Atlantica Sustainable Infrastructure plc (NASDAQ:AY) operates as a green energy company, with a robust portfolio encompassing 2.2 GW of operating assets across renewable, natural gas, transmission line, and hydro assets.

The majority of their assets are linked with renewables, constituting approximately 70% of the total portfolio.

In the turbulent world of green and renewable energy, Atlantica’s business model adheres closely to the standard industry framework, revolving around energy generation and the development and retention of a green asset portfolio through project finance, backed by retained cash flows providing the initial equity component in joint ventures and ring-fenced vehicles.

The energy produced is primarily sold through Power Purchase Agreements (PPAs), which not only mitigate market risk but also enhance the attractiveness of Atlantica’s projects in the eyes of lenders, who seek certainty in cash flow generation.

Adding to this, Atlantica also holds a 27% asset exposure to natural gas and transmission lines, acting as solid diversifiers to the renewable asset base.

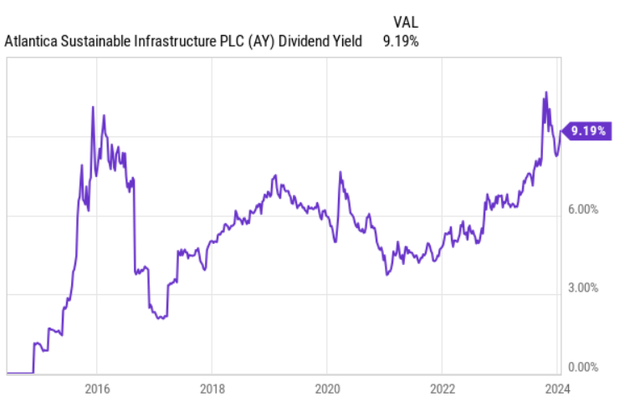

The Safety of Atlantica’s Dividend Yield

Against this backdrop, we delve into the safety of Atlantica’s current dividend yield of 9%, despite concerns raised by a yield approaching 10%, a 29% drop in share price over the TTM period, and a history of dividend cuts, notably in 2016. To support our position, let’s explore three reasons why Atlantica’s current dividend yield could be considered secure.

While the potential for stock price appreciation is a point of contention, sustained current yield levels remain alluring to long-term and dividend-seeking investors, justifying a bullish investment thesis. The same elements that bolster the case for Atlantica’s dividend stability are likely to act as catalysts for stock price appreciation.

#1: Consistently Stable Cash Flows

An essential driver behind dividend cuts is declining cash generation, rendering dividend distributions unsustainable. However, Atlantica’s top line has maintained a fairly stable and predictable trajectory, exhibiting resilience against market risk. Quarterly adjusted EBITDA has demonstrated stability and marginal growth since Q1, 2021, without significant disruption.

Power Purchase Agreements (PPAs) have been pivotal in sustaining this stability, being a feature for nearly the entire renewable asset base, except for three ~50MW assets. The aggregate structure of these PPAs at a relatively tight pricing range has contributed to the overall stability, evident in historical EBITDA figures. Furthermore, all PPAs carry a duration profile exceeding project-level debt, mitigating volatility in market prices after neutralizing financial risk on a specific asset level.

While the context of EBITDA must be weighed against interest expense due to Atlantica’s leveraged business, this is better addressed in the next point.

#2: Prudently Leverage Management

Atlantica’s reliance on ring-fenced project financing structures has restrained heavy external debt burdens at a corporate level. Instead, it absorbs minor portions of debt on its books, blending these with retained cash flows to form equity injected into joint ventures or fully owned subsidiaries, serving as a base for new borrowings in an isolated manner from Atlantica’s structure.

Amidst notable leverage, nearly the entire chunk of Atlantica’s debt is either fixed via the issuance of fixed-rate project finance debt or hedged through interest rate derivatives, effectively achieving a similar outcome. This prudent approach mitigates the exposure to interest rate fluctuations, sustaining a virtuous cycle of secure financial positioning.

Continued on page 2…

Continuation

AY, one of the leading names in the renewable energy industry, has showcased an impressive resilience in its expense position, a noteworthy feat considering the prevailing higher interest rates and constrained financing environment. Despite these challenges, AY’s expense position has remained remarkably flat, demonstrating a robust financial stance in the face of adversity.

Financial Risk Neutralized

One key aspect contributing to AY’s formidable financial stance is the neutralization of financial risk on its renewable asset base level. AY has successfully attracted Power Purchase Agreements (PPAs) that sufficiently cover the financial costs, effectively mitigating interest rate risks and ensuring a stable financial position.

Moreover, the calibration of financial costs in accordance with the incoming cash flow levels from PPAs further bolsters AY’s position, fortifying the company against potential interest rate fluctuations.

Additionally, from a corporate-level debt structure perspective, AY has strategically positioned itself with the majority of its debt considered as an asset, given the favorable interest rates at which it was secured. The proactive approach to securing fixed-rate financing prior to aggressive interest rate hikes has significantly bolstered AY’s financial position, instilling confidence in the stability and resilience of its corporate debt structure.

Portfolio Expansion Driving Cash Generation

AY’s proactive expansion and growth-oriented initiatives have positioned the company for incremental cash generation, underpinning its ability to cover dividend payouts and fuel future growth. With a substantial pipeline of approximately 2 gigawatts (GW) – nearly on par with its current generation capacity – AY is poised for significant growth.

While the pipeline projects are still in their early stages and may take several years to reach their commercial operation dates (CODs), AY’s strategic foresight and extensive pipeline provide a strong foundation for sustained growth and profitability.

Despite the capital-intensive nature of these expansion projects, AY’s robust financial position, backed by available liquidity and retained cash flows, provides the company with the necessary resources to finance and navigate through this expansion phase effectively.

The Verdict: AY is a Compelling Buy

In light of these compelling factors, AY’s dividend yield of approximately 9.2% with a CAFD (Cash Available for Distribution) payout of around 85% appears to be on solid ground. The well-structured leverage profile and locked-in positive cash flows, poised for growth, are expected to propel AY’s ability to not only sustain its existing yield but also enhance it in the future.

In conclusion, AY’s resolute financial position, poised for growth, makes it a compelling buy in the current market landscape, reflecting the company’s potential to soar amidst the challenges and seize opportunities in the renewable energy sector.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.