“`html

Welcome to the New Year!

To celebrate the start of 2025, we present our take on the 10 most significant charts from our blogs in 2024.

Throughout the past year, we explored various topics, including options trading, short selling, latency issues, and enhancing market conditions for issuers and investors.

Let’s dive into our countdown, beginning with number 10:

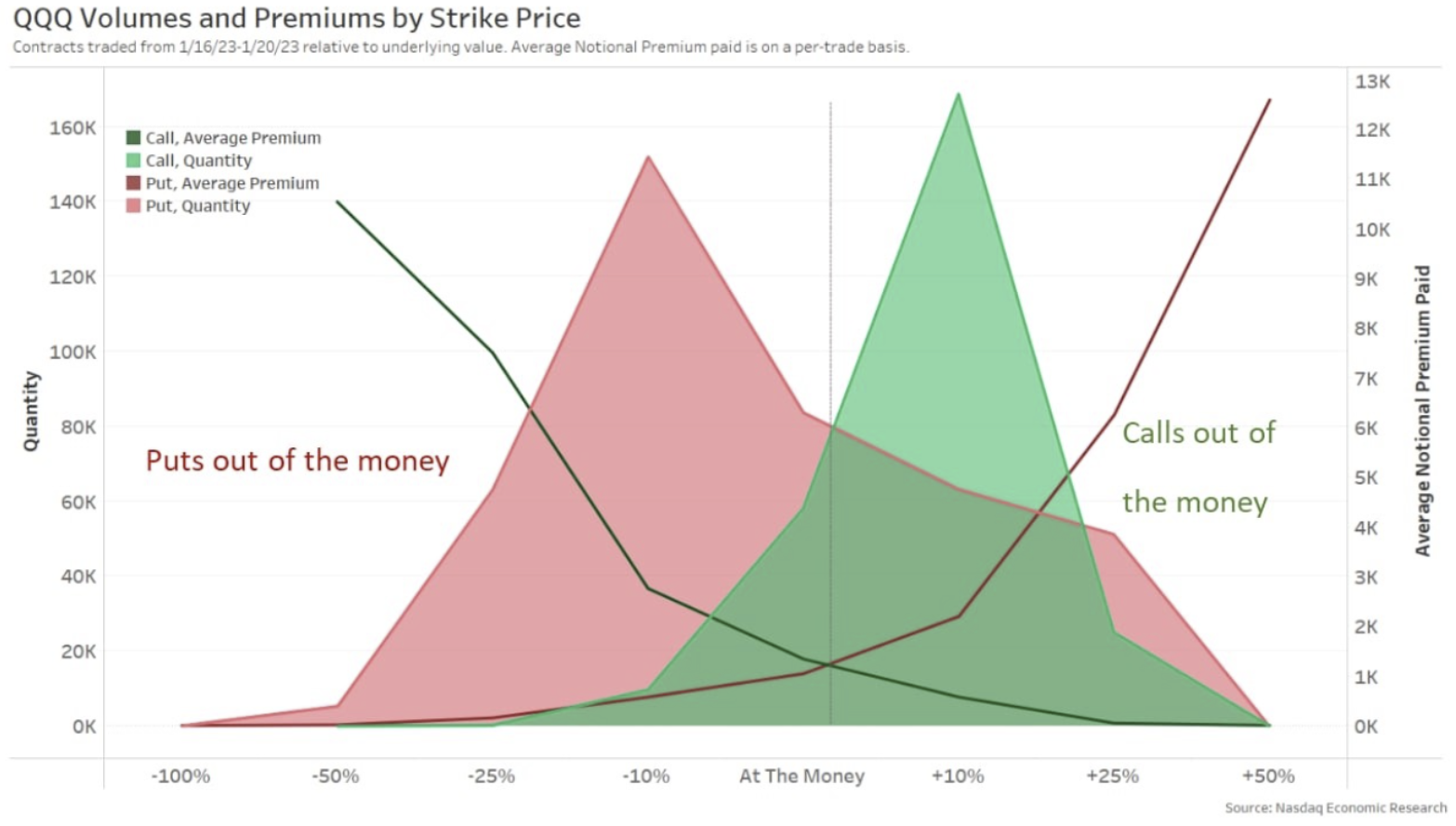

10. Interns’ Guide to Options Trading

In 2024, we expanded our summer interns’ guides to include a comprehensive overview of options markets. This new guide covered essential concepts such as option payoffs, liquidity in U.S. options markets, and the expiration details of each option. A helpful table demonstrated the differences between options that expire at market open versus those at market close, alongside the distinctions between physical delivery options.

A notable chart illustrated the “moneyness” of traded options. It revealed that most options are traded when they are “out of the money,” which lowers their premium costs. As a result, the necessity for market makers to hedge reduces since the likelihood of exercise is less. This observation highlights that aggregating “options notional value traded” does not accurately reflect the liquidity of underlying stocks, given that actual exposures and hedging are significantly lower than a 1-to-1 basis.

