Vale S.A. failed to meet expectations in the fourth quarter of 2023, reporting adjusted earnings per share of 56 cents. This figure fell short of the Zacks Consensus Estimate of $1.04, marking a stark 32% decline from the year-ago quarter’s 82 cents. While revenues climbed 9% year over year to approximately $13.05 billion, the increase in provisions linked to Samarco’s dam failure weighed heavily on Vale’s profitability.

Revenues Surge Despite Challenges

The noteworthy surge in net operating revenues was a bright spot, exceeding the Zacks Consensus Estimate, reaching $12.95 billion. Within the Iron Solutions segment, net operating revenues saw an 18% uptick year over year to $11 billion, driven by elevated iron ore realized prices, albeit offset by lower sales volumes.

Vale’s Operating Performance Analysis

In the fourth quarter of 2023, Vale managed to keep its cost of goods sold in check at $6.9 billion, reflecting a 3.7% decrease from the previous year. The company’s gross profit shot up by an impressive 29% year over year to reach $6.2 billion. Furthermore, the gross margin expanded to 47.2% compared to 40.1% in the year-ago quarter.

In terms of expenditure, selling, general and administrative costs experienced a marginal 1% year-over-year decrease to $146 million. Meanwhile, research and development expenses grew by 6% to $231 million from the comparable period last year.

Adjusted operating income soared to $5.5 billion, marking a substantial 47% improvement year over year. Vale’s adjusted EBITDA also demonstrated a notable increase, reaching $6.3 billion in the fourth quarter, compared to $4.6 billion in the same period the previous year.

Balance Sheet & Strategic Moves

Exiting 2023 with around $3.6 billion in cash and cash equivalents, Vale displayed sound financial footing. While its cash flow from operations hit $13.2 billion in 2023, compared to $11.4 billion the year before, the company reported a gross debt of $12.5 billion at the end of 2023.

Vale’s strategic agreements with companies like Anglo American and Hydnum Steel underscore its commitment to innovation and expansion. The partnership with Anglo American, involving the acquisition of a 15% ownership interest, and the collaboration with Hydnum Steel for an iron ore briquette plant project in Spain, showcase Vale’s forward-thinking strategies in diversifying its operations.

Analyst Insights and Stock Performance

Despite the recent challenges, Vale maintains a Zacks Rank #3 (Hold). For investors seeking other options in the Basic Materials space, companies like Carpenter Technology Corporation and Ecolab Inc., with Zacks Rank #1 (Strong Buy), present compelling opportunities. These stocks exhibit strong growth potential and positive earnings trajectories, offering a promising outlook for investors.

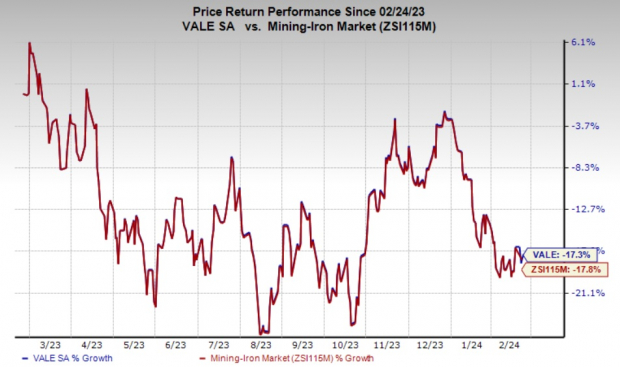

In terms of price performance, Vale saw a 17.3% decline in its shares over the past year, slightly better than the industry’s decline of 17.8%. Analyzing the broader market trends and Vale’s strategic moves can provide valuable insights for investors looking to navigate the market landscape and capitalize on emerging opportunities.

Image Source: Zacks Investment Research