NiSource Inc.’s NI ambitious infrastructure modernization endeavors are set to fortify its operational reliability, positioning the company as a beacon of stability in the utility sector. By integrating eco-friendly assets into its portfolio, NiSource is not just boosting its overall performance but also championing sustainability in a world hungry for energy innovation.

Now, let’s delve into the compelling reasons why this Zacks Rank #2 (Buy) enterprise shines brightly in the investment landscape.

Unveiling Growth Trajectory & Track Record

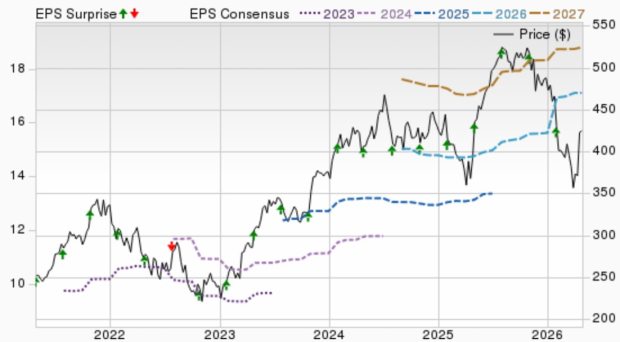

In the last 90 days, the Zacks Consensus Estimate for NiSource’s 2024 earnings per share (EPS) remains steady at $1.71.

Predictions for the 2024 sales estimate stand firm at $6.14 billion, indicating a bullish 11.5% year-over-year surge.

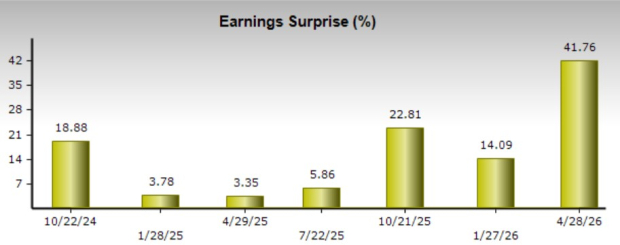

NiSource flaunts a stable long-term (three to five years) earnings growth rate of 6%, supplementing this with an impressive average earnings surprise of 5.6% over the last four quarters.

Ascension in Equity Returns

Currently boasting a robust Return on Equity (ROE) at 10.11%, NiSource outperforms the industry’s average of 8.66%, proving that it maximizes its funds better than peers in the utility electric power sector.

Debt Discipline & Resilience

NiSource exhibits a total debt to capital ratio of 58.23%, surpassing the industry’s standard of 61.5%, showcasing a prudent financial stance.

With a healthy time-to-interest earned ratio of 2.7 in the fourth quarter of 2023, the company displays a reassuring ability to meet future interest obligations without breaking a sweat.

The Legacy of Dividend Consistency

NiSource’s unwavering commitment to shareholders is evident in its sustained dividend payments. The current quarterly dividend of 26.5 cents per share amounts to an annualized $1.06, marking a 6% rise from the previous level. The company aims for an annual dividend payout ratio of 60-70%, with a current dividend yield of 3.88% trumping the Zacks S&P 500 Composite’s 1.29%.

Strategic Capital Infusion

NiSource’s meticulous focus on modernizing its utility infrastructure is a testament to its forward-thinking approach. With projected investments ranging between $3.3-$3.5 billion for 2024 and $15.2-$16.6 billion during 2024-2028, NiSource anticipates an annual rate base growth of 8-10% until 2028, underpinned by robust capital expenditures.

Performing Ahead of the Pack

Over the past six months, NiSource’s stock has surged by 14.1%, outperforming the industry’s 10.1% growth trajectory.

Further Investment Insights

In the same industry arena, other formidable contenders include Pinnacle West Capital Corporation (PNW), Unitil Corporation (UTL), and TransAlta Corporation (TAC), all currently carrying a Zacks Rank #2. These companies embody resilience and promise in the dynamic utility sector.

PNW and UTL showcase extended earnings growth rates of 7.55% and 7.08%, respectively, with TAC experiencing significant positive EPS estimations for 2024. Each entity brings a unique value proposition to the investor’s table.

Conclusion: A Power Surge Awaits

As the energy landscape evolves, NiSource stands as a stalwart, orchestrating a symphony of innovation, stability, and growth to entice investors looking for a reliable asset in a phantasmagoria of market offerings.

Source Guide

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.