Chart 10: Majority of Options are Traded “Out of the Money”

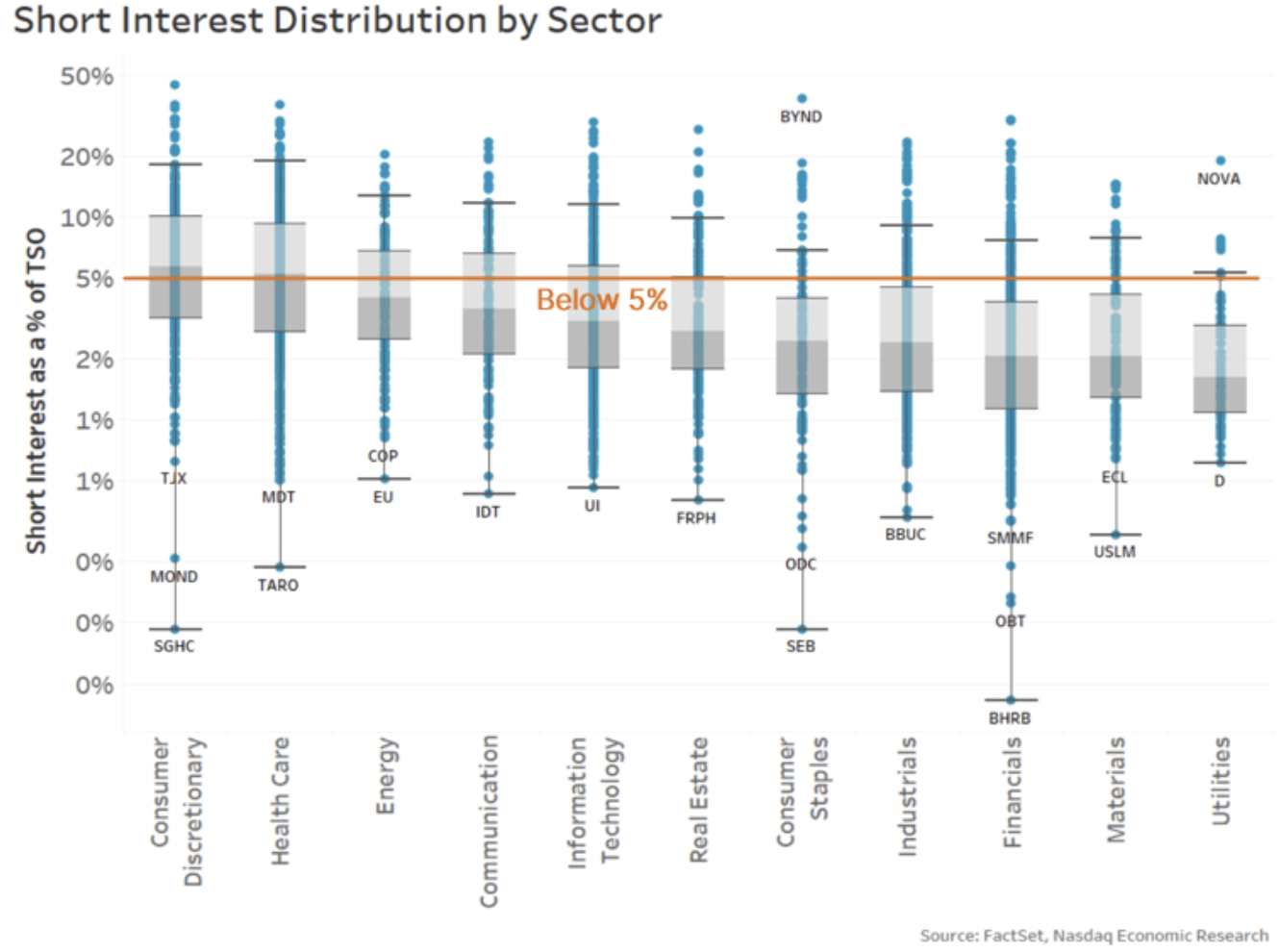

9. Understanding Short Interest in the Market

Falling stock prices typically lead to frustration among investors and companies alike, often resulting in blame directed toward short sellers. However, our 2024 blog clarified some aspects of this common perception.

While a significant number of trades may carry a “short sell” designation, actual short interest levels in the market remain relatively stable and lower. The accompanying chart confirms that most stocks have less than 5% of their shares held short, indicating that most short-selling activities originate from “bona fide market makers.” These market makers are obligated to buy and sell throughout trading sessions, without necessarily adopting directional positions.

Additionally, regulations require stocks to be borrowed before settlement, ensuring that buyers receive the stocks they purchased from short sellers. Data suggests that trade failures are infrequent, with most occurrences linked to smaller retail trades.

Chart 9: Most Stocks Have Less Than 5% of Shares Shorted

Research has repeatedly shown that short selling contributes positively to market efficiency, facilitating hedging and cross-market arbitrage, which helps ensure fair pricing in Futures and ETFs and tightens stock spreads.

