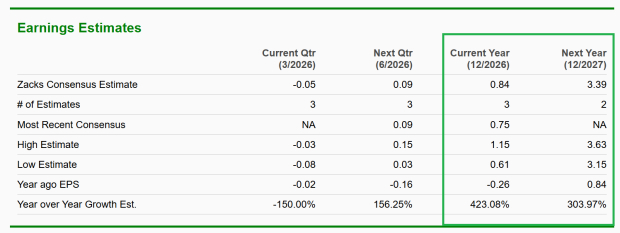

Throughout your career, required minimum distributions (RMDs) may seem like a distant concern, but as the years advance, they inevitably shuffle to the forefront of retirement planning.

RMDs are a pivotal component of retirement financial strategy. Collaborating with a financial advisor can fortify your readiness for these mandatory withdrawals, which wield considerable influence over your taxable liabilities.

RMDs mandate that you commence yearly withdrawals from traditional IRAs, 401(k)s, and other tax-deferred retirement accounts. The chronological trigger for your inaugural RMD hinges on your age. Despite RMDs currently commencing at age 73, a winds of change are afoot. Enshrined in the SECURE 2.0 Act, the RMD age is slated to ascend to 75 by 2033.

Decoding the RMD Age

Superficially, the mechanics of RMDs embody a straightforward paradigm: Account holders extract a predetermined percentage of the tax-deferred funds, predicated on their preceding year-end account balances. This quantum is cleaved by the account holder’s life expectancy factor – a variable computed by the IRS – engendering the RMD quantum.

For instance, the IRS designates a life expectancy factor of 25.5 for a 74-year-old. Should their IRA perch at $200,000 on the prior year’s December 31, their RMD stands at $7,843.

This is the realm of rudimentary arithmetic. Conversely, discerning when to embark on your maiden RMD voyage is a tad more intricate:

- Individuals birthed antecedent to July 1, 1949, must christen their RMDs at age 70 ½, hence these stalwarts should already be disseminating distributions.

- Progeny of the mid-century from July 1, 1949, through 1950 were beckoned to embark upon their RMD odyssey at age 72, and accordingly should have already inaugurated the process.

- Offspring from the expanse of 1951 through 1959 are summoned to partake in their maiden RMD endeavor by April 1 of the post-73 era.

- The brood of 1960 and beyond must discern their inaugural RMD by April 1 of the post-75 epoch.

Evidently, the IRS luxuriate in granting the latitude to postpone the virgin RMD till the April denouement of the mandated inception year. For those inheritors of 1951 vintage, their RMDs debut this epoch while the dispensation to consummate the withdrawal stretches until April 1, 2025. Thereafter, the annual draws must precede the year’s curtain call, signifying that any reluctant first-time RMD partakers in 2024 will necessitate a second withdrawal antecedent to 2026’s dawn.

A word to the wise: A sage financial advisor boasts the acumen to architect a holistic retirement blueprint, poised to encompass RMDs within its tapestry.

To Postpone or Not to Postpone Your Maiden RMD?

The quandary looms: Is it judicious to procrastinate your maiden RMD? In certain scenarios, the stratagem holds water. Should your spouse presently toil, yet plots to pivot towards retirement in the ensuing annum, the deferral portends a prospective descent into a reduced tax bracket by the subsequent April 1.

However, the nether side of the coin proffers that executing bifurcated distributions within a lone annum could propel you skyward into a loftier tax bracket. This duality in RMDs is liable to augment your aggregate income, poteially inculcating levies on 85% of your Social Security benefits. Elevated income thresholds also bode a potential escalation in Medicare premiums, predisposed to an income-related monthly adjustment amount (IRMAA) surcharge.

Nevertheless, should a qualified charitable distribution (QCD) convene with your RMD, the dispensation manifests as a tax-exempt withdrawal. Ergo, ensconcing your virgin distribution in abeyance unfurls a vista where the capital can germinate additional yields until bequeathed unto a beneficent cause. Moreover, in the event of requisitioning the secondary RMD for sustenance, you are blissfully absolved of the fiscal repercussions engendered by dual RMDs within the identical year, courtesy of the antecedently allocated QCD.

No matter your preconceived stratagem for commencing RMDs, adhering to the prescribed timelines reigns paramount. Defaulting on an RMD couriers a chastisement in the guise of a 25% tax on the necessitous sum you neglected to withdraw. While the retribution may exhibit a steely retribution, it’s worth harking back to an era where the penal tariff was a staggering 50% ere the advent of the SECURE 2.0 Act in 2022. Engaging a wizened financial advisor can furnish sagacious counsel to scaffold your RMD trajectory and forewarn you of their fiscal implications.

The Crux of the Matter

The threshold for inaugurating mandatory withdrawals has undergone a metamorphosis for multitudes, yet the option to defer your primordial RMD till the year post the stipulated commencement lingers. This postponement bespeaks a tableau of either favorable or detrimental fiscal consequences, contingent on the overarching financial landscape.

Strategies for Navigating Your RMDs

- If uncertainty shrouds your anticipated withdrawal quantum, SmartAsset proffers a bespoke RMD calculator sculpted particularly to delineate the girth of your compulsory distributions.

- A financial maestro can blueprint your RMD trajectory, potentially diluting their fiscal impact. Unearthing a financial guru doesn’t necessitate arduous exploits. SmartAsset’s cost-free arsenal aligns you with up to three seasoned financial luminaries weaving their craft around your locale, permitting a preliminary tête-à-tête with your matches to pinpoint the right accord. Should you find yourself on the cusp of seeking an adept who shepherds you toward your pecuniary ambitions, consider taking the plunge and embark now.

Photo credit: ©iStock.com/designed491, ©iStock.com/shapecharge, ©iStock.com/katleho Seisa

The post When Should I Take My First RMD? appeared first on SmartReads by SmartAsset.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.