Berkshire Hathaway’s Investment Strategy: AI and Apple Under Scrutiny

Warren Buffett and his team at Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B) have established one of the most impressive investment records in history. Few investors have reached his level of success throughout Berkshire’s extensive history.

Berkshire’s successes come not from chasing hot tech stocks or fads. Instead, Buffett focuses on acquiring reliable companies within well-established industries at discounted prices, then holding them long-term. Although this value-investing approach has waned in popularity, it continues to benefit Berkshire Hathaway shareholders.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Nonetheless, some observers may view Berkshire’s largest holding as an artificial intelligence (AI) Stock, which contrasts with Buffett’s typical investments. With nearly 23% of his portfolio in this Stock, one has to wonder: does Buffett know something that we don’t?

Apple: A Latecomer to AI

Berkshire Hathaway’s largest holding is Apple (NASDAQ: AAPL), which constitutes around 23% of its portfolio. This significant concentration in a single Stock has historically benefited Buffett. By the end of 2023, Apple accounted for approximately 50% of Berkshire Hathaway’s investment portfolio before Buffett began to sell off shares.

As the world’s largest company and a leading consumer electronics brand, Apple revolves around its iPhone-centered ecosystem. Many competitors have already integrated crucial AI features into their phones, while Apple’s generative AI, referred to as Apple Intelligence, is still in the process of being fully launched.

Historically, Apple tends to be a late adopter of cutting-edge technology, favoring perfection over rapid rollouts. This delay places Apple at a disadvantage in the AI landscape compared to its rivals.

Some may label Apple as an AI company due to its AI tools, but it functions more as an integrator. If Apple were to introduce innovative AI features akin to those already available on Android, my perspective might shift. Currently, however, AI does not seem to be Apple’s primary strong suit.

Buffett’s investment in Apple likely doesn’t hinge on anticipated AI advancements. Instead, he capitalized on the Stock‘s attractive pricing in 2016 and has continued to hold it due to its dedicated customer base. Investors should reflect, though, as Apple may not hold the same allure it once did, much like Buffett assessed while selling some shares.

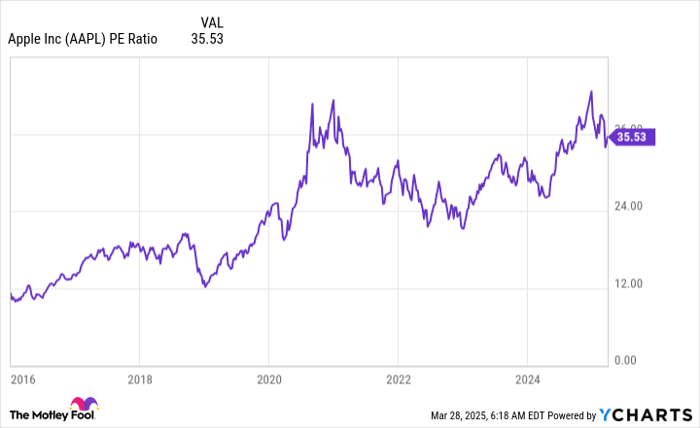

The Stock’s Rising Valuation

In 2016, Apple traded at a lowly 12 times earnings. Today, its valuation has tripled.

AAPL PE Ratio data by YCharts

A significant portion of Apple’s recent gains stems from multiple expansion, revealing that investors are willing to pay higher prices for its Stock‘s earnings. Despite this, Apple’s revenue and earnings per share (EPS) growth have lagged behind that of other tech firms during the same period.

AAPL Revenue (TTM) data by YCharts

Since the boost during the COVID-19 period, Apple’s earnings and revenue have plateaued. Wall Street forecasts revenue growth of only 4.6% for fiscal 2025 and 8% for fiscal 2026. This optimistic outlook for fiscal 2026 likely assumes that Apple Intelligence will be launched as a subscription service, thereby increasing revenue.

However, as Apple Intelligence is still being developed, the company risks losing AI enthusiasts to the Android ecosystem. Given this scenario, the projected growth rate appears overly optimistic.

With Apple Stock at what appears to be inflated levels and the company struggling in the AI race, it seems to be trading based on its historical brand strength rather than current performance. This combination of factors makes Apple less appealing, especially as other tech giants are experiencing rapid growth and are more attractively priced.

Consequently, investors may want to consider reallocating their Apple investments into other companies that offer greater potential for returns, particularly if Apple fails to introduce innovative products as it has in recent years.

A Second Chance at Lucrative Opportunities

Have you ever felt like you missed the opportunity to invest in winning stocks? If so, now may be your chance.

Occasionally, our team of analysts issues a “Double Down” Stock recommendation for firms they predict are on the verge of significant gains. If you believe the opportunity to invest has passed, now is the time to buy before it slips away. The statistics highlight their track record:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $281,057!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,114!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $502,905!*

Our current “Double Down” alerts for three dynamic companies may not arise again for a long time.

Continue »

*Stock Advisor returns as of April 1, 2025

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and Berkshire Hathaway. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.