The Tale of Path’s Remarkable Growth

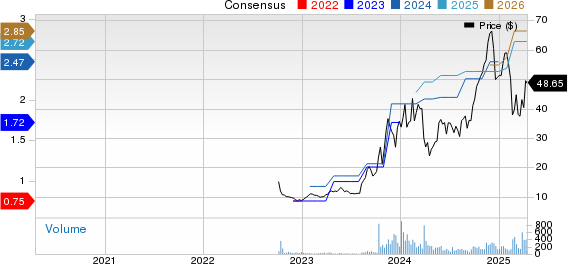

Path, taking a different road from its competitors, has defied the market norms over the last two tumultuous years. The market, akin to a roller coaster, witnessed both consistent dips and sharp ascensions, but none have triumphed quite like UiPath. Despite the cloud ETFs experiencing contrasting fates, Path has soared, leaving its peers in the dust. However, it’s crucial to note that while Path’s shares have witnessed a commendable surge, they still lag far behind their levels of two years ago.

“Have Path shares run too fast and too far?” This is the question that lingers in the minds of many. The recent rally seems to be predicated on the hope of diminishing inflation and lower interest rates. However, the future remains uncertain, and predictions about the course of the market are rife with contradictions. Market observers are split between conflicting forecasts, with no prevailing consensus in sight. The immediate future for high-growth IT shares, including UiPath (NYSE:PATH), seems enshrouded in mystery. It’s expected that these shares, including Path, will soon encounter a period of consolidation due to the prevailing uncertainties.

In line with expectations, Path shares have finally embarked on the anticipated phase of consolidation. With the New Year came a swift decline in Path shares, providing investors with a potential entry point. Despite this, attempting to forecast the macro influences that will significantly impact PATH’s share price in the coming weeks would be an exercise in futility.

However, this article doesn’t dwell on short-term market maneuvers. Instead, it focuses on the operational performance and valuation of Path over the next 12 months. Counting on a crystal ball is futile, so the valuation of UiPath shares will undoubtedly hinge on the evolving high-growth IT market in 2024. The stage for appreciable growth in Path shares can only be set against a backdrop of a congenial market environment for high-growth IT shares. Guided by these dynamics, UiPath is poised to surpass current consensus forecasts, as outlined in this article.

Last quarter, Path’s revenue growth and year-on-year growth of the ARR balance reached an impressive 24%, with net new ARR growing by 15% sequentially. Notably, the company’s free cash flow margin stood at about 13%. It also raised its expected year-end ARR and increased its forecast for non-GAAP operating income. Surprisingly, the 1st Call consensus for 2024 revenue growth fell below 20%, suggesting a potential slowdown in growth. However, the company’s backlog (RPO balance) revealed a contrasting indicator regarding Path’s actual growth momentum.

Path’s performance didn’t solely hinge on revenue. The sequential growth in ARR additions, albeit a second-order figure, indicated a shift in market efficiency. The company’s go-to-market focus on acquiring larger customers with a higher propensity to grow yielded fruit, manifesting in a constant currency, dollar-based net expansion rate of 123% in the quarter.

Ashim Gupta

Yes, I would just say, Mark, we’re really pleased with our performance and the team’s execution. We are focused on closing out a good year-end here. And the teams are really focused on that. And we look at our fourth-quarter guidance just putting the right prudence and the right macroeconomic variability included in our guidance, and we’ll update as we get closer to next year.

In this very uncertain environment, the company has taken an appropriately conservative path

The Future of Automation: Path’s Growth Acceleration and Positive Sales Outlook

In the realm of enterprise IT spend, the recent upturn in macro environment, as indicated by various surveys, may bring with it a welcome surge in current guidance and expectations. However, despite the positive momentum, some analysts on SA appear to have downgraded their ratings without fully acknowledging the broader implications. It’s crucial not to be too literal when using the guided numbers as the most likely forecast.

Looking at the recent forecasts, the company is now anticipating Q4 revenues of $383 million, compared to the previous projection of $380 million. The predicted ending ARR stands at $1.455 billion, up from the previous forecast of $1.435 billion. For a company of this caliber, ARR and ARR growth are pivotal metrics in assessing sales growth. Additionally, the company has increased its Q4 non-GAAP operating income forecast to $78 million, from the earlier projection of $63 million.

