AMD Anticipates Strong Q1 Data Center Revenues Ahead of Earnings

Advanced Micro Devices (AMD) is projected to see positive results from robust Data Center revenues in the first quarter of 2025. The company’s earnings report will be released on May 6.

Benefiting from a solid product range and an expanding partnership network, AMD continues to enhance its position within the enterprise data center sector, primarily through its fourth-generation EPYC CPUs.

Notable developments in AMD’s portfolio include the Instinct MI300X Series data center AI accelerators and the Versal RF Series Adaptive SoCs. Industry partners such as Dell Technologies, HPE, Lenovo, and Supermicro have actively incorporated the Instinct platforms into their operations.

The Zacks Consensus Estimate sets first-quarter Data Center revenues at $3.4 billion, reflecting a significant year-over-year increase of 47.5%.

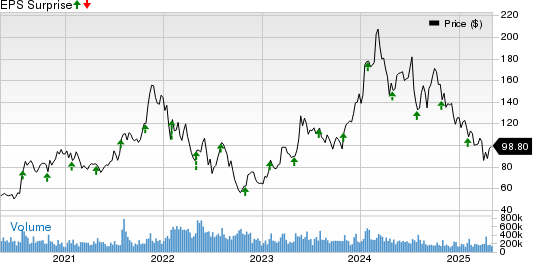

AMD’s Price and EPS Surprise

This graphic illustrates AMD’s price-eps-surprise.

Expanding Portfolio to Fuel Client Revenues

AMD’s growing product lineup and diverse partnerships are key drivers for the client segment revenues.

It is expected that AMD will observe continued growth in its client business, propelled by increased demand for AMD Ryzen processors across desktop and mobile devices.

Moreover, collaborations, like the one with Dell Technologies for Ryzen Pro processors in commercial PCs, are predicted to contribute significantly to growth in this segment for the upcoming quarter.

The Zacks Consensus Estimate for first-quarter Client segment revenues stands at $2.04 billion, indicating a year-over-year increase of 49.34%.

Anticipated Decline in Gaming and Embedded Segments

The Gaming segment is expected to see a decline in the first quarter of 2025, primarily due to a reduction in semi-custom sales as major partners cut back on channel inventory. This trend is anticipated to lead to a year-over-year decrease in revenues.

The consensus estimate for Gaming revenues is set at $570 million, reflecting a considerable 38.1% decline.

Furthermore, the Embedded segment is also projected to be impacted by ongoing challenges in the industrial and communication markets. The Zacks Consensus Estimate for first-quarter Embedded revenues is expected to be $838 million, indicating a 0.9% decline compared to the previous year.

Analysis from the Zacks Model

According to the Zacks model, a positive earnings ESP combined with a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) increases the likelihood of an earnings beat. This scenario aligns with AMD.

Currently, Advanced Micro Devices has an earnings ESP of +0.74% and holds a Zacks Rank of #3.

Stocks to Watch

Here are some companies that might outperform in their upcoming earnings reports, based on Zacks’ model:

Affirm (AFRM) has an earnings ESP of +63.27% and a Zacks Rank of #1. Affirm shares have declined by 14.1% year-to-date and will release its third-quarter fiscal 2025 results on May 8.

StoneCo (STNE) boasts an earnings ESP of +6.25% and also holds a Zacks Rank of #1. StoneCo shares have surged 72.8% year-to-date and are set to report its first-quarter 2025 results on May 8.

Baidu (BIDU) presents an earnings ESP of +8.67% and holds a Zacks Rank of #2. Baidu shares have increased by 6.7% year-to-date, with first-quarter 2025 results scheduled for May 21.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.