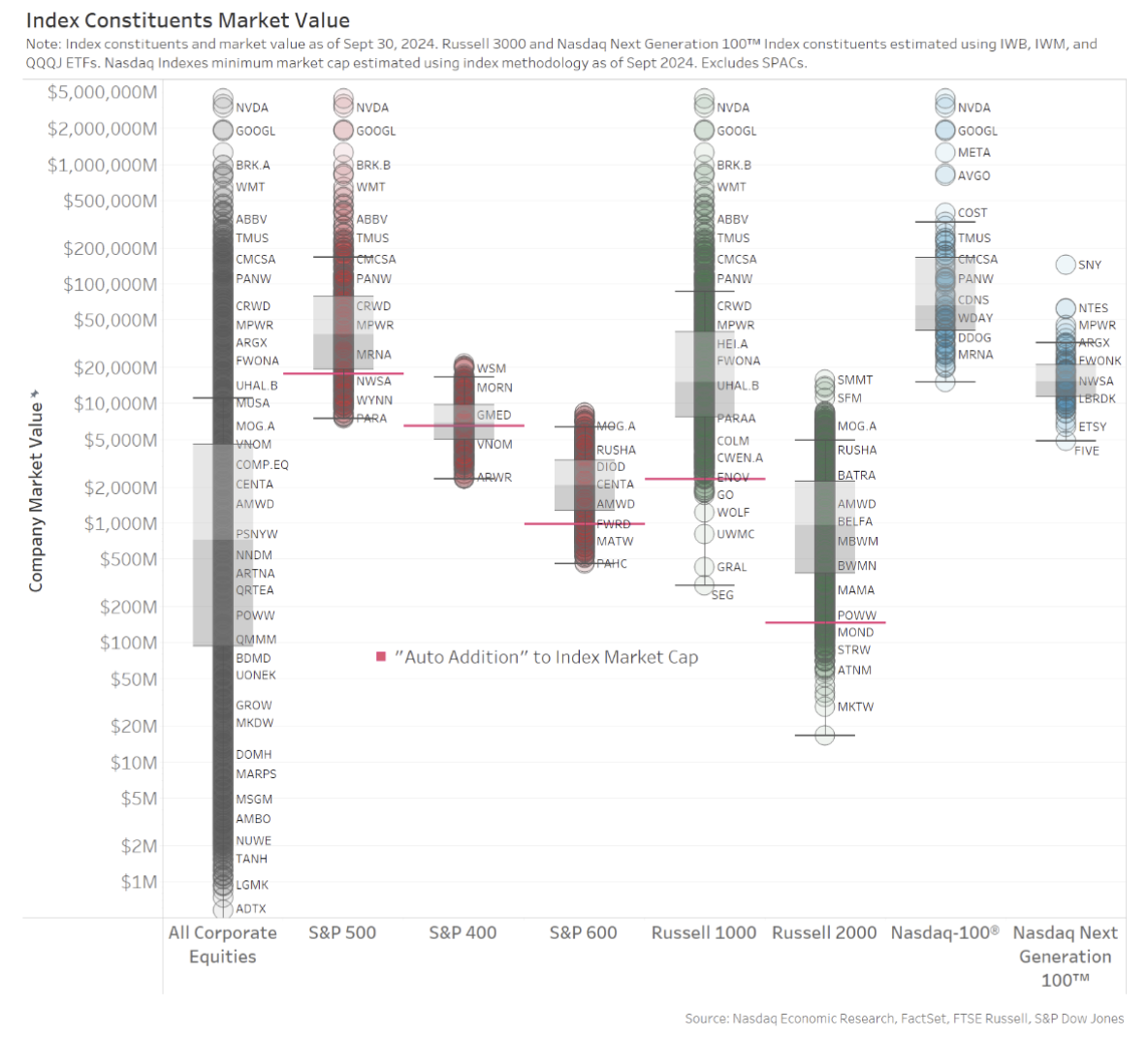

8. The Definition of Small-Cap Stocks Varies by Index Provider

Discussions around large-, mid-, and small-cap stocks often imply a clear categorization of companies. However, our findings revealed significant variability depending on the index provider. Our favored chart demonstrated that some small-cap stocks may exceed the size of the smallest large-cap stocks, a discrepancy influenced by annual price changes and strategic decisions to minimize turnover and trading costs for index fund managers.

Chart 8: Small-Cap and Large-Cap Stocks According to Different Index Providers

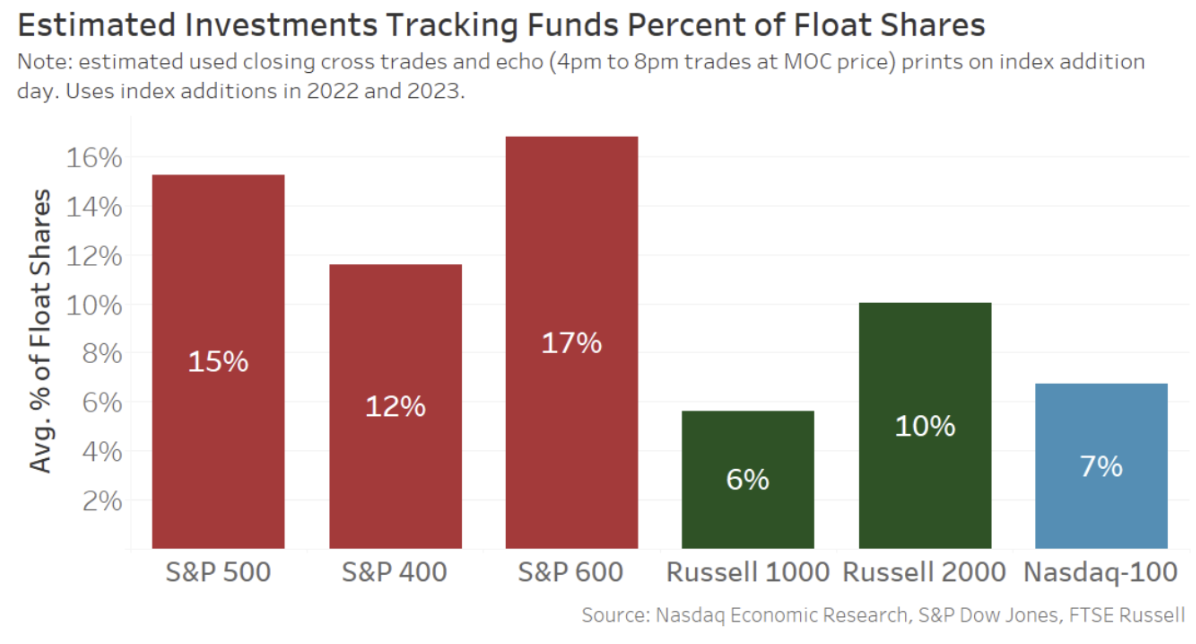

7. Analyzing Index Trades for Tracking Insights

The popularity of index funds and ETFs has surged in recent years. Our examination focused on the volume of a company’s available shares traded during the close on the day of index inclusion.

The findings were insightful, revealing that the market can offer substantial liquidity during closing trades to accommodate index demands. Notably, even as the popularity of index funds grows, the associated liquidity costs have decreased.

