Meta Platforms (META) boasted phenomenal performance throughout the previous year, culminating in its decision to issue its inaugural dividend. Nevertheless, the exorbitant premiums on put options present a lucrative opportunity for shareholders to generate additional income by shorting out-of-the-money (OTM) puts.

Delving into Meta’s robust free cash flow (FCF) recently in a Feb. 9 Barchart article titled, “META Stock Could Still Be Worth Up Over 18% to $556 Per Share, Based on Its Massive FCF,” I posited that the company’s steadfast FCF in the past 4 quarters could imply Meta’s stock has a value of $556 per share.

Currently, trading around $487.23 per share as of midday on Friday, Feb. 23, META’s price forecasts a potential upside of at least 14% in the immediate future.

More notably, the elevated put option premiums pave the way for existing shareholders to capitalize on the situation by selling short OTM puts expiring soon.

Making Profits by Shorting OTM Puts

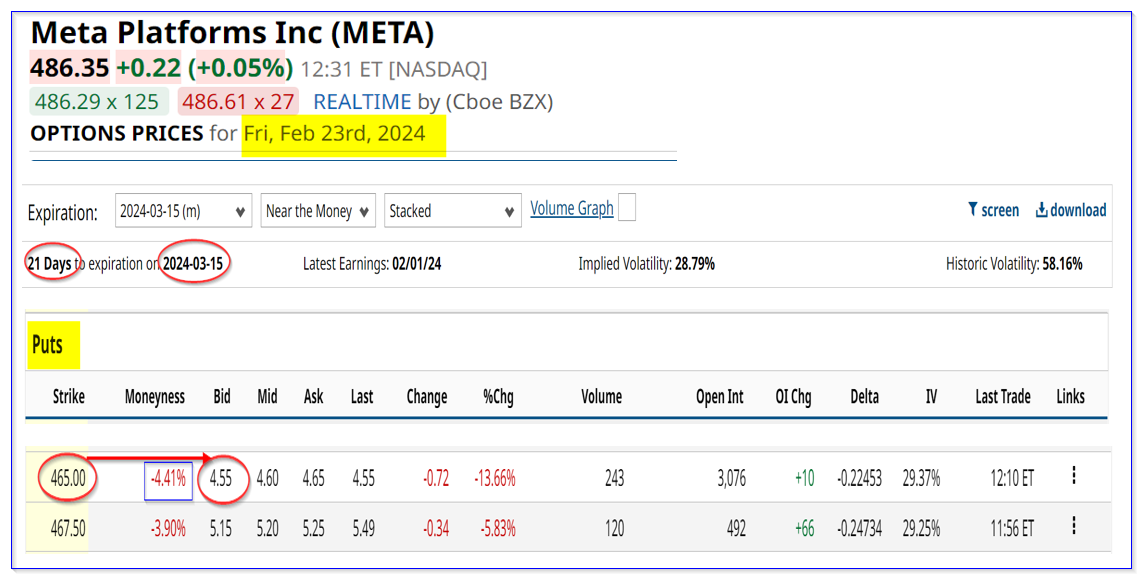

For instance, examine the March 15 expiration period, looming three weeks away. A prime example would be selling short the $465 strike price put, positioned over 4% lower than today’s price, with a bid side premium of $5.00 per contract.

This translates to an instant yield of roughly 1.0% for the short seller. Although buying the stock at $465.00 is a contingency if Meta plunges to that level, the short seller secures an immediate payment of $4.55 per contract for that commitment.

To navigate this approach, the investor must first raise $46,500 in cash and/or margin through their brokerage firm since each contract comprises 100 shares of META stock, amounting to 100 x $465.00, which equals $46,500.

Thereafter, securing authorization from the brokerage firm to vend short cash-secured puts, the investor can proceed by initiating an order to “Sell to Open” 1 put contract at $465 for expiration on March 15.

The account swiftly receives $455.00. Hence, regardless of the outcome, the investor retains this premium. Should Meta’s stock price remain constant by March 15 without dipping to $465 from $487.23, the short put contract expires inconsequential.

This implies an anticipated annualized return (ER), given this pattern recurs every 3 weeks, of 16.63%, since there are 17 intervals of 3 weeks in a year, culminating in 17 x 0.9875% equaling 16.63%.

In essence, the dollar ER per episode amounts to $7.735 (17 x $455) against an investment each period of $46,500.

Strategizing against Downside Potential

However, anticipating, each 3-week out put option play might not yield 1.0% consistently for the investor represents one risk.

An alternate risk surfaces in the event of Meta’s value plummeting below $465.00, triggering the automatic utilization of the investor’s secured cash to procure META at $465.00 (if the investor fails to address the option play or exit from it).

Consequently, an unrealized loss could materialize. Nonetheless, current shareholders can potentially offset this through averaging it with their existing holdings.

Multiple methods exist to mitigate this downside prospect. Initially, the investor could consider acquiring put options at a deeper OTM strike price for the same expiration period to temper the risk. For instance, purchasing the $460 strike price put at $3.65, utilizing the $4.55 premium received, allows the investor to confine the downside risk to just $5.00.

It is vital to note that the investor already commands a net credit of 90 cents ($4.55 received minus $3.65 paid). Hence, the net risk merely amounts to $4.10 ($5.00 – $0.90). Furthermore, closing the short-put trade before its expiration can restrict the obligation to procure the shares.

Another risk-abating approach entails vending out-of-the-money covered calls once the short puts come into play. This avenue empowers the investor to recoup additional income with the newly purchased shares in the event they were mandated to buy the shares post-expiration.

Given Meta’s substantial growth potential, acquiring META stock at $465.00 and retaining the shares long-term could prove beneficial for existing investors.

More Stock Market News from Barchart

On the publication date, Mark R. Hake, CFA held no positions (directly or indirectly) in any of the mentioned securities. The information and data in this article serve purely informational purposes. Refer to the Barchart Disclosure Policy for further details.

The opinions and viewpoints expressed in this piece solely belong to the author and do not necessarily mirror those of Nasdaq, Inc.