InvestorPlace – Stock Market News, Stock Advice & trading Tips

AI stocks have been on a tear recently, with Nvidia (NASDAQ:NVDA) once again breaking records and crossing above $950 per share. However, as I’ve cautioned many times before, this is a stock that investors need to be very careful with at these levels. While I would not recommend shorting Nvidia, the company does face significant downside risk if the AI rally loses steam. At the same time, there is not a whole lot of upside potential left after the meteoric rise.

Discovering Hidden Gems in the AI Sector

That’s not to say Nvidia couldn’t potentially climb even higher – $1,000 per share or more is certainly possible if the momentum continues carrying it upward. But purely chasing momentum gains above $950 would not be a smart move in my view. Instead, investors should look to more under-the-radar AI stocks that have significant organic growth potential in the coming quarters and years. Here are seven that could trounce Nvidia’s gains next year:

Unveiling GigaCloud Technology’s Promising Future

trading concept. Robotic hand analyzing financial data on stock exchange, artificial intelligence utilization to predict precise price change in stock market. Trailblazing. trillion-dollar ai stocks. AI Stocks with Potential. stocks to buy. Strong Buy AI Stocks”>

trading concept. Robotic hand analyzing financial data on stock exchange, artificial intelligence utilization to predict precise price change in stock market. Trailblazing. trillion-dollar ai stocks. AI Stocks with Potential. stocks to buy. Strong Buy AI Stocks”>

Source: Owlie Productions / Shutterstock.com

At first glance, GigaCloud Technology’s (NASDAQ:GCT) name may seem a bit misleading. That’s because this is not actually a cloud computing company at all. Instead, GCT operates a B2B marketplace connecting buyers and sellers of furniture and other large goods. The company also provides logistics intelligence services, which I believe puts it squarely in the AI sector as well. Moreover, furniture and related companies have seen significant downtrends in their businesses lately that could be poised for a breakout rebound in the coming months.

GCT’s recent results have been stellar. The company has increased its revenue by 95% to $245 million and net income rose by 185% to $35.6 million. Looking ahead, revenue is expected to rise above $1 billion in 2024 alongside 50% year-over-year growth. Earnings per share should hit $2.6 this year. EPS is then forecasted to reach $4.2 in 2026, alongside revenue hitting $1.6 billion. In exchange for this tremendous growth, you’re paying just 11 times forward earnings and 1 times forward sales – extremely cheap valuations for a high-growth software company. I don’t believe the $402 million debt load changes this thesis either, as GCT generates significant cash flow and has $243 million in cash to help offset it.

Since I first covered this stock in an article last year, the share price has more than doubled. The recent correction looks to me like a prime entry point for the next leg up in this exciting AI play. While not yet a household name, GigaCloud Technology has all the ingredients for huge returns if execution remains strong.

Continuing Upstart’s Momentum

Source: T. Schneider / Shutterstock.com

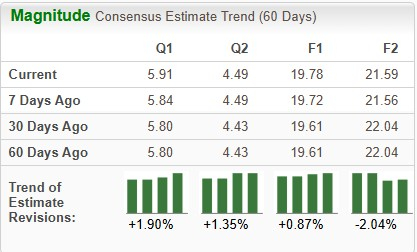

Upstart’s (NASDAQ:UPST) stock price was up nearly 400% at one point since I first touted the AI lending platform back in early 2023. While the stock has given back some gains and is now up around 100% since then, I stand by my initial bullish call. I continue to believe Upstart can climb much higher over the long term.

Most of Upstart’s challenges lately stem from banks facing pressures and taking fewer risks. With economic uncertainty high, banks are hesitant to try new technologies like Upstart’s platform. Moreover, consumers have delayed major purchases for the past two years amid rising rates, and cratering demand for loans. However, I expect the tide to turn as the Fed pivots to rate cuts, spurring more borrowing activity. This should significantly benefit Upstart as banks again need credit risk capabilities.

Looking out, I see revenue potentially topping $1 billion in 2026, alongside expanding profitability. EPS could hit $1 that year, and some analysts estimate as high as $1.26. If achieved, that kind of income growth at reasonable valuations would send the stock soaring. While the path may be bumpy depending on the economy, I remain confident in Upstart’s innovative AI over the long run.

Unveiling the Potential in T Stamp’s AI Solutions

Source: everything possible / Shutterstock.com

T Stamp (NASDAQ:IDAI) is one of the more smaller AI stocks, with its modest size allowing for potentially huge returns if the business takes off. IDAI provides identity authentication software solutions using AI-powered biometrics, cryptography, and data mining. Their tech aims to predict identity/trustworthiness, prevent fraudulent attacks, and protect sensitive user data.

