“Value investment” and “Magnificent Seven” rarely share the limelight. The Magnificent Seven, a formidable group of megacap growth stocks, have commanded the market since the dawn of 2023. This stellar ensemble comprises Microsoft, Apple, Nvidia, Amazon, Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), Meta Platforms, and Tesla.

However, nestled within this elite cadre lies an unexpected gem of a value investment: Alphabet. Possessing all the quintessential traits of a value play while exuding the vigour of a growth enterprise, Alphabet stands at the crossroads of opportunistic investing. A convergence of two pivotal investing philosophies can pave the way for substantial returns provided the company stays nimble.

In light of Alphabet’s illustrious past, there is a strong belief that it may emerge as the cream of the crop among the Magnificent Seven – a dark horse indeed.

Alphabet’s AI Odyssey: A Path Less Trodden

Alphabet’s reputation often precedes it, with flagship products like Google, YouTube, and Android defining its public persona. At the heart of its operations lies an advertising colossus, responsible for 76% of its revenue in the fourth quarter.

Yet, Alphabet’s recent narrative has been hijacked by tales of artificial intelligence (AI) missteps. Despite CEO Sundar Pichai’s bold proclamation of Alphabet as a paragon of AI-led innovation, tangible outcomes are yet to materialize. OpenAI trumped Alphabet by unveiling ChatGPT, the maiden generative AI titan. Alphabet, playing catch-up with its Bard model, stumbled during a demo by furnishing an erroneous response. In a subsequent fiasco, rebranded as Gemini, the model’s image-generation feature produced grotesquely inaccurate images, vexing users.

The specter of Alphabet slumbering through the AI renaissance looms large, accompanied by dire predictions of AI model inaccuracies impinging on its advertising hegemony, potentially coercing advertisers to seek greener pastures. Given Alphabet’s profound reliance on ad revenue, this perceived vulnerability could potentially deal a crippling blow to the tech giant.

Nevertheless, these trepidations, somewhat exaggerated, fail to encapsulate Alphabet’s true potential.

Over the years, Alphabet has meticulously amassed its engineering arsenal, equipped with the acumen to realize its ambitions. While the fruits of these endeavors may take time to ripen, the present juncture presents an alluring opportunity to partake in Alphabet’s journey, a journey that is unlikely to fade into oblivion quietly.

Alphabet’s Arsenal for Triumph: Financial and Strategic

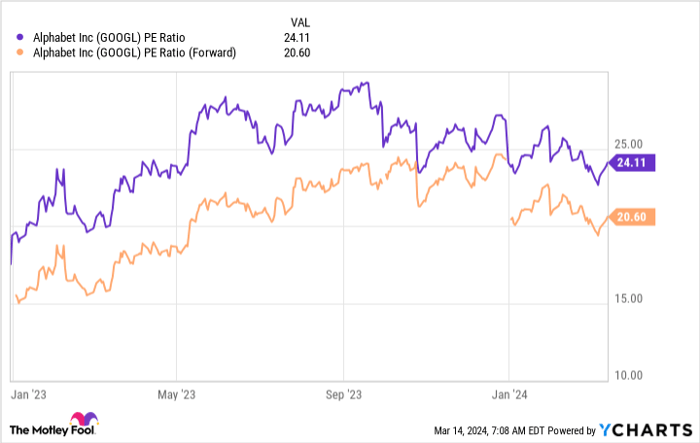

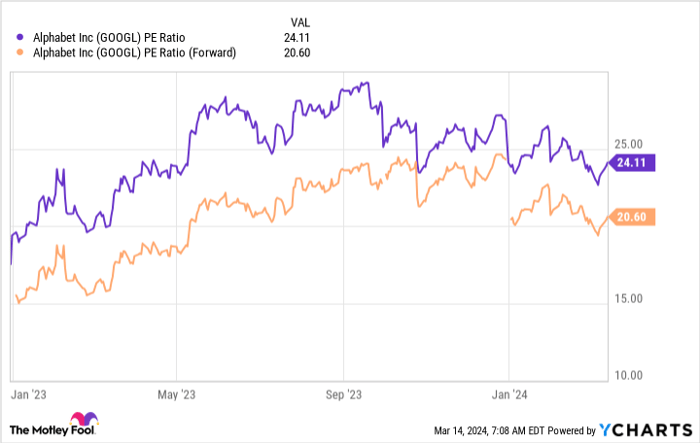

Alphabet’s recent missteps have nudged its forward price-to-earnings (P/E) ratio slightly below the S&P 500’s average ratio.

GOOGL PE Ratio data by YCharts.

While the S&P 500 trades at 23.2 times trailing earnings and 21.1 times forward earnings, Alphabet’s valuation hovers around the market average. However, a peek into its financial reserves unveils a divergent narrative.

During Q4, Alphabet witnessed a 13% surge in revenue year over year. Concurrently, its operating margin ascended by 3 percentage points to an impressive 27%. These numbers mirror a resurgent ad sector, convalescing post the late 2022 and early 2023 recessionary premonitions.

With a treasure trove exceeding $110 billion in cash and equivalents adorning its balance sheet, Alphabet is poised for strategic moves. Unfettered by debt, it could hypothetically acquire entities like Airbnb, Lockheed Martin, or Deere & Company at their present market capitalizations. Alternatively, a fraction of this war chest could be deployed to procure an AI startup, augmenting Alphabet’s AI prowess.

Although AI poses a distinct challenge, Alphabet’s profound resources leave little room for doubt regarding its ability to birth a triumphant product. It’s merely a matter of time.

My conviction in Alphabet’s dual value and growth persona positions it as a premier pick in my investment lexicon.

Is allocating $1,000 towards Alphabet prudent at this juncture?

Before plunging into Alphabet’s stock, a moment of reflection beckons:

The esteemed analyst team at Motley Fool Stock Advisor, having identified what they posit as the 10 optimal stocks for the contemporary investor, excluded Alphabet from the coveted roster. The selected decathlon is purported to furnish titanic returns in the foreseeable future.

Stock Advisor proffers a navigational compass for investors’ success, embellished with potent advice on portfolio construction, periodic insights from analysts, and bimonthly stock recommendations. Since 2002, the Stock Advisor service has trounced the S&P 500 return thrice over*

Discover the 10 Stocks

*Stock Advisor returns as of March 11, 2024

Suzanne Frey, an executive at Alphabet, sits on The Motley Fool’s board of directors. Randi Zuckerberg, former market development director and spokesperson for Facebook, sister to Meta Platforms CEO Mark Zuckerberg, also graces The Motley Fool’s board. John Mackey, erstwhile CEO of Whole Foods Market, an Amazon subsidiary, is also a member of The Motley Fool’s board. Keithen Drury holds positions in Airbnb, Alphabet, Amazon, Meta Platforms, and Tesla. The Motley Fool boasts stakes in and recommends Airbnb, Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool advocates for Deere & Company and Lockheed Martin while suggesting options like long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool maintains a disclosure policy.

The views and opinions expressed herein solely represent the author’s voice and may not necessarily mirror those of Nasdaq, Inc.