EverQuote, Inc.’s EVER has tightened its belt, fine-tuned its algorithms, and with the promise of a roaring revival in the auto insurance realm, it’s a seat many might want to hold onto in the rollercoaster world of stock investing.

Earnings on the Horizon

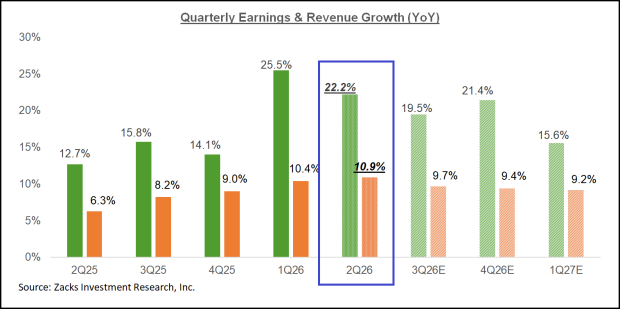

Step right up and behold! The Zacks Consensus Estimate hints at a 68.1% surge in EverQuote’s 2024 earnings per share from the year prior, accompanied by a melodious 11.2% uplift in revenue expectations.

And the show goes on! The 2025 forecast promises a harmonious 56.8% leap in EPS juxtaposed against a crescendo of 22.1% in revenue projection.

Earnings Highs and Lows

Much like a magician pulling a rabbit out of a hat, EverQuote has consistently surprised with its earnings, outshining expectations in the last four quarters with an average beat of 36.78%.

Market Pulse & Performance

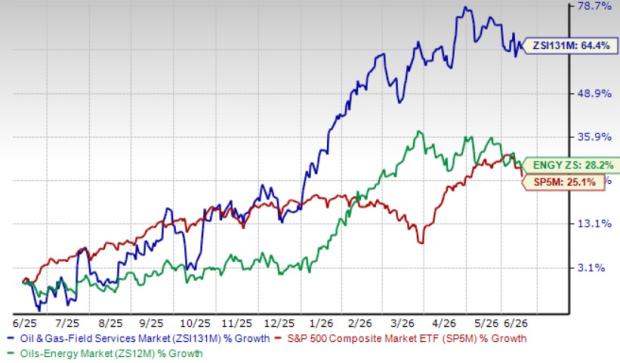

With a Zacks Rank #3 (Hold) badge, EVER has been the Cinderella of the stock market ball, rising 41.7% in the past year, outshining industry rivals by leaps and bounds.

Image Source: Zacks Investment Research

Engines of Growth

EverQuote is a trailblazer striding into new territories with gusto. Witnessing an upsurge in consumer interest, the company stands ready to capture a larger slice of the insurance market pie. Tinkering with its marketing strategies, EverQuote is set to feast on increased consumer traffic and a potential bonanza of policyholders.

As the coins keep rolling in, EverQuote’s coffers are swelling, with no debt to weigh it down. The company is positioned to meet future financial obligations through savvy cash management, setting a sturdy cornerstone for its financial fortress. A recent makeover in its loan agreements and extended lines of credit indicate a commitment to financial health in the long run.

Trimming the excess fat, EverQuote dropped its health insurance division to sharpen its focus on home and renters’ insurance, resulting in a significant revenue surge. This trimmed physique allows EverQuote to dance gracefully, generating strong top-line performance from a less tumultuous segment.

With insurance premiums scaling up and claims costs stabilizing, EverQuote’s future looks rosy alongside the broader auto insurance industry, promising a bouquet of growth opportunities.

Other Contenders

In a market teeming with potential, other notable contenders include Horace Mann Educators Corporation (HMN), CNO Financial Group, Inc. (CNO), and Assurant, Inc. (AIZ). With Horace Mann and CNO Financial shining brightly at Zacks Rank #1 (Strong Buy), and Assurant gleaming with a Zacks Rank #2 (Buy), the competition is fierce but promising. The future looks bright for those wise enough to hitch their wagons to these stars.

Is EverQuote destined for greatness among the constellation of insurance stocks? Only time will tell as investors buckle in for the thrilling ride. As the financial data unfolds, the choice to hold, sell, or buy EverQuote stock remains a calculated gamble, akin to navigating a maze of mirrors in a carnival funhouse where each reflection holds a different outcome. Stay vigilant, dear investor, for the stock market, like the unpredictable twists and turns of a rollercoaster, promises thrills, chills, and unforeseen surprises at every bend.

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.