Coverage and forecasts on IDAI are limited given its nano-cap status. However, I view the stock as a worthwhile gamble at around 90 cents per share after falling close to its July 2023 floor price. Revenue grew 127% year-over-year to $3 million last quarter. Its market cap sits at just $8.3 million currently. My biggest worry is the cash burn, likely requiring some dilution before reaching profitability. But if IDAI gains traction, the upside in this cybersecurity play could be enormous.

Exploring AmpliTech Group’s Path to Growth

Source: Shutterstock

AmpliTech Group, Inc. (NASDAQ:AMPG) is a technology company designing, engineering, and assembling microwave component-based amplifiers. Their products include radio frequency (RF) amplifiers and related subsystems used in communication systems like Wi-Fi, radar, satellite, and cell phones.

This is not directly an “AI” firm, but AMPG does employ AI in many operations, as most companies do today. What matters is they are in high-tech sectors with solid growth runways. However, stellar financials are lacking currently. Revenue is expected to dive to $15.6 million in 2023 from over $19.4 million in 2022, alongside expected reversion to unprofitability.

So why do I view AMPG as a promising buy? The future looks bright. The company should deliver triple-digit growth in 2024, propelling revenue to $32 million and EPS back into positive terrain. The 2024 revenue estimate puts the stock at a mere 0.6 times sales, very inexpensive. I believe this could catalyze a breakout above $2. If execution goes smoothly, 2024 could mark the start of a high-growth, profitable period for AMPG.

Examining the Potential of Klaviyo’s AI Expansion

Revolutionizing the Market: Innovating Companies to Invest In

Turnkey Marketing Automation with Klaviyo (KVYO)

Klaviyo (NYSE: KVYO) is a force to be reckoned with in the marketing automation realm, serving a vast clientele of over 143,000 companies worldwide. The platform excels in real-time activation of customer data for tailored email, SMS, mobile push, and reviews.

Companies like Klaviyo, centering around marketing and customer relations software, often command premium valuations. The market buzzes as analysts predict substantial growth in EPS from 45 cents to 73 cents by 2026 and revenue soaring from $893 million to $1.5 billion by 2027. Though trading at a lofty 57 times forward earnings, the potential for growth seems justifiable.

Encouragingly, robust EPS surprises of 78.5% and 15% in Q3 and Q4, coupled with revenue surprises of 5.2% and 2.8%, spark optimism for Klaviyo investors. With a trajectory of continued outperformance, the promise of significant gains over the next few years appears tantalizing if the company maintains its edge in execution.

Automation Ascendancy with Symbotic (SYM)

Symbotic Inc. (NASDAQ: SYM) spearheads the drive toward greater operational efficiencies within contemporary warehouses and supply chains, leveraging automation technology. As technology infiltrates blue-collar domains, Symbotic paves the way by streamlining warehouse operations.

Positioned at a premium of 26 times book value, SYM reflects the market’s anticipation of future needs. Projections hint at impressive growth, with EPS poised to surge from 18 cents in 2024 to 87 cents in 2026, and revenue scaling from $1.74 billion to $3.5 billion. Looking ahead, the company may warrant an even higher premium as automation adoption accelerates.

AI-Powered Excellence at Lumine Group (LMGIF)

A shining star born from the loins of Constellation Group (OTCMKTS: CNSWF), Lumine Group (OTCMKTS: LMGIF) steers the ship in communications and media software, blending in artificial intelligence for a robust product lineup. Post the acquisition of Neural Technologies in 2021, Lumine Group’s inertia has seen it skyrocket, clocking in a staggering 130% surge post its spin-off.

With an estimated average annual revenue growth of around 50% over the next 3-5 years, LMGIF showcases considerable potential. Despite apparent losses, a closer look reveals a decline in net loss in 2023 largely attributed to a valuation increase in redeemable preferred and special securities. Analysts foresee significant profit upticks on the horizon, bolstered by rapid top-line expansion.

If Lumine Group fortifies its AI-driven offerings and sustains its momentum, the future appears bright. Bearing the standard in a lucrative market segment, the company stands poised to secure a stronghold through iterative innovation. The growth narrative seems compelling as of the moment.

More From InvestorPlace

The post 7 AI Stocks That Will Trounce Nvidia’s Returns in 2025 appeared first on InvestorPlace.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.