Key Points

-

Oracle is experiencing significant demand for its high-speed, cost-efficient data centers, primarily from AI companies like OpenAI.

-

The company has a substantial backlog of $638 billion in performance obligations, a 363% increase year-over-year. However, concerns about customer fulfillment remain.

-

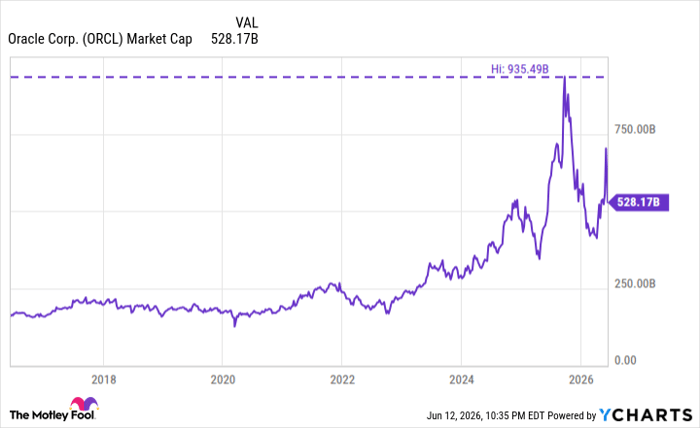

As of now, Oracle’s stock is down 44% from its peak last year, with a GAAP earnings per share of $5.83 and a P/E ratio of 31.6.

Oracle’s data centers are increasingly sought after by AI giants due to their efficiency and speed. As of May 31, the company reported total revenue of $19.2 billion for its fiscal 2026 fourth quarter, marking a 21% year-over-year increase. Notably, Oracle Cloud Infrastructure contributed $5.8 billion to this total, growing at an impressive 93%. However, the $638 billion remaining performance obligations (RPO) reported by Oracle raises concerns; much of this backlog—around $300 billion—comes from OpenAI, which reported just $25 billion in annualized revenue.

Oracle’s stock has found itself down 44% from its all-time high, raising questions about its valuation and future growth. Analysts forecast minimal earnings growth of 7.7% for fiscal 2027, though expectations for fiscal 2028 suggest a higher 45.7% growth potential. Investors are advised to proceed cautiously until Oracle demonstrates consistent positive results in upcoming quarters.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.