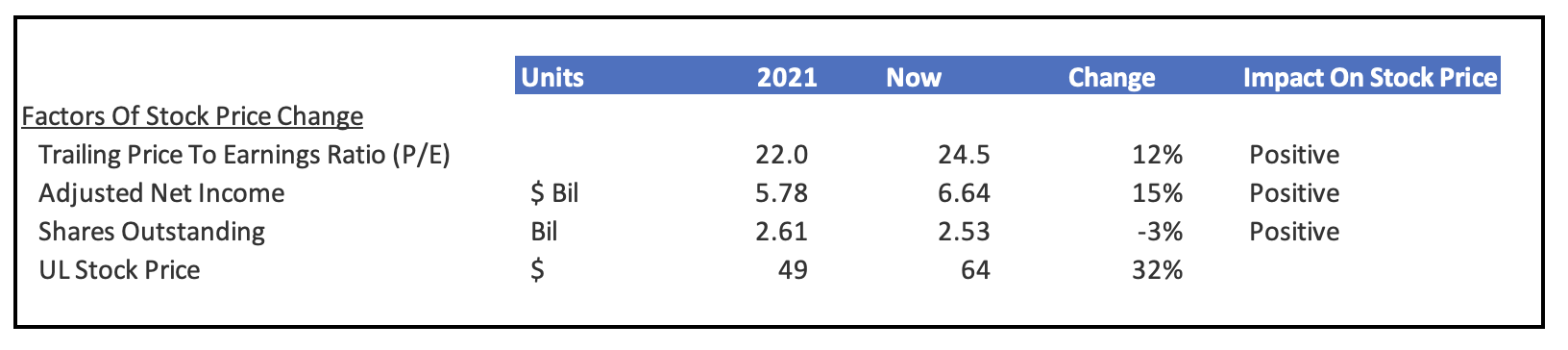

Unilever stock (NYSE: UL) has gained 32% in value since early January 2022 – jumping from levels of $49 then to $64 now – vs. an increase of about 18% for the S&P 500 over this period. This can primarily be attributed to a 12% rise in the stock’s P/E ratio from 22x in 2021 to 24.5x now. Furthermore, the company’s net income grew 15% from $5.8 billion to $6.6 billion over the same period. Profit growth was driven by higher sales and margin expansion. Investors have rewarded UL stock thanks to the uptick in its profitability. Our dashboard on Why Unilever Stock Moved has more details.

UL stock has had a poor run, with the stock losing value in each of the last three years. Returns for the stock were -8% in 2021, -3% in 2022, and 0% in 2023. The growth in UL stock was primarily seen in 2024, with YTD gains of 36%. In contrast, the Trefis High Quality (HQ) Portfolio, with a collection of 30 stocks, is less volatile. And it has outperformed the S&P 500 each year over the same period. Why is that? As a group, HQ Portfolio stocks provided better returns with less risk versus the benchmark index; less of a roller-coaster ride, as evident in HQ Portfolio performance metrics.

Given the current uncertain macroeconomic environment around rate cuts and weak consumer sentiment, could UL face a similar situation as it did in 2021 and 2023 and underperform the S&P over the next 12 months — or will it see a strong jump? We estimate Unilever’s Valuation to be $62 per share, close to its current market price of $64. Our forecast is based on a 21x forward expected earnings of $2.90 per share in 2024. The 21x figure is slightly above the stock’s average P/E ratio of 19x, seen over the last five years.

Unilever reports its sales under three segments – Personal Care, Foods & Refreshments, and Home Care. These segments accounted for 44%, 35% and 21% of the company’s total sales in 2023. Our dashboard – Unilever Revenues: How Does Unilever Make Money – has more details on the company’s segments. Much of the sales growth lately is being driven by a good mix of better pricing and volume gains. Unilever sales stood at $33.6 billion in the first half of 2024. Its underlying revenue rose 4.1%, driven by a 2.6% rise in volume and 1.6% pricing gains. The company continues to expect at 3% to 5% underlying sales growth in the near term. Looking at a slightly longer term, Unilever’s sales grew 7% from $59.8 billion in 2021 to $63.9 billion in 2023. This growth has primarily been led by a better price realization.

Along with the company’s sales growth over the recent years, its adjusted net margin has increased from 9.7% in 2021 to 10.4% in 2023. Even for the first half of 2024, the company’s underlying segment profit margin rose 250 bps y-o-y. With the company’s focus on cost management, and an overall rise in volume, Unilever is poised for continued earnings growth. Furthermore, a decline in interest rates bodes well for consumer sentiment, and it will bolster Unilever’s performance.

Overall, Unilever is poised to deliver a low single-digit average annual top-line growth and a mid to high-single-digit earnings growth over the next three years. Investors have rewarded the stock with a higher valuation multiple, but is it worth picking now? We don’t think so. We believe that the positives around the improved profitability and pickup in volumes are already priced in. As such, investors willing to pick UL will likely be better off waiting for a dip.

While UL stock looks appropriately priced, it is helpful to see comparisons for companies across industries at Peer Comparisons.

| Returns | Sep 2024 MTD [1] |

2024 YTD [1] |

2017-24 Total [2] |

| UL Return | -1% | 36% | 106% |

| S&P 500 Return | -3% | 15% | 146% |

| Trefis Reinforced Value Portfolio | -1% | 12% | 736% |

[1] Returns as of 9/19/2024

[2] Cumulative total returns since the end of 2016

Invest with Trefis Market-Beating Portfolios

See all Trefis Price Estimates

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.