Charter Communications Prepares for Q3 Earnings Release Amidst Market Challenges

Insights on Financial Projections and Stock Performance Ahead of Earnings

Charter Communications, Inc. (CHTR), a major telecommunications player based in Stamford, Connecticut, is set to announce its fiscal Q3 earnings results on Friday, Nov. 1, before market trading begins. The company holds a market capitalization of almost $47 billion and provides services ranging from broadband and cable TV to voice services, catering to both residential and commercial customers.

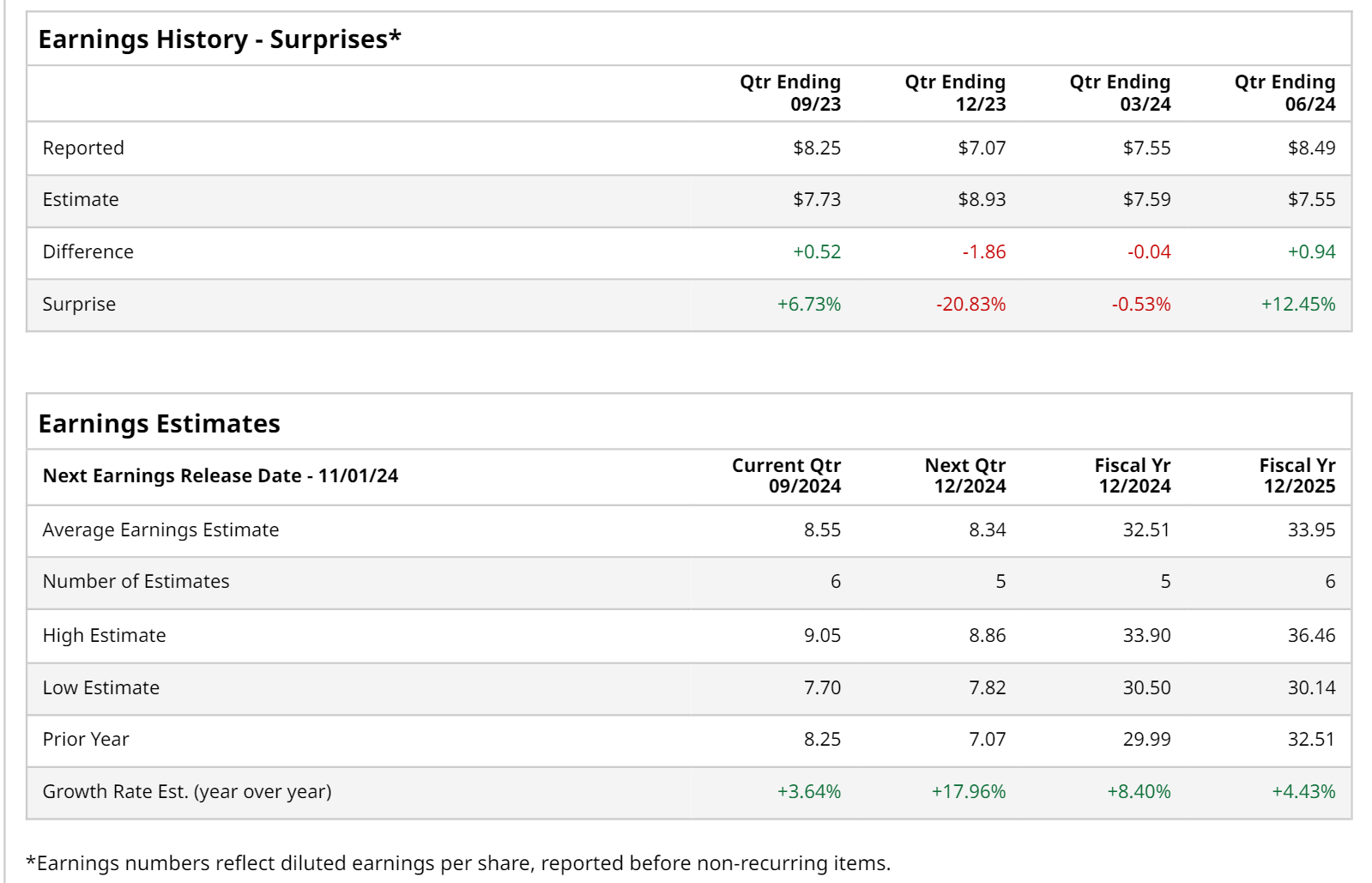

Analysts anticipate that Charter will report earnings of $8.55 per share, reflecting an increase of 3.6% from last year’s $8.25. The company has a mixed earnings history recently, having met or exceeded Wall Street estimates in two of the last four quarters—most recently in Q2, where it reported an EPS of $8.49, beating forecasts by 12.5%.

Looking ahead to fiscal 2024, analysts estimate an EPS of $32.51, which would represent a notable 8.4% growth from the $29.99 reported in fiscal 2023. Moreover, projections indicate a further rise to $33.95 in fiscal 2025, reflecting a 4.4% year-over-year increase.

Year-to-date, Charter’s shares have experienced a decline of 16.1%, in stark contrast to the S&P 500 Index ($SPX), which has risen 21.9%, and the Communication Services Select Sector SPDR ETF (XLC), with a return of 24.5% during the same period.

Several factors have led to Charter’s stock underperformance, notably a decline in internet and video subscribers due to intensifying competition. Nevertheless, after its Q2 earnings report on July 26—which highlighted a profit of $8.49 per share and revenue of $13.7 billion, both exceeding analyst expectations—shares surged by 16.6%. This positive result was chiefly attributed to effective initiatives that improved adjusted EBITDA by 2.6%, while also bolstering mobile service revenue despite losses in residential and small-to-medium business internet customers.

The overall sentiment from analysts remains cautious for Charter’s stock, with a prevailing “Hold” rating. Among 25 analysts, seven advocate for a “Strong Buy,” 13 recommend a “Hold,” and five advise a “Strong Sell.” This outlook is slightly more reserved compared to three months ago, when eight analysts favored a “Strong Buy.”

Currently, the average price target for CHTR stands at $370.09, indicating a potential upside of 13.5% from present trading levels.

More Stock Market News from Barchart

On the date of publication, Sohini Mondal did not hold positions, directly or indirectly, in any of the securities mentioned in this article. All information and data presented here are for informational purposes only. For more details, please refer to the Barchart Disclosure Policy here.

The views and opinions expressed herein are solely those of the author and do not necessarily reflect the stance of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.