Assurant, Inc. has witnessed a momentous 57.6% surge in the market over the past year, eclipsing industry growth at 27.3%. This performance significantly outpaces the Finance sector’s rise of 26.1% and the Zacks S&P 500 index’s uptick of 27.7% within the same timeframe.

Bolstered by a market capitalization of $9.73 billion, the average volume of shares traded in the last three months stood at 0.3 million.

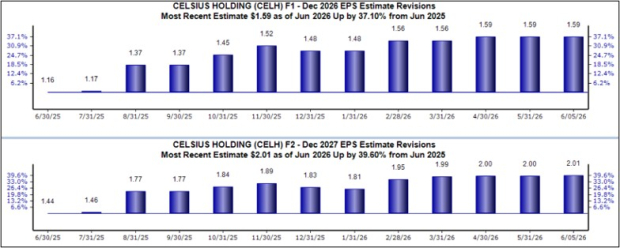

Image Source: Zacks Investment Research

Fueling this meteoric rise were the flourishing Global Lifestyle arm, growth in fee-based capital-light businesses, robust capital management, and effective capital deployment.

This Zacks Rank #2 (Buy) insurer boasts an impressive four-quarter average earnings surprise of 42.15%.

The recent 5.9% surge in the Zacks Consensus Estimate for Assurant’s 2024 earnings, followed by a 6.4% increase projected for 2025, portrays a bright outlook in the eyes of analysts.

Are We in for a Long Bull Market?

Forecasts paint a promising picture for Assurant, with the Zacks Consensus Estimate hinting at a 3.4% year-over-year earnings growth projection for 2024, alongside a 4.1% upsurge in revenues compared to 2023.

The 2025 estimates look even rosier, with a projected 7.7% earnings growth and a 3.4% revenue boost year-on-year from the 2024 consensus marks.

Amidst this favorable landscape, a strategic focus on expanding fee-based capital-light businesses – currently accounting for 52% of segmental revenues – is expected to drive growth for Assurant, with management eyeing double-digit growth from this sector over the long haul.

The insurer is set to make strides in Homeowners coverage due to burgeoning lender-placed net earned premiums, while growth in Connected Living and Global Automotive is poised to fuel Global Lifestyle.

Shifting gears to innovation, Assurant is set to elevate the Connected Living platform through new products, services, and partnerships, potentially doubling margins to 8% over the long term.

Furthermore, a rising trend in investment income, coupled with consistent net investment growth, is indicative of a healthy financial strategy.

With a rock-solid capital management policy, Assurant’s 19-year dividend increase streak stands as testament to its financial stability. Share repurchases totaling $10 million have already been initiated in 2024, with $664 million still allocated for further buybacks. A free cash flow conversion exceeding 100% in recent quarters underscores the company’s robust earnings.

The company’s Return on Equity (ROE) – up by 490 basis points year-over-year to 18.4% – outperforms the industry average of 13.2%. Trading at a discount relative to the industry average, Assurant’s price-to-book value of 2.05X sits below the industry standard of 2.43X, making it an opportune time to consider an investment before valuations expand.

Notably, Assurant boasts an exemplary Value Score of A, historically synonymous with stellar returns. Conjoining a Value Score of A or B with a Zacks Rank #1 or 2 has showcased superior returns in back-tested results.

Exploring Other Investment Options

Other standout stocks in the multi-line insurance realm include Enact Holdings (ACT), CNO Financial Group (CNO), and Horace Mann Educators Corporation (HMN), each currently holding a Zacks Rank #1. Noteworthy performance metrics underscore the potential for growth within this sector.

Enact Holdings, with a notable four-quarter average earnings surprise of 24.59%, has witnessed a remarkable 33.9% surge in its stock value over the past year.

CNO Financial Group’s anticipated earnings growth of 2.5% and 7.1% for 2024 and 2025 respectively, echoes the overall growth trajectory witnessed by the company, with stocks up by 20.8% over the same period.

Horace Mann Educators Corporation has also shown stellar performance, with a 104.5% and 19% projected year-over-year growth for 2024 and 2025 earnings, reflecting a steady upward trend in the stock price.

Such positive indicators across the multi-line insurance landscape hint at favorable conditions for investors in the present market climate.

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.