The Glitch in the Matrix: Reasons Nvidia Isn’t in the Dow Yet

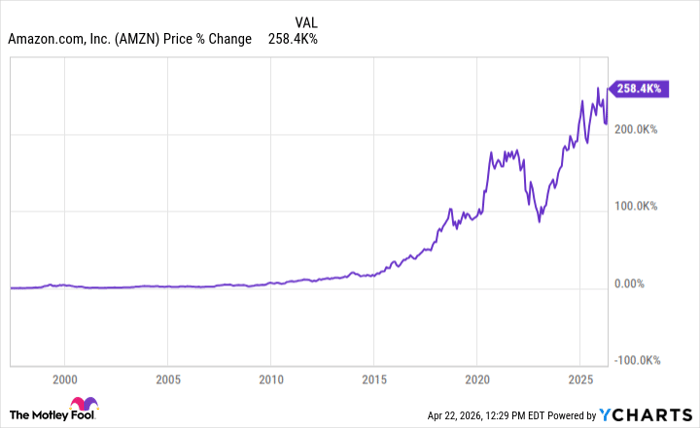

In February, the technological behemoth Amazon became the third big-tech stock to sway into the monumental Dow Jones Industrial Average. Yet, the illustrious Nvidia, a prodigy in itself, lay waiting in the wings. So, what keeps it from claiming a coveted seat at the table?

Nvidia, valued as the most inhabitable company not in the Dow, finds its twilight obscured by Intel, an established Dow disciple. Intel, despite being a thriving entity, stands as the most apparent choice for Nvidia’s forthcoming ingress.

But is the stage set for Nvidia yet? Not quite. Pricing plays a pivotal role in Dow dynamics, and with Intel’s price per share at a modest $42, replacing it may engender misbalance. Furthermore, the ebb and flow of industry trends tilts the scale towards Intel, given its focus on the foundry business rather than direct competition with Nvidia.

Splitting Nvidia’s stock seems to be the entry ticket to the Dow ball. Amazon’s recent split paved its way into the index, creating a precedent Nvidia could emulate with a judicious 5-for-1 stock split to align with the median price of Dow components.

But patience beckons. Dow reshuffles unfold at their own leisurely pace, with no imminent schedule. Amazon’s recent entry quells any immediate swap prospects for Nvidia. Should Nvidia attire for the Dow gala, a symphony of factors awaits harmonization—replacement selection, split ratio formulation, and the intricate timing of the forthcoming index restructuring.

Certainty, in the realm of Nvidia’s Dow debut, remains tantalizingly elusive.

Harvesting the AI Garden: Monetizing Nvidia’s Sojourn

Nvidia, a chameleon in its own right, metamorphosed into an unanticipated entity, most notably due to its foray into data centers.

By rewinding to fiscal 2022, the Graphics dominion overshadowed Compute and Networking divisions. However, a meteoric ascent ensued, with the latter domains assuming supremacy in fiscal 2024—commanding 77.8% of total revenue and 84.5% of segment-operating income.

Customers, voracious for AI prowess, bestow an unending demand upon Nvidia’s innovation. Yet, the fickle semiconductor industry poses a cyclical labyrinth. Presently, soaring demand outstrips supply, kindling a blaze of prosperity and margin expansion for Nvidia.

For Nvidia to sustain its crescendo, the AI realm must prove its mettle in the financial arena. The litmus test lies in the profitability of AI solutions—businesses must reap tangible gains from their investments. Microsoft’s flourishing dalliance with AI provides a roadmap, but the fidelity of this journey hinges on market sentiment, economic tides, and consumer reception.

Every crescendo bears within it the harbinger of a decrescendo. Nvidia too shall weather its downturn, for such is the ebb and flow of cyclic industries. Investors, in due time, might rethink their valuation as the growth narrative mellows.

Awaiting the Overture: Grant Nvidia Time to Conquer

With the wings of a Dow stock, Nvidia’s data center odyssey commenced with a flash—an overture to a symphony yet unfinished.

Before the gavel’s resounding echo admits Nvidia into the Dow chorus, a trial by fire awaits. Mid-cycle scrutiny shall parse the fortitude of Nvidia’s data center juggernaut, for the Dow covets stability over transient glimmers of eminence.

Speculative fervor often whisks valuations to uncharted altitudes. Yet, in this cauldron of excitement, tempered patience must prevail. The magical realism of AI’s saga, intertwined with Nvidia’s ascent, shall only unravel fully with the passage of time—unveiling a narrative that marries growth with substance.

So, while the world anticipates Nvidia’s grandeur, the Dow Jones Industrial Average shall stand vigil, awaiting the telling overture that solidifies Nvidia’s position in the pantheon of blue-chip titans.

Do you dare to wager your fortune on a company that dances on the frontier of technological crescendo, where every rise is met with anticipation for the inevitable fall?

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Mastercard, Microsoft, Nvidia, PayPal, Salesforce, Visa, and Zoom Video Communications. The Motley Fool recommends Intel and Verizon Communications and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $370 calls on Mastercard, long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short January 2025 $380 calls on Mastercard, short January 2026 $405 calls on Microsoft, short March 2024 $67.50 calls on PayPal, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.