Chart 7: Significant Liquidity Absorption at Index Rebalance Dates

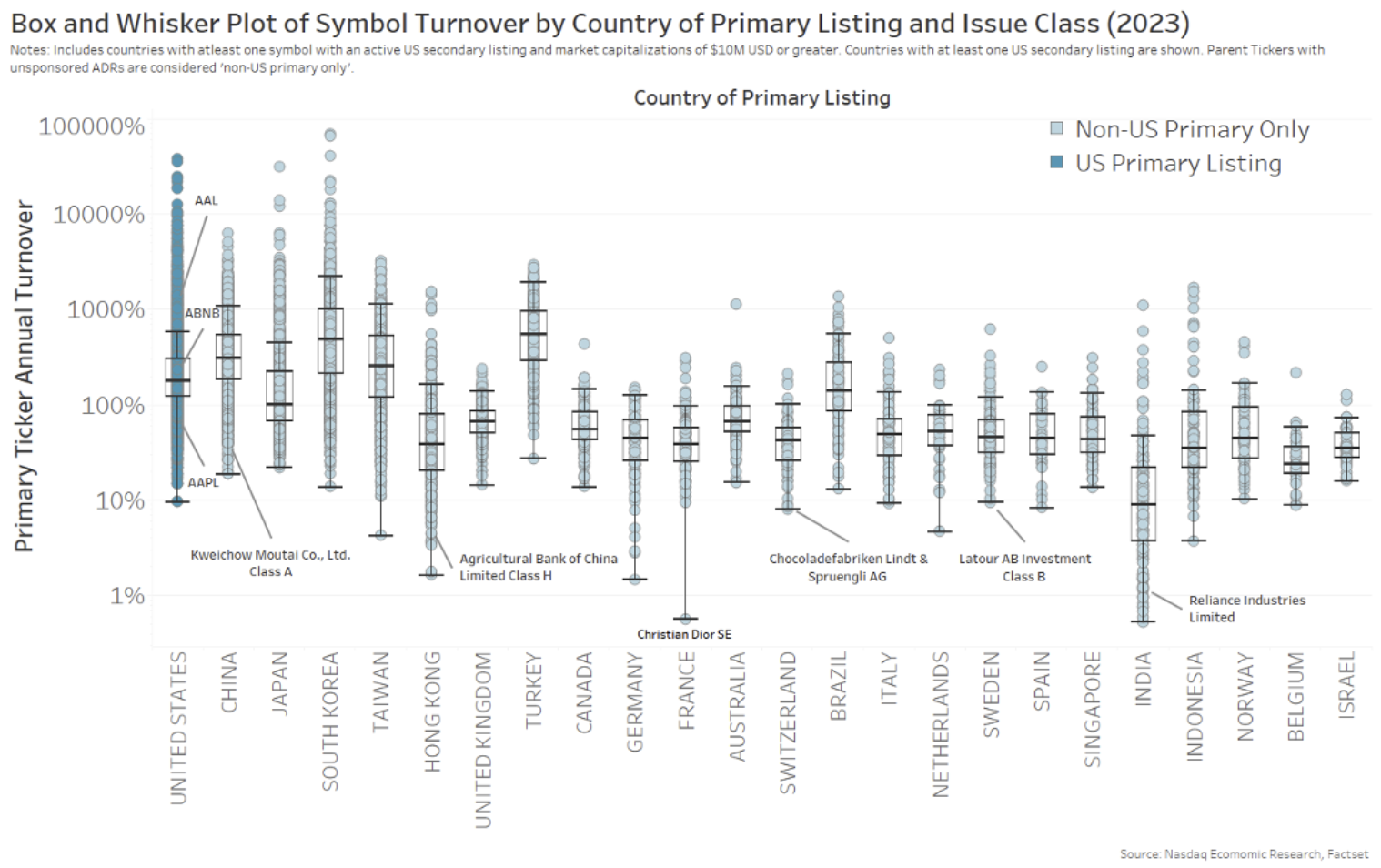

6. Is the U.S. Truly the Most Liquid Market Worldwide?

The U.S. is often recognized as the most cost-effective and liquid equity market globally. However, with approximately 6,000 U.S. companies listed compared to under 900 in France, is this an equitable comparison?

To provide a clearer picture, we calculated the “market-cap turnover” for each company, which measures how frequently total available shares trade annually. This metric considers variances in share prices and market caps internationally.

The results of this analysis were surprising; while U.S. liquidity remains strong, it is not the highest. Notably, several Asian markets, recognized for robust retail participation, demonstrated even greater liquidity on average. However, liquidity figures for larger developed markets in Asia have dragged the overall regional average below that of the U.S.

