The ASML Success Story

A few days ago, I penned an article proclaiming TSMC (TSM) as the world’s most crucial company. This undoubtedly sparked debates about ASML Holding N.V. (NASDAQ:ASML) potentially holding that title. The truth is, both companies are linchpins of our global economy.

ASML’s resounding success stems from its foresight and astute capital allocation over the decades. This strategic prowess has primed them with an unrivaled advantage, a bulwark in an industry poised for exponential growth.

In a strategic coup in 2017, ASML acquired a 24.9% stake in Carl Zeiss SMT GmbH for €1 billion. This move secured ASML’s critical supply chain element – Lithography Optics. Zeiss has been the bedrock of ASML’s market dominance since 1983, playing an indispensable role in their technological supremacy. Without Zeiss, ASML wouldn’t enjoy the commanding edge it holds today.

This dependency is further cemented by ASML’s recent acquisition of Berlin Glas Group, a German company specializing in ceramic and optical modules. Each strategic move further fortifies ASML’s competitive edge.

Despite naysayers fearing ASML’s exposure to Taiwan and China, the company’s long-term approach and stellar risk management instill confidence. Many overlook the fact that their entire portfolio may be entwined with the same geo-economic risks.

Financial Fortitude and Metrics

ASML’s conservative financial approach is a testament to its prudence. With a mere $5.28 billion in long-term debt and a current cash position of $5.26 billion, the company stands strong with a robust balance sheet.

Even when delving deeper and excluding cash, ASML’s net income to long-term debt ratio paints a more remarkable picture. With a TTM net income of about $8 billion, well exceeding its debt, ASML proves its mettle. The balance sheet remains steadfast, even in adverse conditions. In December 2020, their net income of $4.34 billion still comfortably stays below the threshold for net income to be less than four times debt.

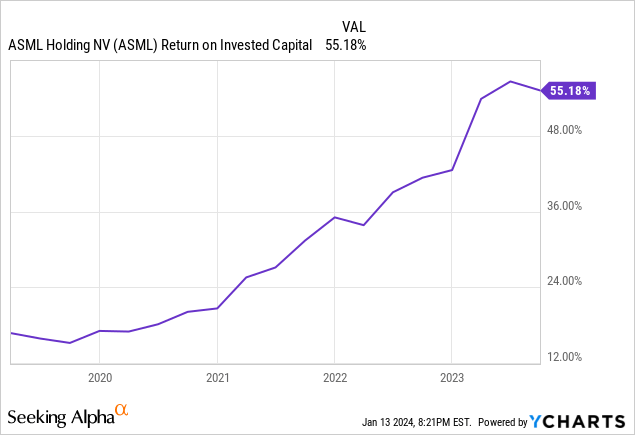

ASML’s alignment of shareholder and management interests is equally striking. Return on average invested capital (“ROAIC”) stands as one of the performance targets, a move lauded for its long-term benefits to shareholders. With a 30%+ target, achieving this should significantly create value for shareholders.

ASML’s critical dependence on knowledge and superior technology renders technology leadership imperative. Nonetheless, their total shareholder return targets might benefit from a different approach.

ROIC and Capital Management

ASML’s robust return on invested capital (ROIC) over the last 5 years, coupled with a relatively low cost of capital, highlights their efficient capital utilization. With a WACC of about 10%, the ROIC-WACC spread stands at an impressive 45%, underscoring ASML’s competitive advantage. Such efficient capital use amid vast growth opportunities bodes well for shareholders.

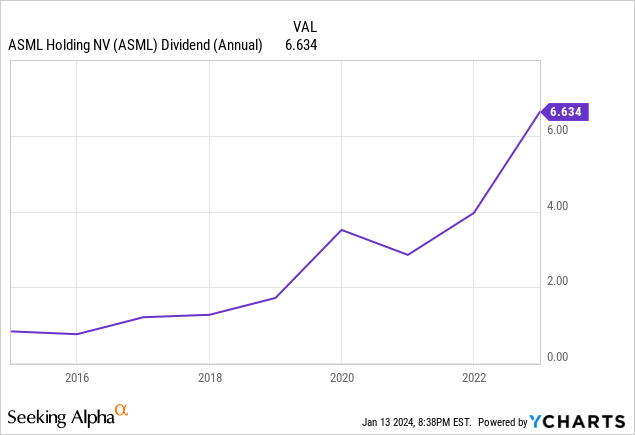

Additionally, ASML boasts an impressive 10-year dividend growth CAGR of 25.05%. While the current dividend yield stands at 0.9%, its consistent growth promises to augment total shareholder return significantly.

