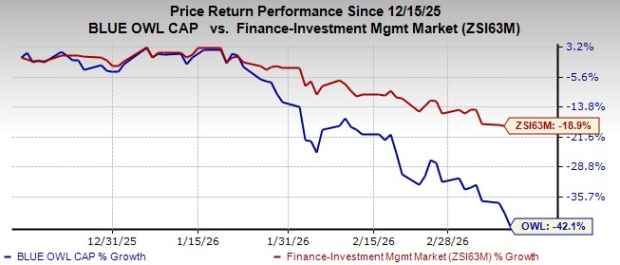

Blue Owl Capital Inc. (OWL) has struggled in the private credit sector, underperforming with a Zacks Rank of #5 (Strong Sell). Over the past three months, OWL shares have lagged behind the industry due to investors recalibrating risk, with only one earnings beat in the last four quarters against the Zacks Consensus Estimate.

As of December 31, 2025, Blue Owl faces significant liquidity concerns, especially in retail-oriented private credit, raising red flags about fundraising momentum and fee growth. A notable incident occurred in February, when liquidity issues at Blue Owl Capital Corporation II led to restricted withdrawals after requests exceeded 5%. Furthermore, with $28.4 billion in assets yet to generate fees, management anticipates over $325 million in annual management fees once these assets are deployed, emphasizing the impact of deployment timing on earnings recognition.

The broader alternative asset management sector, which includes competitors like Apollo Global Management and Blackstone Inc., is also feeling the effects of bearish investor sentiment amid private credit apprehensions. High expenses and concerns regarding borrower quality, particularly in technology-related sectors, continue to contribute to the overall challenges facing Blue Owl.