Driving Momentum with Innovative Products

Axon Enterprise, Inc. has been on a winning streak with its TASER segment, fueled by soaring demands for devices and cartridge products. The steady interest in virtual reality training services has also been a boon. Furthermore, Axon Evidence and cloud services are witnessing remarkable growth, thanks to the escalating number of users, augmented average revenue per user, and software add-ons.

The infusion of investments in product innovations, automation, and manufacturing efficiency is poised to trigger growth for AXON. For instance, the rollout of Axon Body 4 in April 2023 has set a new benchmark. Packed with advanced features like a bi-directional communications facility and a point-of-view camera module option, this body camera has been in hot demand, driving the segment’s expansion.

Axon’s strategy of integrating complementary businesses through acquisitions has paid off handsomely. The acquisition of Sky-Hero in July 2023, renowned for its drones and ground-based vehicles, has enriched Axon Air portfolio, providing a valuable edge in the endeavor to safeguard life and march toward its ambitious goals.

Upbeat Guidance Amid Challenging Terrain

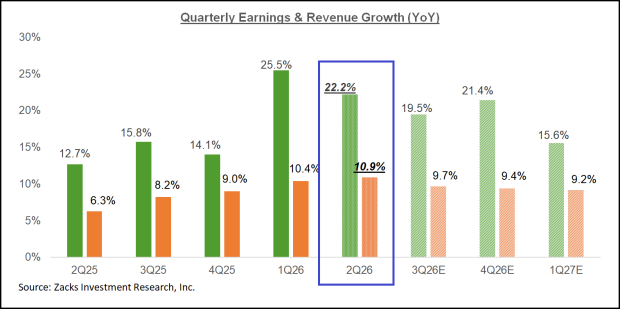

Despite the headwinds, AXON’s management remains optimistic about the path ahead. The company foresees robust growth in 2024, with revenue expectations ranging from $1.88 billion to $1.94 billion, marking an impressive 20-24% surge from the previous year. The adjusted EBITDA projection for 2024 stands at $410-$430 million, accompanied by a promising margin expansion compared to 2023.

Image Source: Zacks Investment Research

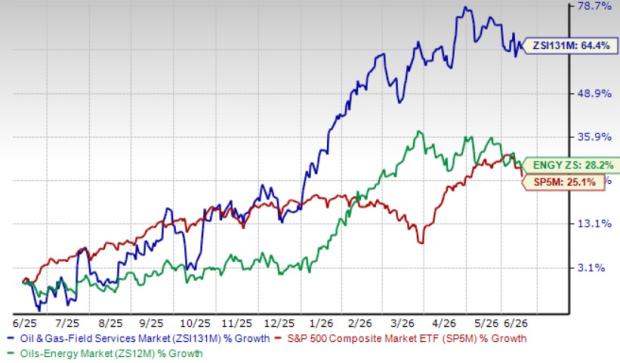

Market Performance and Risk Factors

Over the past three months, with a Zacks Rank #3 (Hold), Axon Enterprise has outpaced the industry, registering a 24.7% upswing against the sector’s 12.9% growth.

However, challenges loom, with stagnant demand for the TASER 7-series posing a hurdle. The company noted flat sales from TASER 7 in the fourth quarter of 2023, signaling a need for strategic recalibration. Furthermore, the substantial investments in research and development could exert pressure on Axon Enterprise’s profitability. In 2023, research and development expenses surged by 29.9%, amounting to $303.7 million.

Encompassing a broad international footprint exposes AXON to risks associated with adverse foreign currency fluctuations. A robust U.S. dollar could potentially crimp profit margins in global markets outside the United States.

Promising Picks in the Arena

For investors seeking opportunities in the same realm, a few standout stocks are worth considering:

MSA Safety Incorporated, with a Zacks Rank #1 (Strong Buy), has consistently surpassed earnings expectations, with a trailing four-quarter average earnings surprise of 21.8%. The Zacks Consensus Estimate for its 2024 earnings has been on an upward trajectory.

Cadre Holdings, Inc. currently holds a Zacks Rank of 2 (Buy) and has been delivering solid earnings surprises, with room for growth in its 2024 estimates.

With a Zacks Rank #2, Powell Industries, Inc. boasts an excellent track record of earnings surprises. The Zacks Consensus Estimate for its fiscal 2024 earnings has remained stable recently.

Striking a Balance Amid Challenges

Key Takeaway: Axon Enterprise’s journey is a fascinating rollercoaster ride, marked by triumphs and trials. Despite challenges, the company’s relentless focus on innovation and strategic expansion continues to drive growth and resilience.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.