Chart 6: Annual Market-Cap Turnover by Country

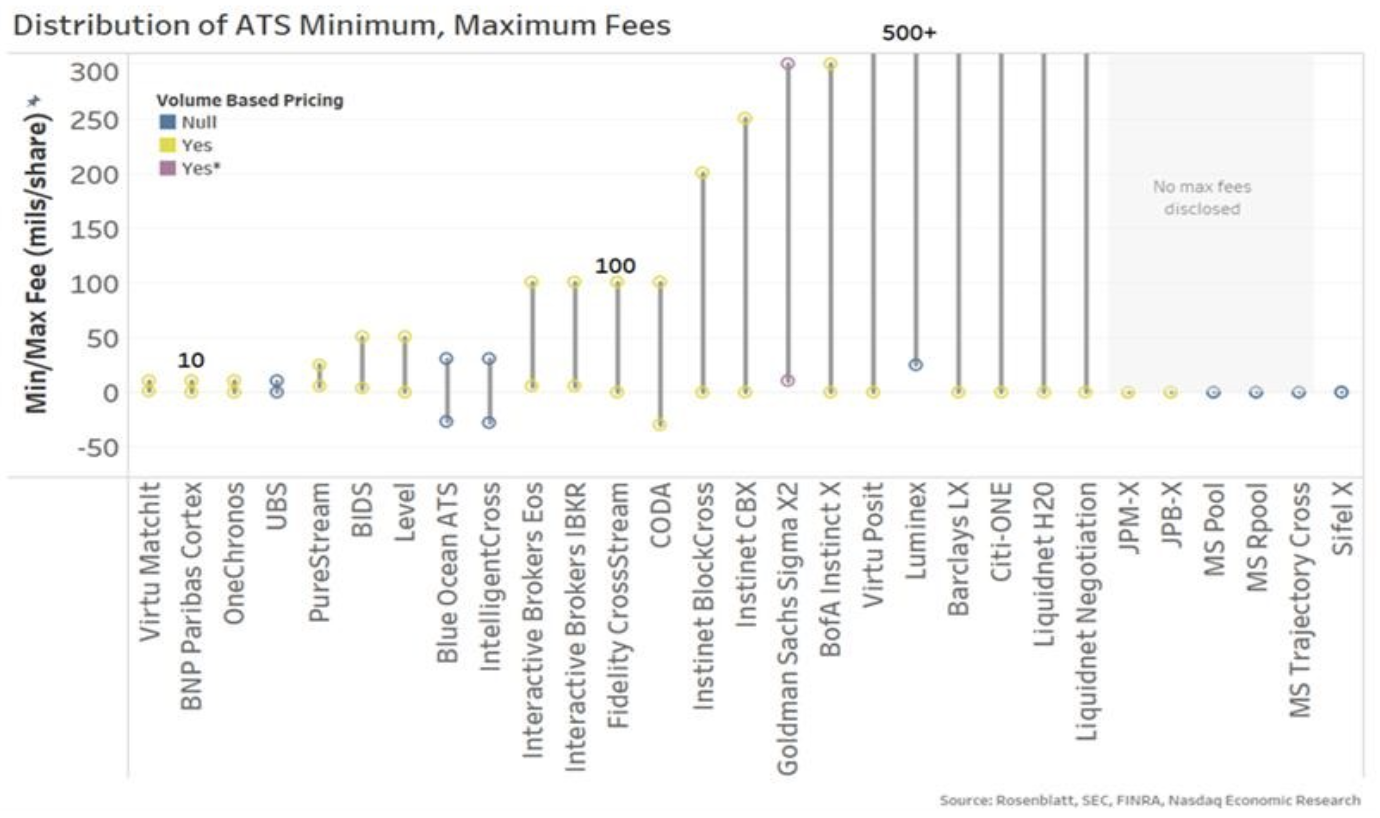

5. Exchange Fees and Alternative Trading Systems Differ Significantly

In 2024, the U.S. Securities and Exchange Commission (SEC) was notably active, finalizing several new rules, some targeting exchange fees. These included reductions in access fees and the removal of volume discounts for active traders.

This regulatory focus on exchanges is notable, especially as off-exchange trading consistently surpassed the 50% mark, a threshold viewed as critical for maintaining market quality and ensuring a meaningful National Best Bid and Offer (NBBO) that protects investors.

By concentrating on exchange fees, the SEC may have overlooked the evolving economic landscape of the “other half” of the trading market.

“`

The Complex Reality of Market Fees and Latency in Trading

The question of fairness in market fees reveals a clear disparity. The rates for SIP, which include volume discounts, differ significantly from the SEC’s varied annual budget recovery methods. This disparity reflects a broader difference between access to exchanges versus alternative trading systems (ATSs).

On the other side of the trading spectrum, the economic landscape is distinct. Instead of the equal access the SEC aims for on exchanges, trading in ATSs tends to be bilateral and bundled. This setup creates customer quality tiers and segmentation that contributes to higher trading fees. As illustrated in the chart below, ATSs charge fees spanning from “free” to amounts exceeding the current exchange fee cap.

In this context, it’s evident that “ten” is not the norm, and the fees in the market cannot be considered “equal.”

Chart 5: Form ATS-N highlights the intricacies of market pricing across various venues

