in digital channel sales during the fourth quarter of fiscal 2023.

Ulta Beauty’s collaboration with Target, with 155 Ulta Beauty at Target shop openings in fiscal 2023, further augments its omnichannel reach, enhancing customer accessibility.

The Glow of Skincare Excellence

Ulta Beauty’s dominance in major beauty categories, especially skincare, has been a highlight. The fourth quarter of fiscal 2023 witnessed robust growth in the skincare segment, driven by popular brands like Bioma, Bubble, Good Molecules, La Roche-Posay, Dermalogica, and Cetaphil. Guests’ growing emphasis on self-care and healthy skincare routines, coupled with Ulta Beauty’s focus on novelty and innovation, bode well for sustained growth in the skincare category.

Challenges in the Horizon

Despite its successes, Ulta Beauty faces challenges in the form of rising SG&A costs. Management anticipates SG&A deleverage in fiscal 2024 due to wage pressures, investments in core traffic support, and transformational pursuits. The company foresees modest gross margin declines in fiscal 2024, primarily due to soft merchandise margins and supply chain cost pressures.

Nonetheless, Ulta Beauty remains optimistic about its revenue and earnings outlook for fiscal 2024, underpinned by its robust omnichannel strategies, customer engagement initiatives, and unique product offerings. The company anticipates revenue growth and expects earnings to rise, reflecting its resilience in a challenging retail landscape.

Ulta Beauty’s stock, holding a Zacks Rank #3 (Hold), has outperformed the industry in recent months, indicating investor confidence in the company’s strategic direction and growth prospects.

Three Retail Gems Worth Considering

Burlington Stores BURL, Abercrombie & Fitch ANF, and The Kroger Co. KR are notable retail picks to keep on the radar. Each company boasts a unique value proposition and growth potential in the competitive retail landscape.

Investors and analysts remain optimistic about the growth prospects of these companies, reflecting a positive sentiment in the retail sector.