“`html

Apple’s Stock Performance: Earnings Outlook and Revenue Growth

Apple (AAPL) has gained attention on various stock-tracking platforms, prompting investors to consider key factors that could affect its performance in the near future.

Over the past month, Apple’s shares have risen by +9%, significantly outperforming the Zacks S&P 500 composite, which changed by +0.4%. In contrast, the Zacks Computer – Micro Computers industry, where Apple is categorized, has seen a decline of 8.1%. This raises the critical question: What direction will the stock take next?

While news reports or speculation about potential changes in business operations can make a stock trend, fundamental facts ultimately influence buy-and-hold decisions.

Revisions in Earnings Estimates

At Zacks, we emphasize the importance of changes in a company’s earnings projections. These revisions play a crucial role in determining a stock’s fair value, reflecting its future earnings potential.

Our analysis focuses on how analysts covering the stock modify their earnings estimates based on recent business trends. Generally, rising earnings forecasts lead to a higher fair value for the stock. If the market price is below this fair value, investors typically buy, pushing the price up. Empirical studies show a strong link between earnings estimate trends and short-term stock price movements.

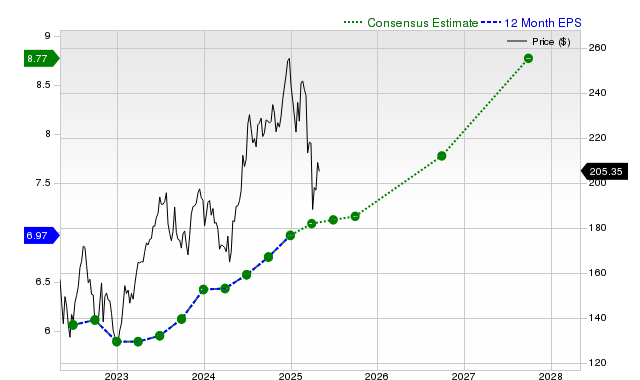

For the current quarter, Apple is projected to report earnings of $1.44 per share, reflecting a year-over-year increase of +2.9%. This estimate has declined by -3% in the past 30 days.

The consensus earnings estimate for the current fiscal year sits at $7.16, representing a +6.1% year-over-year change; however, it has decreased by -1.5% over the last month.

Looking ahead to the next fiscal year, the consensus estimate of $7.78 indicates an +8.7% increase from last year’s expectations. Nevertheless, this estimate has also experienced a -4.7% drop in the last month.

With a robust track record confirmed by external audits, our proprietary stock rating tool, the Zacks Rank, offers insights into short-term price movements, particularly in relation to changes in earnings estimates. Given the recent consensus estimate change and additional factors affecting earnings revisions, Apple is currently rated as Zacks Rank #3 (Hold).

12-Month EPS Analysis

Revenue Growth Forecast

While earnings growth is an important indicator of a company’s financial health, revenue growth is equally critical. Sustained earnings growth typically relies on consistent revenue increases.

In Apple’s case, the consensus sales estimate for the current quarter is $89.12 billion, indicating a year-over-year growth of +3.9%. Estimates for the current and next fiscal years are $403.06 billion and $419.86 billion, respectively, projecting changes of +3.1% and +4.2%.

Last Reported Results and Performance History

In its most recent quarter, Apple reported revenues of $95.36 billion—up +5.1% from a year ago. The EPS for that quarter was $1.65, compared to $1.53 the previous year.

Apple’s revenue surprised estimates by +1.16%, exceeding the Zacks Consensus Estimate of $94.26 billion. Earnings per share exceeded expectations by +2.48%.

Apple has achieved earnings surprises above consensus estimates in each of the last four quarters, outperforming revenue estimates as well during that time.

Valuation Insights

Understanding a stock‘s valuation is essential for making informed investment choices. A stock’s current price should reflect the underlying business’s intrinsic value and growth prospects to determine its future price trajectory.

Assessing a company’s valuation multiples, such as price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF), provides insights into whether a stock is fairly priced, overvalued, or undervalued. Comparing these multiples to historical norms and peer evaluations can clarify a stock’s market positioning.

The Zacks Value Style Score, which evaluates various valuation metrics using a grading system from A to F, indicates whether a stock is overvalued or undervalued. Currently, Apple has a D rating, suggesting it trades at a premium compared to its competitors.

Conclusion

The information presented here may assist investors in deciding whether to pay attention to the market trends concerning Apple. The company’s Zacks Rank #3 implies it may align with overall market performance in the near term.

“`