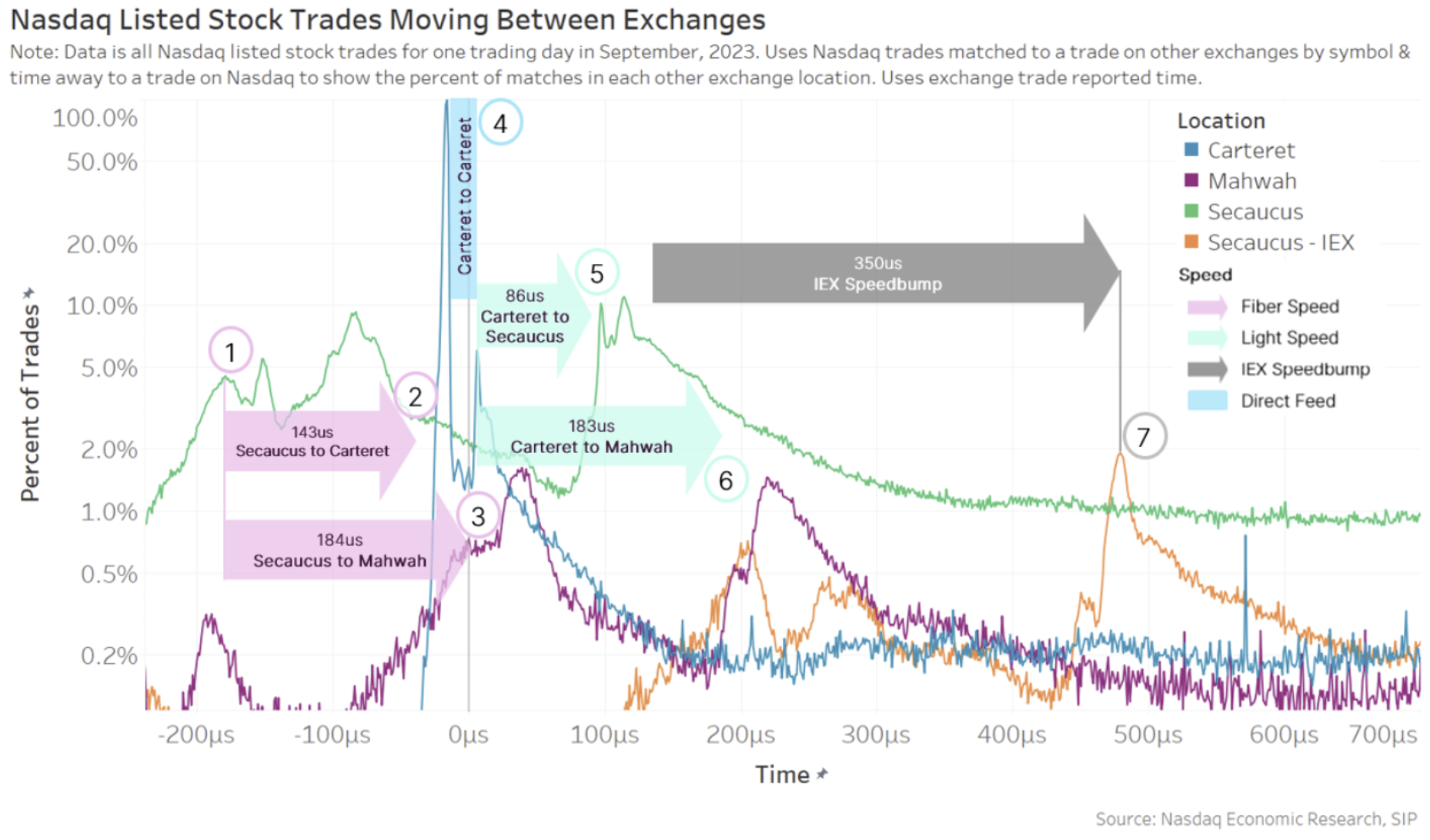

4. The Impact of Latency: A Millisecond Matters

Years back, the SEC introduced a “de minimis” rule to legitimize IEX’s speed bump market. Ironically, they rejected a similar proposal from Cboe, despite its small latency difference. Over time, the SEC utilized this rule to endorse IEX’s D-limit, which features fade-able yet protected lit quotes, but overlooked its relevance for SIP latency considerations.

This backdrop is crucial when analyzing trading latency in our 2024 study. Our previous blog discussed how, even at light speed, trades take time to travel across the U.S. marketplace, resulting in minute delays and reactions.

Our analysis revealed that many trades initiate from Secaucus, where broker algorithms are centered. These orders move swiftly at fiber speed (indicated by pink arrows), while fills trigger reactions at microwave speeds (as shown by green arrows), ultimately culminating in trading at IEX after passing through their speed bump.

Even with IEX’s speed bump, this entire process takes under one millisecond.