In a heartening development, third-party surveys on IT spending growth have shown a recent uptick. While surveys may not always be entirely reliable, there seems to be a consensus that the sluggish revenue growth witnessed in the space last year was an anomaly in the overall trajectory of IT spending growth. This sentiment appears to hold water, especially given the indication of an acceleration in growth within the process automation space, where Path enjoys a leading market position.

In the case of Path, its ability to develop products that users view as integral to an AI strategy has been a significant factor in its success. While delving into the product strategy in detail is beyond the scope of this discussion, the concept of automation using bots and AI resonates strongly with large enterprises.

The Dynamics of PATH’s Growth Acceleration

UiPath, the frontrunner in the Robotic Process Automation (RPA) domain, offers technology that simplifies the building, deployment, and management of software robots, commonly referred to as bots. These bots can be trained to mimic human actions, such as interpreting screen content, executing specific keystrokes, and performing a wide array of predetermined tasks—essentially handling repetitive tasks, and doing so with far greater speed and precision than human counterparts. (Refer to PATH’s marketing white paper for a detailed insight into RPA).

It is common knowledge that users are keen to heavily invest in generative AI solutions, a trend that is poised to lift numerous boats, but perhaps not all. When the AI frenzy took the market by storm last spring, a prevailing concern for PATH, or more specifically, its shares, was whether the advancements in generative AI would diminish the demand for the process automation bots central to the company’s offerings. The underlying belief is linked here.

Contrary to the provocative narrative, in the context of PATH’s operational performance, this notion couldn’t be farther from the truth. In reality, AI and process automation bots complement each other seamlessly. This very insight was at the core of my previous article on PATH shares last spring.

A few months ago, PATH introduced a game-changing sales tool, NorthStar, which has evidently made a significant impact on the company’s sales efficiency. While an in-depth analysis of NorthStar is beyond the scope of this discussion, it is crucial to note that the tool equips PATH sales personnel with a roadmap demonstrating the ROI at various stages of the automation journey for users. The iterative use of NorthStar is proving to have a more significant impact on driving the increase in ARR than may be immediately apparent. Furthermore, the company’s relatively new partnerships with SAP and Deloitte are beginning to yield substantial transactions.

Daniel Dines

(For those unfamiliar with the term, and that most surely includes this writer until I looked it up, an autonomous agent is a system situated within and part of an environment that senses that environment and acts on it, over time in pursuit of its own objectives. According to the link above, the deployment of autonomous agents is supposed to be the next AI wave after Chat GPT. There is some uneasiness about this trend, which I confess I share, but which is not a factor in evaluating PATH shares—the only subject at hand).

I believe the quote from the founder/co-CEO encapsulates the crux of the ongoing developments. A combination of generative AI and automation undeniably yields superior results for users, and the success of PATH’s sales tool NorthStar effectively demonstrates this. This is a key reason for the robust growth in sales, as evidenced by the substantial increase in net new ARR, which I anticipate will be a long-standing trend, driving a sustained acceleration in revenue growth.

Another notable impediment to sales growth in the past has been the protracted deployment time for the average bot. While it is designed to take only a few weeks to create an intelligent bot, deploying it across a business vertical typically takes 6-12 months, an untenable duration. The challenge has been to establish a viable knowledge base that enables a new chatbot to deliver satisfactory performance.

Now, the company has unveiled a product called UiPath AutoPilot, a characteristic nomenclature for most generative AI products. This pilot, currently in beta, is reportedly demonstrating tangible and positive results in terms of streamlining the bot deployment cycle.

Already in use at some of PATH’s clients are models for Document Understanding and Communication Mining, a concept elucidated by the co-CEO.

Daniel Dines

The Rise and Dominance of UiPath in the RPA Market

UiPath, the leader in the Robotic Process Automation (RPA) space, has emerged as a dominant player in the industry, commanding a massive market share of approximately 36%. The company has been making waves in the RPA market, showcasing significant improvement over the past several quarters.

UiPath’s Break-through Growth Quarter

UiPath recently reported a break-through growth quarter driven by multiple pillars supporting significant growth above the current 1st Call consensus revenue growth forecast of less than 20% for the year. The foundation of this success lies in the enhanced results users are experiencing in their automation journeys through the use of bots and generative AI as part of a unified strategy.

