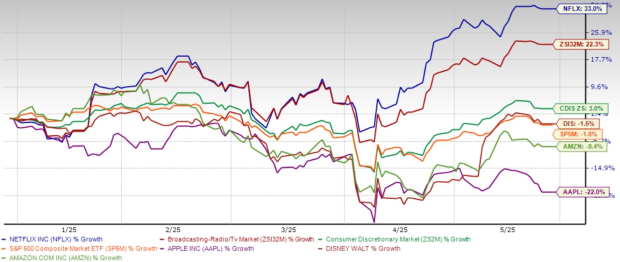

Netflix Share Prices Soar 33% in 2025, Outperforming Competitors

Netflix (NFLX) has gained 33% in 2025, far exceeding rivals like Apple (AAPL), Amazon (AMZN), and Disney (DIS), which saw declines of 22%, 8.4%, and 1.5%, respectively. This performance also outstripped the S&P 500 and the Zacks Consumer Discretionary sector.

Investors are encouraged to view Netflix as a long-term opportunity despite its remarkable performance. The company aims to double its revenues and reach a $1 trillion market capitalization by 2030.

Strong Financial Results Highlight Operational Excellence

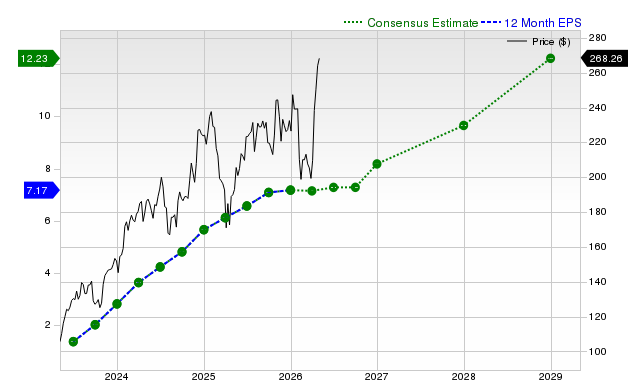

Netflix exceeded financial expectations with an earnings per share (EPS) of $6.61, surpassing estimates of $5.68 by 16.37%. This consistent outperformance spans four consecutive quarters.

Revenue reached $10.54 billion, slightly above the $10.50 billion expected, while the company maintains a forecasted 29% operating margin and $8 billion in free cash flow for 2025. This robust financial performance allows continued investment in content and shareholder return through buybacks.

For 2025, the Zacks Consensus Estimate for Netflix’s revenues is $44.46 billion, reflecting a 13.99% increase, and the estimated EPS stands at $25.32, a 27.69% rise year-over-year.

Membership retention is strong, according to Co-CEO Greg Peters. He indicated that new subscribers acquired during major events show similar retention rates to those drawn in by other premium content, reinforcing Netflix’s ability to convert event-based viewers into long-term customers.

Advertising Growth Projected to Boost Revenue

Netflix sees its advertising sector as a key growth driver. They project that advertising revenue will double in 2025, aided by the rollout of their ad technology platform in major markets, including Canada and the U.S.

This platform allows for sophisticated targeting based on Netflix’s unique data, improving both advertising efficacy and user experience. Co-CEO Peters noted that enhanced targeting, combined with Netflix’s extensive content library, yields better outcomes for advertisers.

Currently, Netflix captures about 6% of consumer ad spend in its markets, indicating significant potential for growth. With its relatively modest advertising presence, the company is well-positioned to gain market share as its platform evolves.

Content Strategy Enhances Global Leadership

Netflix’s content strategy has strengthened with partnerships, such as one with Dan Brown for a new thriller series, showcasing its attraction to high-caliber creative talent. Brown’s series has sold 250 million copies worldwide, indicating a built-in audience.

The investment in global content remains strong, with commitments of $1 billion for Mexican productions, $2.5 billion in Korean content, and continued expansion in 50 countries. This localized approach serves regional viewers while providing global appeal.

Live programming efforts are notably successful, with events like the Taylor-Serrano fight and all-day NFL football on Christmas generating strong viewer engagement and premium advertising prices. Netflix’s ability to integrate live events into its offerings sets it apart from competitors.

Investment Considerations

Netflix’s solid financial results, innovative advertising capabilities, and expanding content strategy place it in a strong position for sustained growth. While its forward 12-month price-to-sales ratio stands at 10.84, significantly higher than the Zacks Broadcast Radio and Television industry’s ratio of 3.7, this premium valuation is supported by Netflix’s unique market position and effective execution.

NFLX’s Premium Valuation Through P/S Ratio

Netflix Maintains Strong Position with Growth Potential

Investors Eye Netflix’s Growth Strategy

Investors interested in streaming should focus on Netflix (NFLX), which demonstrates solid execution and various growth strategies. NFLX currently holds a Zacks Rank of #2 (Buy).

Top Semiconductor Stock Revealed

In a recent analysis, Zacks highlighted a semiconductor stock significantly smaller than NVIDIA. While NVIDIA has seen an increase of over 800% since its recommendation, the new candidate has considerable upside potential.

With robust earnings growth and a growing customer base, this company is well-positioned to cater to the rising demand for Artificial Intelligence, Machine Learning, and the Internet of Things. Global semiconductor manufacturing is expected to grow from $452 billion in 2021 to $803 billion by 2028.

See the Semiconductor Stock Now for Free >>

Stock Analysis Reports Available

Current free stock analysis reports include:

- Amazon.com, Inc. (AMZN)

- Apple Inc. (AAPL)

- Netflix, Inc. (NFLX)

- The Walt Disney Company (DIS)

This article was originally published on Zacks Investment Research.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.