CF Industries Positioned to Benefit from Tariff Decrease and Market Trends

Discussions around dividend growers often bring attention to those ready to capitalize on market changes. CF Industries (CF), a key American producer of fertilizers and the largest manufacturer of ammonia, stands out as a prime candidate for growth amid the recent easing of tariffs.

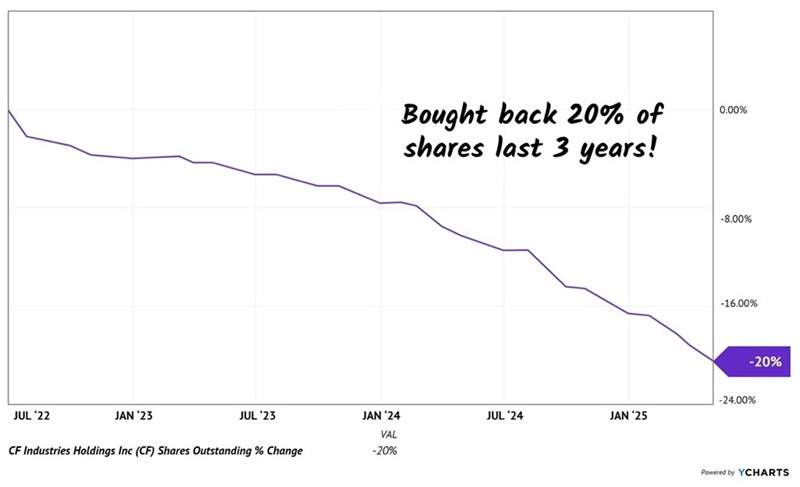

Why is CF Industries poised for this potential upturn? Its management has demonstrated confidence by initiating significant stock buybacks, amounting to 20% of the company’s “float” over the past three years. Recently, the board authorized an additional $2 billion for share repurchases.

Impact of the US-China Tariff Truce

The United States and China, two colossal players in global agriculture, have seen tariffs on exports fall dramatically. Tariffs on US exports to China have decreased from 125% to 10%, while on Chinese exports to the US, they dropped from 145% to 30%. This reduction in tariffs benefits American farmers and suppliers like CF Industries, enhancing their profitability.

With tariffs relaxing, US farms can expect an uptick in profits. Concurrently, CF can leverage its US manufacturing base, which not only circumvents tariff issues but also allows access to cheaper North American natural gas—an essential input for ammonia production, constituting 70% of the costs.

Inflation-Cutting Strategies Favor CF

The current administration, spearheaded by Treasury Secretary Scott Bessent, plans to tackle inflation through a multi-faceted strategy that includes regulating tariffs, lowering costs via deregulation, and increasing oil production to reduce energy prices. Stronger crop yields, supported by fertilizer producers like CF, will further help stabilize food prices.

Addressing the Global Ammonia Shortage

Another essential factor in CF’s trajectory is the global ammonia shortage, with estimates indicating that approximately seven new factories are necessary to meet the demand. CF is responding by developing a new $4 billion plant in Louisiana known as the Blue Point Complex, which will also incorporate advanced carbon capture technology to secure its future viability.

This facility is being constructed in partnership with Japanese firms, with CF responsible for roughly $2.2 billion of the total project costs, thereby managing financial risk efficiently.

Strategic Buybacks Enhance Shareholder Value

CF Industries is currently seeing a resurgence in demand for its nitrogen fertilizers and is wisely using its profits to repurchase shares. At about 11.4 times trailing earnings, CF trades well below the S&P 500 average of around 23. Since 2022, it has returned $5 billion to shareholders through dividends and buybacks, a figure expected to grow with the board’s recent authorization.

Lowering the number of shares on the market enhances future dividend hikes for the remaining shares. CF’s current dividend yield stands at 2.3%, with an expectation of increased payouts driven by a reduced share count and strong free cash flow, which currently supports dividends at just 19% of its total.

The company’s balance sheet remains robust, managing only $1.6 billion in long-term debt against total assets of $13.3 billion.

Conclusion: A Positive Outlook for CF Industries

CF Industries is on a promising path that highlights its potential for dividend growth and shareholder returns. As market conditions continue to shift, its strategic positioning in the fertilizer sector aligns well with emerging trends and policy changes.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.