ASML: Shaping the Future of Semiconductor Industry

As if the stars have aligned, ASML, the Dutch semiconductor equipment giant, seems to be on a trajectory of unwavering success. Let’s delve into the company’s financial prowess and the factors contributing to its future growth.

Capital Allocation and Shareholder Value

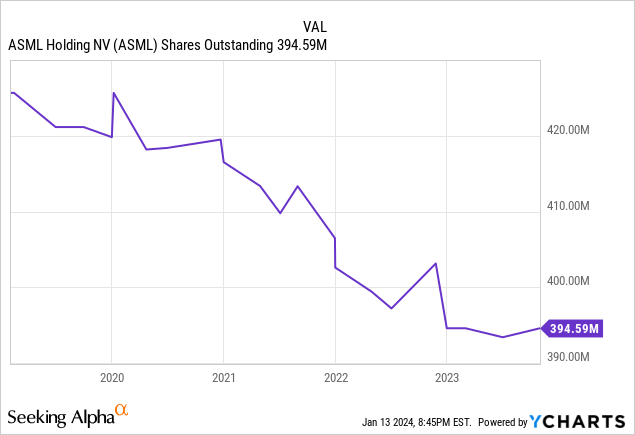

With ASML, investors need not fret over excessive stock-based compensation diluting their stakes. Notably, the company has exhibited a steady reduction in its share count over the past five years, indicative of prudent capital management and a friendly approach towards shareholders.

According to management, the top three priorities for capital allocation include investing in the business, bolstering the dividend, and share buybacks. However, due to the prevailing economic environment, ASML has temporarily curtailed its buyback initiatives to redirect capital into other strategic areas.

The company’s robust dividend growth, coupled with high returns on capital and diminishing share count, signifies a compelling investment proposition. The only missing piece of the puzzle seems to be a conducive valuation multiple for potential expansion – a trifecta that remains elusive, but not inconceivable.

ASML currently carries a price-to-earnings (P/E) multiple of 34x, constraining the prospect of multiple expansion, despite witnessing higher multiples in recent years. However, stakeholders stand to gain from the company’s earnings and dividend growth, given its strong competitive advantage. A P/E ratio in the thirties seems reasonable for a company of such towering strength.

Returning Wealth to Shareholders

A testament to ASML’s commitment to rewarding its shareholders is evident in its substantial capital returns trajectory. Over the past decade, the company has escalated its wealth distribution from €5 billion to a staggering €30 billion, with dividends claiming an increasingly significant portion, underpinned by remarkable growth rates.

ASML’s Reverse DCF

A reverse discounted cash flow (DCF) analysis unveils that the stock is currently factoring in an earnings-per-share (EPS) compound annual growth rate (CAGR) of 14% over the next decade. However, ASML has historically achieved an exceptional 28% EPS CAGR since 2018, signaling that the stock appears undervalued if it can sustain its historical growth trajectory. Moreover, the impending improved margins from the 3800 series and the array of growth opportunities are poised to facilitate ASML in maintaining its historical CAGR.

Future Earnings Projections

Despite a flat guidance for 2024, ASML finds itself in a typical phase of the industry cycle, characterized by customer deferment of purchases and pre-sanction bulk acquisitions by Chinese enterprises. This cyclical pattern presents an opportune moment for investors to seize the upcoming segment of the cycle, typically aligned with stagnant revenues.

It’s imperative to assess the forward P/E for 2025 and beyond, as market dynamics could distort the current multiple. Future earnings are poised to steer the stock price, rather than being tethered to the preceding year’s earnings. ASML is primed with ample momentum, poised to benefit from various subsidy programs in the semiconductor industry, concomitant with the escalating demand for its pioneering technologies in spheres like AI, hyperconnectivity, and energy transition.

Risks and Mitigation

In the face of prevailing apprehensions regarding the China risk, ASML’s revenue exposure from the region remains historically limited. The recent export bans may lead to a marginal dip in revenue from China, mitigated by substantial investments anticipated from the likes of Intel and Samsung. Furthermore, the company’s unwavering commitment to innovation has favored a robust customer retention, albeit posing a challenge to prompt recurrent machine purchases.

Another lurking risk pertains to the disruption posed by quantum computing, with the landscape potentially undergoing transformative shifts. ASML finds itself pitted against formidable tech titans like Google, Amazon, and IBM, adding an element of unpredictability to the competitive milieu.

In Conclusion

Even in the hypothetical scenario of complete revenue erosion from China and Taiwan, ASML is positioned as the vanguard in semiconductor equipment, symbolizing unparalleled demand. The company’s acumen in leveraging adversity to augment its strengths is evident in its foresight to invest in Carl Zeiss SMT GmbH, casting a sanguine outlook even amidst export bans and geopolitical flux.