Amidst the fervor that has characterized the tech sector in recent times, artificial intelligence (AI) has emerged as the propulsive force underpinning soaring market gains, reminiscent of its instrumental role in the preceding year. While the glamour of megacap stocks continues to captivate Wall Street, there is an array of burgeoning contenders eagerly seizing opportunities within this exhilarating niche.

Palantir Technologies (PLTR), with a market capitalization of $55 billion, has gained prominence for its data integration and analytics platforms, notably Gotham and Foundry. Gotham primarily caters to government and intelligence applications, whereas Foundry targets commercial clientele.

The company’s stock witnessed a staggering 167% surge last year, dwarfing the S&P 500 Index’s gain of 25%. Bolstering this meteoric rise, Palantir’s robust fourth-quarter results have further piqued investor interest, propelling its shares by an additional 42% year to date.

Although the overall Wall Street sentiment regarding PLTR stock leans bearish, largely owing to its lofty valuation, some experts tout it as an undervalued AI stock with promising long-term prospects.

Palantir’s AIP Platform Drives Exceptional Growth

Undoubtedly, Palantir’s AIP (Artificial Intelligence Platform) has been the propellant behind the company’s recent financial and stock market upswing. This platform facilitates data analysis for various industries, unearthing intricate patterns and invaluable insights essential for informed decision-making. In his annual shareholder letter, CEO Alex Karp stressed that “momentum with AIP is now significantly contributing to new revenue and new customers” for the company.

In the fourth quarter, total revenue surged by 20% year-over-year to $608 million, while full-year revenue escalated by 17% to $2.23 billion compared to 2022. Palantir also reported a fifth consecutive profitable quarter, with a GAAP (generally accepted accounting principles) profit of $93 million. Notably, it has become eligible for inclusion in the S&P 500 Index, having met the requirement of achieving profitability for four consecutive quarters.

Palantir’s extensive involvement with government agencies has markedly propelled its growth, with government contracts contributing 54% of its total revenue, furnishing a consistent revenue stream. Additionally, it burnishes Palantir’s standing for furnishing potent and secure data solutions. However, this fervent government association also harbors risks, such as controversial projects and potential downturns in defense budgets.

Currently, Palantir has an ongoing three-year contract worth $250 million with the U.S. Department of Defense to provide AI data analytics services. Moreover, the company has forged collaborative agreements with foreign government agencies, culminating in a revenue surge of $324 million in Government contracts in Q4, marking an 11% year-over-year increase. Over the entire year, revenue from this source grew by 14% to $1.2 billion.

While government contracts indisputably constitute a pivotal component of Palantir’s business, the company has been actively broadening its portfolio to encompass commercial clients across diverse industries. The Commercial segment witnessed a 32% year-over-year revenue surge, generating $284 million, with the U.S. commercial market alone witnessing a staggering 70% surge to $131 million.

The Commercial segment, rapidly amassing momentum, currently accounts for 46% of total revenue. Last year witnessed Palantir forging strategic alliances with CAZ Investments and PwC, which is anticipated to furthermore catalyze the segment’s ascent this year.

Management anticipates a 40% upsurge in U.S. commercial revenue, potentially breaching the $640 million mark in 2024, thereby propelling total revenue to a range of $2.65 billion to $2.69 billion for the full year, translating to an 18% to 20% year-over-year growth. Simultaneously, analysts project a revenue upswing to $2.67 billion, accompanied by an enhanced earnings growth of 30.5% to $0.33 per share.

Despite this meteoric upsurge, Palantir proudly touts a robust balance sheet – a commendable feat indeed. Notably, the company boasted a $3.7 billion cash balance (comprising cash, cash equivalents, and U.S. treasuries) at the conclusion of 2023. Furthermore, in 2023 alone, Palantir generated a solid $731 million in adjusted free cash flow (FCF), with expectations of reaching $800 million to $1 billion in 2024.

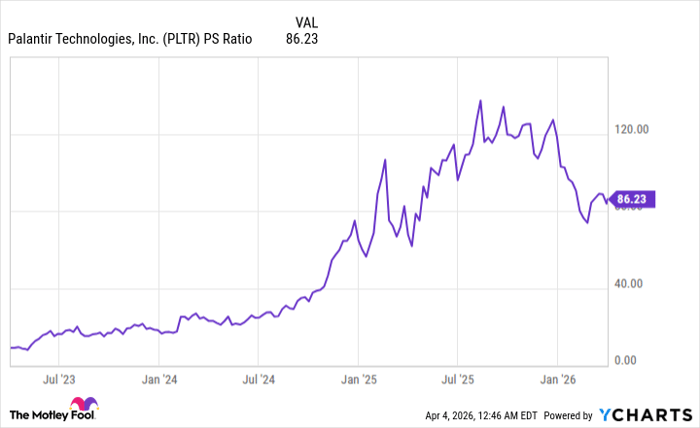

Analysts prognosticate a 20.5% surge in Palantir’s revenue, accompanied by a 20.4% earnings upswing in 2025. Nonetheless, the stock is widely regarded as relatively expensive, trading at 64 times forward earnings and 17 times forward sales.

Wall Street Opinions Are Mixed on PLTR

In recent developments, HSBC analyst Stephen Bersey revised his stance on PLTR to “neutral,” citing the lofty valuation. Nevertheless, the analyst expressed admiration for the company’s AI strategies and growth prospects, assigning a price target of $22 for PLTR.

Meanwhile, Citi analyst Tyler Radke upgraded PLTR to “hold” from “sell” following the company’s robust quarterly results, reflective of its sustained profitability strength. The analyst also upped the stock’s target price to $20, attesting, “U.S. Commercial strength is becoming increasingly conspicuous.”

Similarly, impressed by the company’s AIP platform, Brent Thill of Jefferies forayed into upgrading the stock to “hold” from “sell.” Mariana Perez Mora from BofA Securities voiced comparable optimism, reaffirming her “buy” rating and elevating the target price to $24 from $21.

While Palantir’s stock continues its lofty ascent, the overarching sentiment among analysts oscillates with a consensus “hold” rating. Among the 13 analysts covering the stock, two advocate a “strong buy,” one recommends a “moderate buy,” five favor a “hold,” one advises a “moderate sell,” and four counsel a “strong sell.”

Palantir has transcended its average target price of $17.54, with its lofty target price of $30 hinting at an upside potential of 22.7% in the forthcoming 12 months.

Why PLTR Is the Best Underrated AI Stock To Pick Now

The AIP platform is still in its fledgling stage, with its full potential yet to be unraveled, auguring a plausible revenue and earnings upswing in the coming years. Alex Karp emphatically underscored, “AIP is the future of our company, and we firmly believe that it will emerge as the dominant platform for the entire industry.”

As Palantir diligently expands its footprint across government and commercial sectors, diversifies its AI offerings, and ventures into global markets, the future teems with promise. Perhaps, it’s a premium worth considering.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.