Thermo Fisher Scientific Inc. TMO signals a staunch fortitude for investors, poised to surge in forthcoming quarters on the stalwart foundation of its diversified businesses and calculated acquisitions. The company’s unwavering solvency stands as a beacon of hope amidst uncertainty. Nonetheless, a dip in COVID-19 testing demand and prevailing economic challenges cast lingering shadows over the stock’s trajectory.

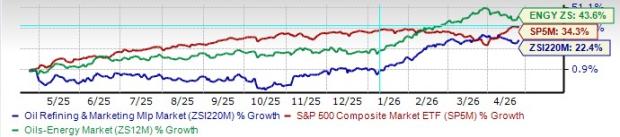

Over the past year, this Zacks Rank #3 (Hold) stock has demonstrated a commendable 4.4% uptick, juxtaposed against the industry’s 9.5% climb and the S&P 500 composite’s 29.5% surge.

A behemoth in the medical and laboratory equipment domain, Thermo Fisher boasts a market capitalization of $216.90 billion. TMO flaunts an earnings yield of 3.78%, leaving the industry’s -6.34% in its wake. In the latest reported quarter, the company managed to exceed earnings expectations by 0.53%.

Let’s peel back the layers.

Upsides: Forging Ahead

Strength in End Markets: Amidst the pharma and biotech end market, Thermo Fisher has amplified its biosciences and bioproduction businesses, robustly catering to global vaccine production requisites. Its pharma services arm diligently supports pharma and biotech clientele in the development and manufacturing of vaccines and therapies worldwide.

The latest update reflects robust growth in academic and government businesses during the fourth quarter of 2023. The company witnessed notable expansion across various sectors throughout the year, encompassing electron microscopy, chromatography, and mass spectrometry, besides the research and safety market channel. Thermo Fisher’s industrial and applied segment glided ahead on a steady course as well.

Image Source: Zacks Investment Research

Strategic Acquisitions to Boost Growth: Thermo Fisher’s growth blueprint revolves around strategic acquisitions aimed at bolstering its technological and business landscapes. The recent announcement unveiling the acquisition of Olink Holdings signifies a strategic move to fortify Thermo Fisher’s footing in the burgeoning proteomics arena.

Moreover, the integration of CorEvitas ramped up Thermo Fisher’s clinical research competencies with a premier regulatory-grade registry platform. The addition of MarqMetrix seamlessly supplements the company with Raman-based in-line PAT capabilities. Furthermore, TMO infused its portfolio with The Binding Site’s acquisition, broadening its specialty diagnostics realm with groundbreaking innovations in diagnosing and monitoring multiple myeloma.

Stable Solvency: As of 2023, Thermo Fisher ended the year with a debt-free balance sheet—a promising portent. The company boasted $8.08 billion in cash and cash equivalents, though a slight decline from $8.52 billion in 2022.

The times interest earned metric for Thermo Fisher stands at 5.6%, witnessing a sequential dip from 6.1% in the third quarter of 2023.

Downsides: Navigating Challenges

Lower COVID-19 Sales Hurt Growth: The surge in biosciences and bioproduction capabilities during the COVID-19 era, catering to global vaccine demands, has encountered a decline recently. Thermo Fisher has witnessed a consistent slump in COVID-19 testing-oriented demand, leading to weakened sales across major regions.

Macroeconomic Challenges Continue to Weigh on TMO: A tumultuous macroeconomic landscape and sluggish economic rebound in China pose obstacles to Thermo Fisher’s growth trajectory. The company faces headwinds in government and academic sectors. Additionally, the challenges in North America and Europe have dent European academic budgets, precipitating declines in those regions.

Estimate Trend: Looking Ahead

The Zacks Consensus Estimate pegs the company’s 2024 earnings per share at $21.53, reflecting a marginal uptick from $21.52 over the past month.

Revenue projections for TMO in 2024 hover around $42.74 billion, signaling a slight 0.3% drop from the preceding year.

Key Picks: Handpicked Selections

Among esteemed contenders in the expansive medical landscape are Cardinal Health (CAH), Stryker (SYK), and DaVita (DVA).

Cardinal Health boasts a long-term estimated earnings growth rate of 14.2%, outshining the industry’s 11.6%. CAH has consistently outperformed in earnings, surging 50.9% over the past year, dwarfing the industry’s 14.2% ascent.

With a Zacks Rank #2 (Buy) badge, Stryker reports an earnings yield of 3.36%, trouncing the industry’s meager 0.02%. SYK’s shares have spiraled up by 28.5% vis-a-vis the industry’s 5.2% increment in the last year.

DaVita, donning a Zacks Rank #1 title, anticipates a long-term earnings growth rate of 12.1%, eclipsing the industry’s 11.9%. DVA shares have witnessed a remarkable 74.4% hike, juxtaposed against the industry’s 22% rise over the past year.

Zacks Reveals ChatGPT “Sleeper” Stock

One little-known company is at the heart of an especially brilliant Artificial Intelligence sector. By 2030, the AI industry is predicted to have an internet and iPhone-scale economic impact of $15.7 Trillion.

As a service to readers, Zacks is providing a bonus report that names and explains this explosive growth stock and 4 other “must buys.” Plus more.

Download Free ChatGPT Stock Report Right Now >>

Stryker Corporation (SYK) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Thermo Fisher Scientific Inc. (TMO) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.