Allstate Corporation Faces Challenges Despite Strong Q4 Results

Allstate Corporation (ALL), a major player in the property-casualty insurance market with a market cap of $49.7 billion, is navigating a tough landscape. Based in Northbrook, Illinois, the company provides a variety of insurance and investment options through agents, call centers, retailers, and online platforms.

Stock Performance Falls Short of Market Gains

Over the past year, Allstate’s stock has lagged behind the overall market. Its shares have seen a 16.3% increase, while the broader S&P 500 Index ($SPX) has appreciated 22.3%. Year to date, ALL’s shares have decreased by 2.7%, in contrast to the SPX, which has gained nearly 4%.

Comparing Returns with Financial Funds

Additionally, ALL has underperformed against the Financial Select Sector SPDR Fund’s (XLF) 32.5% return in the past year and a 7.2% gain year to date.

Q4 2024 Highlights: Strong Earnings Report

The Allstate Corporation showcased a robust financial performance for Q4 2024 on February 5. The company posted an adjusted net income of $7.67 per share, exceeding projections and reflecting a nearly 32% year-over-year increase. This success was fueled by an 8.8% rise in consolidated premiums, totaling $15.1 billion, and a remarkable 46.2% growth in net investment income, which reached $833 million. The increase in investment income resulted from higher returns on fixed-income securities and better performance overall.

Stock Response to Earnings Report

Despite the strong earnings, shares dipped slightly the following day as investors noted missed revenue expectations. Concerns arose over increasing costs, as total expenses grew by 8.1% year-over-year to $14 billion, with catastrophe losses reaching $410 million.

Future Earnings Expectations

Looking ahead to the fiscal year ending in December 2025, analysts anticipate an EPS growth of 1.8% year-over-year, forecasting it to reach $18.65. Allstate’s recent performance history shows promising signs, as it has exceeded earnings forecasts in the last four quarters.

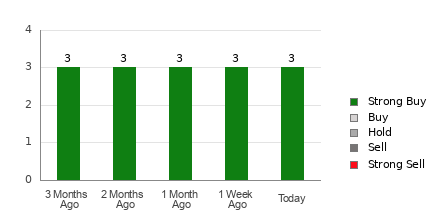

Analyst Ratings and Price Target Updates

The consensus rating among the 20 analysts tracking Allstate is a strong indication of confidence, categorized as a “Strong Buy.” This includes 16 “Strong Buy” ratings, one “Moderate Buy,” one “Hold,” and two “Strong Sells.” Three months ago, the sentiment was slightly less optimistic, reflecting a shift in analyst outlook.

On February 10, Keefe, Bruyette & Woods revised Allstate’s price target to $240 while also raising its EPS estimates for 2025 and 2026. This change was driven by expectations of increased net investment income and improved loss ratios. Even with anticipated $1.7 billion catastrophe losses in Q1 2025, analysts continue to maintain an “Outperform” rating, driven by long-term growth potential.

Currently, ALL trades below the average price target of $225.67. The highest price target set at $279 suggests a potential upside of 48.7% from current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

More news from Barchart

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.