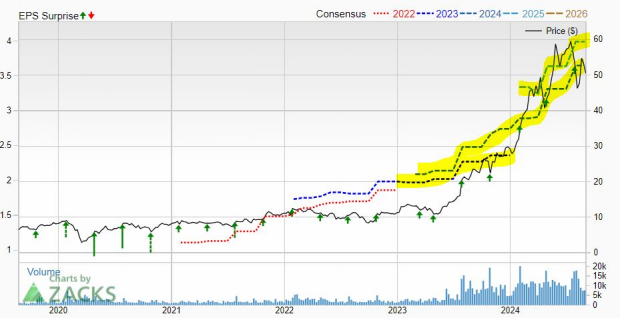

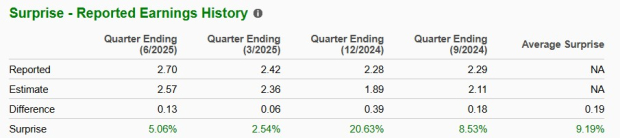

Ferrari N.V. (RACE) reported a strong second-quarter performance for 2025, with revenues reaching €1.66 billion, a 12% year-over-year increase. The increase was driven by higher deliveries and effective pricing strategies. The company’s EPS was $2.70, exceeding the consensus estimate of $2.57. Forward EPS estimates for 2025 rose from $9.60 to $10.41, and for 2026, from $10.81 to $11.74.

In Q2, hybrids accounted for 58% of shipments, a significant increase from 43% the previous year. The company maintains a low-volume production strategy of under 15,000 units annually and has a two-year order backlog. Additionally, about 12% of quarterly revenues, roughly €200 million, now stem from brand-related activities, reflecting a diversification strategy that includes licensing and merchandise.

Ferrari’s EBITDA margin hit 38.3% in Q2, supported by a high-margin personalization program that comprises 20% of revenues. The stock has gained 5% in 2023, outperforming the nearly 9% drop in the broader auto sector, with analysts seeing continued growth potential.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.