**Qualcomm Q2 2026 Revenue Report**

Qualcomm Incorporated (QCOM) reported $9.08 billion in revenue for its Qualcomm CDMA Technologies (QCT) segment in Q2 2026, a 4% decrease year over year. The QCT earnings before tax (EBT) margin fell to 27% from 30% due to lower demand in the handset market, compounded by memory supply constraints and rising prices. Ships to China also decreased, reflecting a temporary inventory adjustment rather than a structural demand decline.

Conversely, Qualcomm’s automotive sector demonstrated strong growth, with revenues increasing 38% year over year to $1.3 billion, driven by new digital cockpit and Advanced Driver Assistance Systems (ADAS) launches. Additionally, the IoT segment saw a 9% revenue increase to $1.73 billion, supported by rising demand for edge AI applications. The company anticipates ongoing smartphone market challenges into Q3 2026.

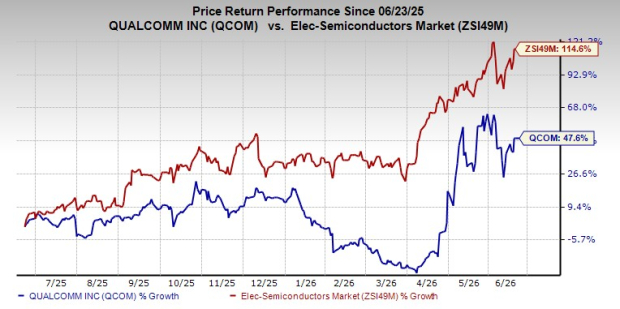

Qualcomm’s share price has risen 47.6% over the past year, compared to the industry growth of 114.6%. The current price-to-earnings ratio stands at 20.88, significantly lower than the industry’s 37.82. However, earnings estimates for fiscal 2026 and 2027 have been revised downward over the past two months.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.