The company’s solutions are designed to aid developers in building next-generation models that comprehend processes, tasks, screens, and documents as part of an enterprise AI strategy. Moreover, UiPath has NorthStar, an effective sales tool, assisting its sales force in developing a roadmap and anticipated ROI, along with tools to expedite the deployment of intelligent bots.

While offering insights into the company’s future growth, it is important to consider historical context. UiPath has consistently outperformed expectations by leveraging its innovative technologies, driving robust growth prospects for the company.

UiPath’s Market Dominance

UiPath’s dominance is underscored by its market share, as validated by a recent study by Gartner, showcasing its strong performance, global brand recognition, and a vast customer and partner ecosystem of more than 2.5 million members.

The company’s prominence in the RPA space has been reiterated by industry thought leaders, including Wayne Butterfield, the Global Lead for Augmented Intelligence at ISG. Butterfield emphasized the suite of complementary capabilities that sets UiPath apart, widening the scope for automation and solidifying its market leadership.

Moreover, UiPath has demonstrated a strategic approach by delving into adjacent fields such as Optical Character Recognition (OCR) and Process Mining, consequently opening up a myriad of new opportunities for customers. It should be noted that UiPath’s consistent leadership in the RPA space has been a precursor to market share expansion and substantial growth prospects.

UiPath’s Business Model

UiPath’s business model has witnessed significant improvement over the past several quarters, attributed to better expense management and leverage at scale. The company has also achieved a slight rise in non-GAAP gross margins, demonstrating its ability to adapt and evolve in the competitive RPA market.

By closely examining UiPath’s performance, it is evident that the company’s strategic approach towards innovation and market expansion has positioned it for sustained growth and continued dominance in the RPA industry. The data indicates that UiPath is more likely to sustain its market leadership in the foreseeable future, presenting lucrative prospects for investors.

The Resilience of UiPath: A Guide to Investment Potential

Meeting Revenue Growth Targets

UiPath, a leading robotic process automation firm, is charting an impressive trajectory to achieve a revenue growth of 30% or more next year in a challenging software sales environment. This comes on the heels of a reduction in non-GAAP sales and marketing expenses to 45% of revenue, down from 53% in the prior year. The notable decline in sales and marketing expense over the first 6 months of the fiscal year reflects the company’s commitment to cost efficiency, even as it accelerates sales hiring to bolster its capacity.

Investment in Research and Development

The company’s research and development expenditure last quarter accounted for a modest 16% of revenue, indicating a consistent commitment to innovation. Sequentially, there was no substantial change in non-GAAP research and development spend, despite a 13.5% increase in revenues. This investment underscores the company’s dedication to technological advancement and product improvement.

Effective Cost Management

Notably, the non-GAAP general and administrative expense ratio was significantly reduced last quarter due to classification adjustments. This led to a 15% decrease in reported non-GAAP general and administrative expense compared to the previous year. The company’s focus on spending discipline has yielded commendable results, with reported general and administrative expenses down by about 16% over the first 9 months of the year.

Operating Margin and Cash Generation

The third quarter saw a substantial improvement in non-GAAP operating margins, reaching 13% of revenue, compared to 7% in the prior year. The company is targeting a further increase to 20% in the current quarter. Despite some skepticism, the company’s history of significant seasonality and its disciplined spending approach provide a strong foundation for achieving this goal. Additionally, UiPath’s resilience is evident in its cash generation, with a 17% free cashflow margin through the first 9 months, compared to burning cash in the prior year.

Evaluating Share Performance and Growth Opportunities

Despite a substantial rise in UiPath shares since their lows in late October 2023, the company’s position is still down over 40% in the last two years, presenting an opportunity for valuation growth. The company’s leadership in robotic process automation and the accelerating growth in this sector, combined with generative AI solutions, highlight the potential for sustained market leadership. Furthermore, third-party analysis indicates a favorable evaluation of UiPath’s competitive position, suggesting additional market share gains.

Assessing Valuation and Future Outlook

Despite the significant run in share price, UiPath remains undervalued relative to its growth prospects. The company’s expansion plans align with a forecasted CAGR in the mid-20% range, indicating substantial investment potential. The current valuation metrics do not fully reflect the company’s likely margin improvement, and the company’s potential for positive alpha presents a compelling case for long-term investment.