Chart 4: Trade responses in the U.S. market unfold in less than a millisecond

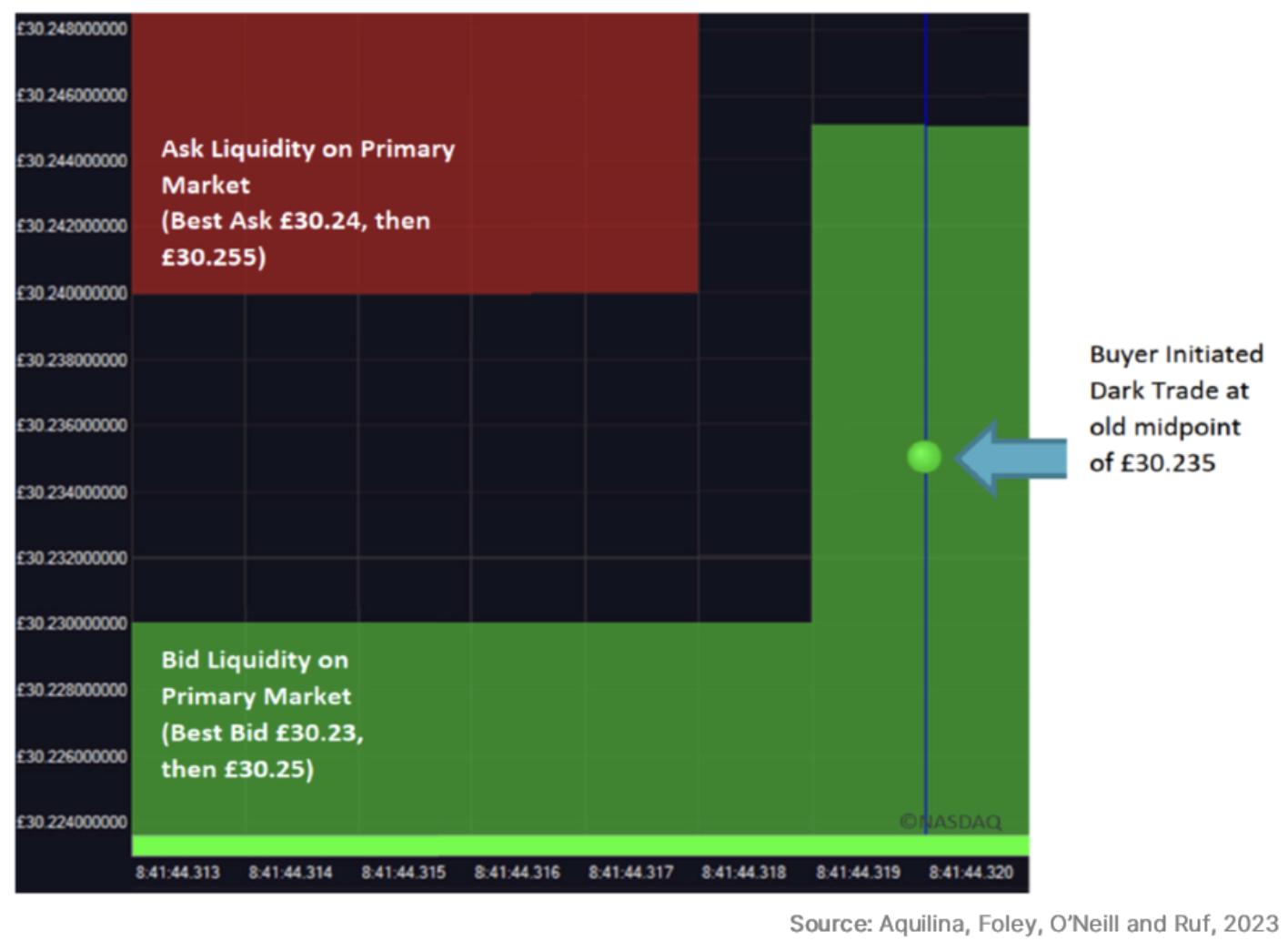

3. Insights into Latency Arbitrage in London

The latency phenomenon mentioned previously introduces discussions of latency arbitrage. A new academic study explores this in London’s dark pools, where orders align with exchange quotes. The most insightful chart from that blog illustrates that:

- The exchange bid increases (depicted in green).

- A fill occurs in a dark pool at the “old midpoint.”

This discrepancy arises because fast arbitrageurs can execute trades over microwave connections, while exchange quotes move along optic fiber at a slower speed. The study revealed a high occurrence of stale trades in dark pools with arbitrageurs winning more than 96% of the time by buying at older midpoints and selling at current prices in primary markets.

Chart 3: Dark pool fills at outdated midpoints due to latency

Similar findings have emerged across Europe, backed by research from Euronext, SIX Swiss, and Deutsche Börse.

This research bears significant implications for ongoing debates regarding consolidated tape systems in Europe and beyond. Delays are inherent in pricing, and a consolidated tape will always introduce additional lag. Consequently, even competitors recognize that a consolidated tape should not be used for trading, as it fundamentally cannot operate pre-trade.

This research also sheds light on the market structure, suggesting that fragmentation reduces fill probabilities for dark pool customers, ultimately leading to wider spreads and reduced market depth.

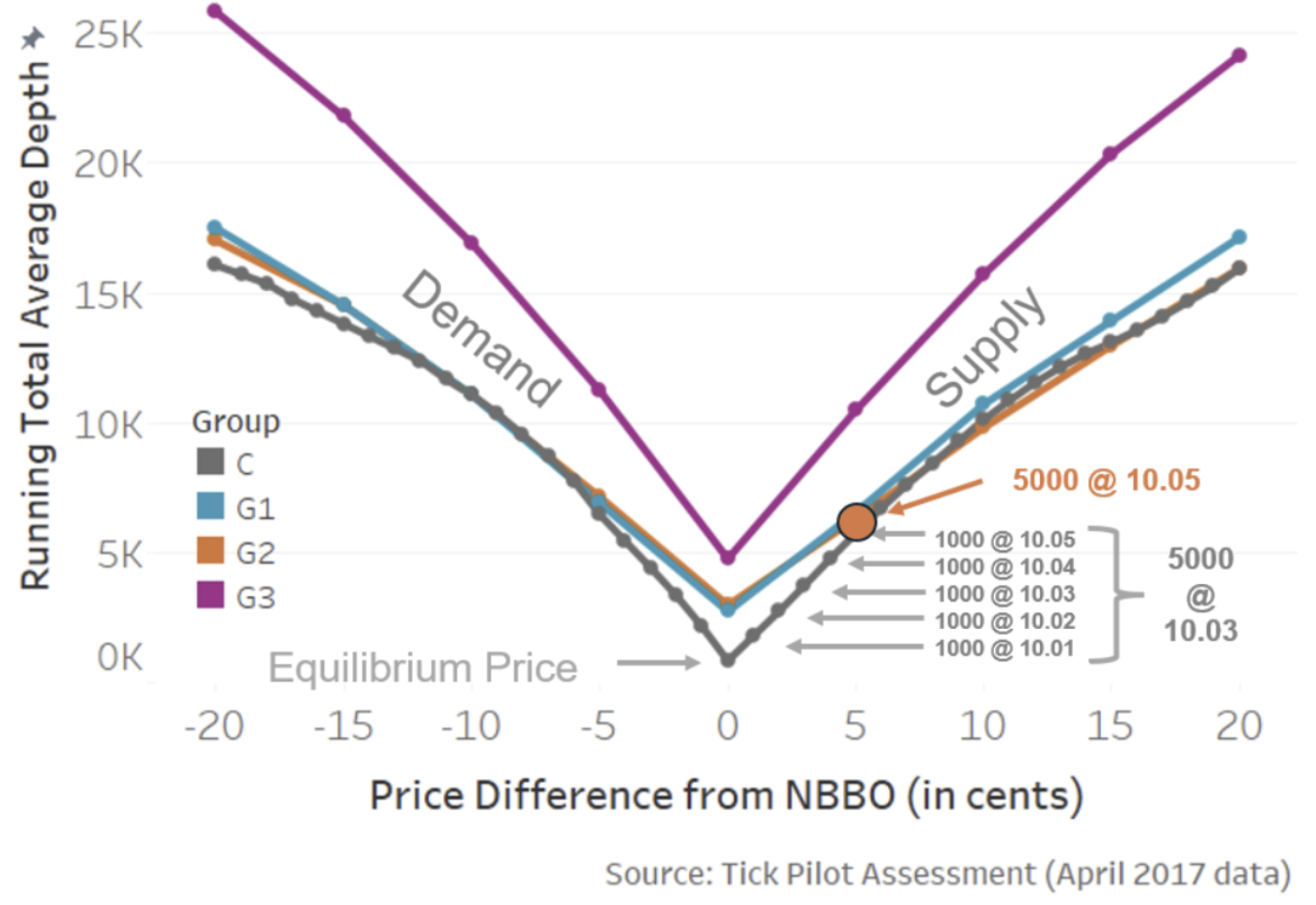

2. The Economics of Supply and Demand in Depth and Spreads

Our analyses, along with academic research, have consistently demonstrated that spreads and market depth are influenced by supply and demand dynamics.

