Micron Technology, Inc. (MU) has surged by 504.3% over the past year, emerging as a significant player in the artificial intelligence (AI) sector. In comparison, NVIDIA Corporation (NVDA) and Palantir Technologies Inc. (PLTR) saw gains of 79% and 25.6%, respectively, during the same period. Both companies reported strong revenue growth in their latest quarterly results, with NVIDIA recording $62.3 billion in data center revenues and Palantir achieving $1.4 billion in total revenues in their respective fourth quarters.

Micron’s fiscal second quarter revenues reached $23.86 billion, fueled by high demand for its AI-focused memory solutions, particularly high-bandwidth memory (HBM) chips. The company anticipates a revenue increase to $33.5 billion in the fiscal third quarter of 2026, underscoring its robust demand in the face of supply limitations. In terms of profitability, Micron is expecting a gross margin of 81%.

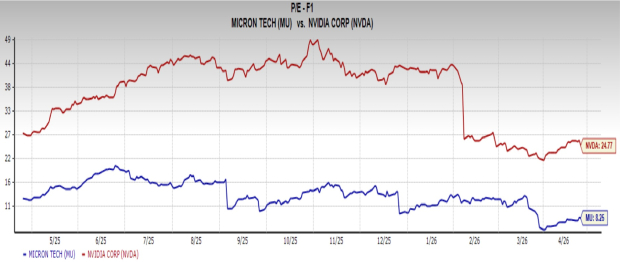

Looking ahead, Micron’s diversified focus on memory and storage solutions positions it favorably compared to NVIDIA and Palantir, which could be susceptible to concentrated risks. Moreover, Micron’s lower forward price-to-earnings (P/E) ratio of 8.25 offers an appealing investment angle against NVIDIA’s ratio of 24.77.