QUALCOMM Inc. on Track for Strong Q4 Earnings Amid 5G Expansion

QUALCOMM Inc. QCOM, a top player in semiconductors, concentrates on advancing 5G mobile network technology. The company is evolving from a traditional wireless communications business aimed at the mobile sector to a more connected processor firm serving the intelligent edge.

Split into three divisions — QCT (QUALCOMM CDMA Technologies), QTL (QUALCOMM Technology Licensing), and QSI (QUALCOMM Strategic Initiatives) — QUALCOMM will announce its fourth-quarter fiscal 2024 earnings on November 6, post-market closure. It currently holds a Zacks Rank #2 (Buy) and has an Earnings ESP of +0.48%.

Research indicates that companies with a Zacks Rank of #3 (Hold) or better, alongside a positive Earnings ESP, have a 70% chance of exceeding earnings expectations. Such stocks are typically expected to rise after earning calls. The Earnings ESP Filter can help investors discover top stocks to buy or sell ahead of earnings reports.

As 5G technology accelerates, QUALCOMM is leveraging investments to enhance its licensing program in mobile, indicating a crucial phase in its growth strategy.

Positive Earnings Predictions for QCOM

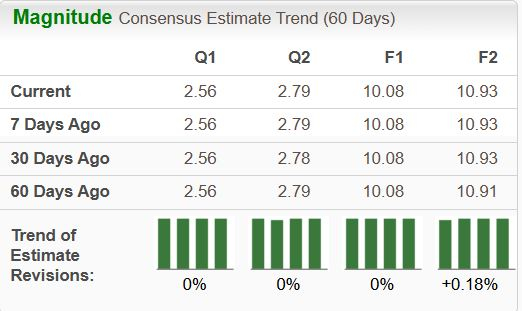

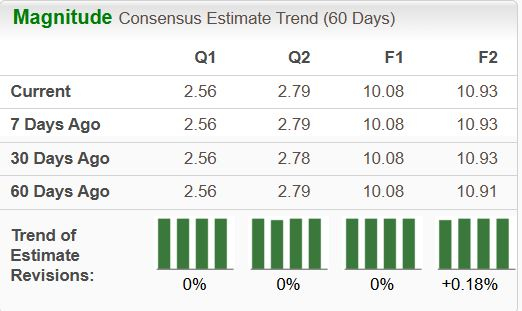

For its fourth-quarter fiscal 2024, analysts forecast QUALCOMM’s revenues to reach $9.90 billion, marking a 14.7% year-over-year increase. The Zacks Consensus Estimate for adjusted earnings per share (EPS) stands at $2.56, reflecting a 26.7% rise from the previous year. The company has consistently surprised Wall Street with positive earnings over the last four quarters, with an average beat of 7.6%.

Further proving its momentum, QCOM has seen positive revisions for fiscal 2025 estimates over the past two months. The outlook indicates an 8.2% increase in revenues and an 8.4% rise in EPS year over year.

Image Source: Zacks Investment Research

Key Factors for Q4 Performance

Analysts predict that QCT revenue from handsets will hit $6.15 billion, reflecting a 12.8% year-over-year growth. For QCT IoT, estimates stand at $1.47 billion, up by 6.4%. Expectations for QCT automotive revenue are robust, estimated at $791.51 million, a significant 48% year-over-year jump. The overall forecast for QCT revenue is set at $8.42 billion, projecting a 14.1% increase.

For QTL revenue, a consensus of $1.44 billion suggests a 14.3% increase compared to last year’s results. Moreover, revenues related to non-GAAP reconciling items are estimated at $44.71 million, marking a notable rise of 54.2%. The overall forecast for equipment and services revenues stands at $8.36 billion, with an expected growth rate of 14.7% year-over-year.

Analysts estimate that ‘Income before taxes- QTL’ will reach $1.04 billion, up from $829 million in the same quarter last year, while ‘Income before taxes- QCT’ is projected at $2.35 billion, compared to $1.89 billion the previous year.

Growth Catalysts for QCOM

Recently, QUALCOMM entered a multi-year partnership with Alphabet Inc. GOOGL to create generative artificial intelligence (AI) solutions within automotive digital cockpits. This initiative aims to drive digital transformation in the automobile industry. Additionally, QUALCOMM unveiled the Snapdragon Cockpit Elite platform to enhance in-car digital experiences and the Snapdragon Ride Elite platform for automated driving.

These advancements within the Snapdragon Digital Chassis Solution portfolio are gaining traction in the market. Leading automobile manufacturers like Mercedes-Benz AG and Li Auto have already integrated these solutions into their upcoming models.

The company is also capitalizing on the demand for enhanced connectivity through EDGE networking, which impacts various sectors including automotive, smart factories, and personal devices.

Growing trends in connected vehicles, including enhanced in-car experiences and vehicle electrification, are supported by QCOM’s robust automotive telematics and connectivity platforms.

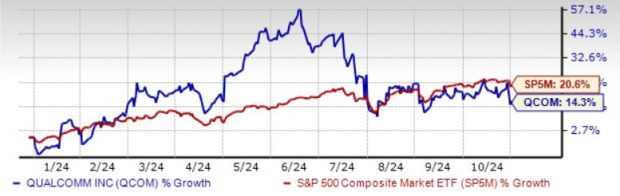

Valuation Insights for QCOM Stock

QUALCOMM is positioned in the top 40% of the Zacks Defined Computer and Technology – Wireless Equipment Industry. Given its favorable rank, the company is expected to outperform the market over the next 3 to 6 months. While QCOM stock has lagged the S&P 500 year to date, it currently presents an attractive valuation.

Image Source: Zacks Investment Research

Trading at a forward price/earnings (P/E) ratio of 15.12X, QCOM is below the industry average of 15.99X and the S&P 500’s P/E of 19.15X. It boasts a return on equity (ROE) of 38.12%, significantly higher than the S&P 500’s 16.78% and the industry’s average of 8.32%.

Potential Short-Term Gains for QCOM Shares

Brokerage firms estimate an average short-term price target for QCOM that suggests a potential increase of 30.6% from its last closing price of $165.27. With target prices ranging from $160 to $270, this indicates a possible maximum upside of 63.4% and minimal downside risk of 3.2%.

Image Source: Zacks Investment Research

Research Team Selects “Top Pick for Significant Growth”

Among thousands of stocks, five Zacks experts have identified their favorites expected to grow by 100% or more soon. Of these, Director of Research Sheraz Mian has handpicked one with the greatest potential for explosive growth.

This chosen company targets millennial and Gen Z audiences, having nearly $1 billion in revenue last quarter. A recent market dip presents an optimal opportunity for investment. Although not every elite pick may succeed, this one shows promise similar to past Zacks recommendations, like Nano-X Imaging, which rose +129.6% in just over nine months.

Want to view our latest stock recommendations? Today, you can download the report 5 Stocks Set to Double for free.

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

To read this article on Zacks.com, click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.