One chart from our research exemplifies this trend:

- Stock supply and demand curves are generally linear.

- Reducing tick sizes in constrained stocks decreases both the spread and market depth, representing a trade-off for investors.

The only scenario leading to simultaneous improvements in spreads and depth occurred through the trade-at group in the Tick Pilot study, where price setters retained their own spreads rather than relying on BBO to execute elsewhere.

Chart 2: Research indicates that efforts to improve spreads often decrease depth; trade-at is key

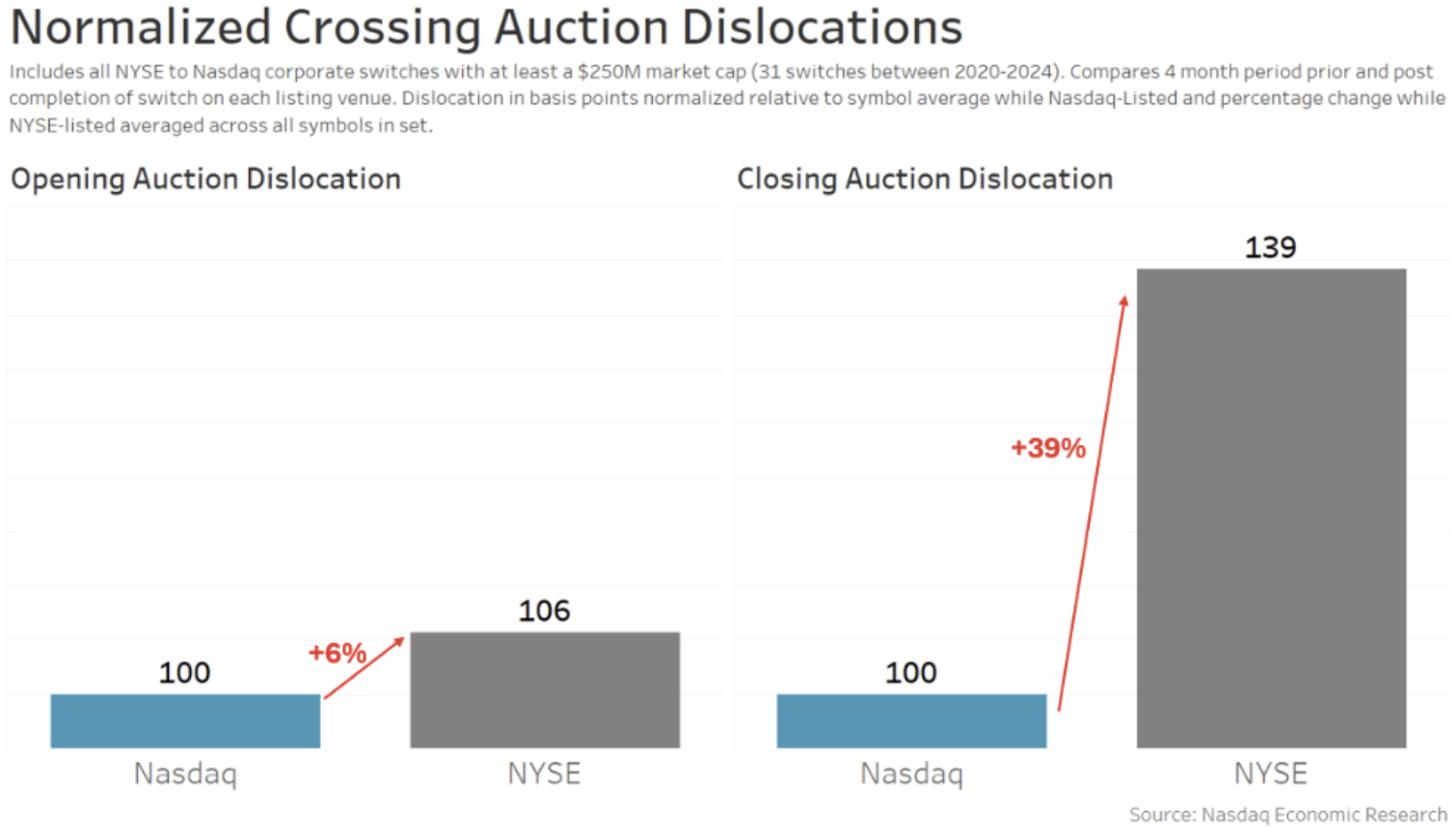

1. Nasdaq’s Strong Position for Issuer Auctions

In 2024, the 500th company transitioned from NYSE to Nasdaq, underscoring Nasdaq’s appeal. In a National Market System (NMS) world, where trading occurs across multiple venues, data analysis indicates that Nasdaq continues to provide superior market quality.

One notable aspect from our blog focused on open and closing auctions, demonstrating how varying auction rules can mitigate stock volatility. This reduction is crucial, as it lowers a company’s cost of capital, spurring further investment and benefiting the U.S. economy.

Chart 1: Reduced auction volatility post-switch to Nasdaq

As we wrap up, we extend our best wishes for a fulfilling and prosperous New Year. We look forward to sharing more insights and observations in 2025.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.