Can Upstart Holdings (NASDAQ: UPST) stock stage a remarkable turnaround? After experiencing a downward financial spiral for six consecutive quarters, investor confidence in this fintech venture is waning. The stock, once known for its rollercoaster movements, has plummeted by 36% in the tumultuous year of 2024. Now, the burning question lingers – is Upstart stock a value trap in disguise or a diamond in the rough waiting to be unearthed?

The Beacon of Evolution in Credit Evaluation…

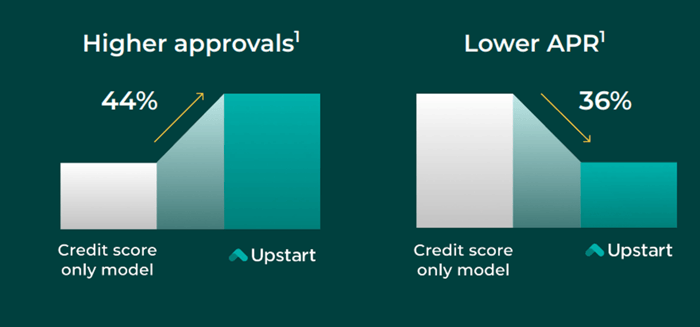

Back in late 2020, Upstart emerged as a shining beacon of hope in the financial technology sector. A pioneer in the niche of credit evaluation, the company’s AI-powered platform promised to revolutionize the assessment of credit risk. By utilizing artificial intelligence, Upstart could more accurately determine the creditworthiness of potential borrowers, leading to increased loan approvals without amplifying the risk for lenders.

Unlike the traditional FICO credit score model, which had remained stagnant for decades, Upstart’s innovative technology aimed to disrupt the status quo and deliver superior outcomes for both borrowers and lenders alike.

With a growing roster of partner banks and credit unions and an expansion into the realm of auto lending, Upstart seemed unstoppable. Its revenue figures were skyrocketing by triple digits, and profitability was soaring. Naturally, investors clamored to seize a piece of this tantalizing opportunity, propelling the stock to unprecedented heights.

Yet, in hindsight, the meteoric ascent of Upstart’s stock – which soared to a price-to-earnings ratio exceeding 400 – set the stage for a precipitous decline.

Navigating the Stormy Seas…

As a lending platform, Upstart stands at the mercy of fluctuating interest rates. During periods of low interest rates, its model excels in identifying creditworthy borrowers, as lower rates translate to reduced default risks. However, when interest rates surge, a myriad of challenges emerge. A smaller pool of borrowers can afford loans at elevated rates, financial institutions adopt a more cautious stance in approving loans, and the likelihood of defaults intensifies – all of which undermine Upstart’s core operations.

Consequently, Upstart witnessed a catastrophic drop in revenue, plunging profitability into the red. In the fourth quarter of 2023, the company reported a 4% year-over-year decline in revenue – compounding the earlier decline in the same quarter of 2022. While its latest net loss of $42.4 million marks an improvement from the $55.3 million loss in the preceding year, it remains a disheartening development for stakeholders.

Despite its challenges, Upstart asserts that its model outperforms the traditional credit scoring system, even in the current economic landscape.

Image source: Upstart Holdings.

With a network encompassing over 100 lending partners and the recent introduction of a home equity product in 12 markets, Upstart continues to diversify its offerings. Positioned within the expansive mortgage market, boasting a $1.5 trillion annual opportunity, the company is exploring bundled product solutions to spur greater engagement and propel growth.

Finding Light at the End of the Tunnel…

Looking ahead, management anticipates first-quarter revenue of $125 million, reflecting a 21% uptick from the previous year. While this forecast appears promising, it remains significantly below the revenue figures recorded in the first quarter of 2022.

Despite the current turbulence, the long-term narrative surrounding Upstart remains compelling. As its model inching closer to supplanting the archaic credit scoring framework and poised to benefit from a downturn in interest rates, the company’s future outlook appears optimistic. With each passing year, and additional operational experience under its belt, Upstart may become more resilient to the cyclical disruptions plaguing its business.

Currently sporting a price-to-sales ratio of 4, Upstart may not be exorbitantly priced; however, for a company grappling with challenges, including dwindling revenue and persistent losses, it doesn’t quite qualify as a bargain.

Investing in Upstart stock at this juncture demands a substantial appetite for risk. Brace yourself for potential turbulence and wild fluctuations before witnessing a decisive upward trend. In the meantime, consider allocating your investment capital towards stocks with clearer growth trajectories as you monitor Upstart for signs of a potential resurgence.

Is Upstart the right investment choice for you at this moment?

Before diving into Upstart stock, ponder on this – the Motley Fool Stock Advisor team has recently unearthed what they consider the top 10 stocks for astute investors to acquire now… and Upstart failed to secure a spot on their prestigious list. These 10 meticulously selected stocks hold the potential to yield staggering returns in the years ahead.

The Stock Advisor service provides a blue-chip guide to investment success, offering expert advice on portfolio construction, timely updates from analysts, and a pair of fresh stock recommendations each month. Since 2002, the Stock Advisor service has surpassed the S&P 500 returns by a threefold margin*

Explore the 10 recommended stocks

*Stock Advisor returns as of March 21, 2024

Jennifer Saibil does not hold any positions in the mentioned stocks. The Motley Fool holds positions in and endorses Upstart. The Motley Fool follows a transparent disclosure policy.

The perspectives expressed here solely represent the views of the author and do not necessarily align with those of Nasdaq, Inc.