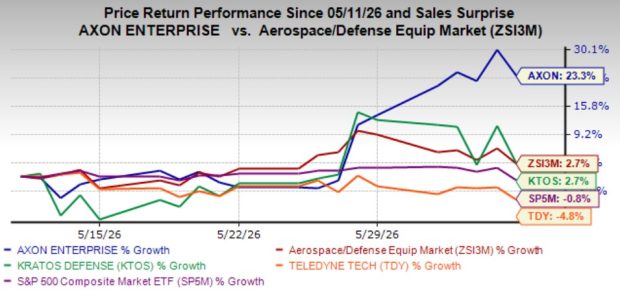

Shares of Axon Enterprise, Inc. AXON have been showing impressive gains of late, rising 23.3% in the past month. Shares of the public safety technology solution provider have outpaced the Zacks sub-industry’s growth of 2.7% and the S&P 500 composite’s 0.8% decline. The company has also outperformed other industry players like Kratos Defense & Security Solutions, Inc. KTOS and Teledyne Technologies Incorporated TDY, which have returned 2.7% and declined 4.8%, respectively, over the same time frame.

AXON Stock’s Price Performance

Image Source: Zacks Investment Research

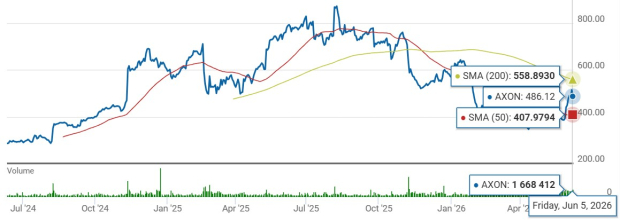

Closing at $486.12 yesterday, the Stock is trading below its 52-week high of $885.92 but higher than its 52-week low of $339.01. Although the Stock is hovering above its 50-day moving average, it is trading below its 200-day moving average.

AXON Shares’ 50-Day and 200-Day SMA

Image Source: Zacks Investment Research

What’s Behind AXON Stock’s Momentum?

The strongest driver of Axon’s business at the moment is the solid momentum in its Connected Devices segment. The company continues to witness solid demand for its next-generation TASER 10 products, whose shipment began in 2023. Growth in cartridge revenues, driven by higher adoption of the TASER products, has been driving the segment’s performance.

Solid demand for its next-generation body-worn camera, Axon Body 4, virtual reality training services and counter-drone equipment also supports its growth. Segmental revenues surged 32.8% year over year in the first quarter of 2026, following an increase of 29.1% in 2025.

The company is also witnessing persistent strength in its Software & Services segment, driven by an increase in the aggregate number of users to the Axon network. Continued momentum in digital evidence management and increased adoption of its latest software offerings are driving the segment’s growth.

Existing customers are consistently returning to purchase additional services, reflecting strong customer satisfaction and engagement. This ongoing expansion supports a growing base of annual recurring revenue (ARR). After witnessing a year-over-year 39.6% jump in 2025 revenues, the metric increased 35% in the first quarter of 2026.

AXON remains focused on strategic collaborations with other companies to expand its product offerings and customer base. In October 2025, Axon’s Dedrone business announced its partnership with TYTAN (a leading provider of interceptor systems for Group 3 drones) to boost detection, identification and mitigation capabilities of counter drone equipment. The integration of TYTAN’s kinetic interceptor technology enhanced Dedrone’s Counter-Unmanned Aircraft Systems (CUAS) mitigation capability, making it suitable to deploy against Group 3 threats.

Axon’s acquisition of Carbyne (in February 2026) also enabled it to come up with Axon 911, a state-of-the-art, fully integrated solution that is designed to connect callers and responders instantly. Growing popularity for its Dedrone platform across several sectors also bodes well. The company currently expects revenues to increase approximately 30-32% year over year, higher than 27-30% predicted earlier.

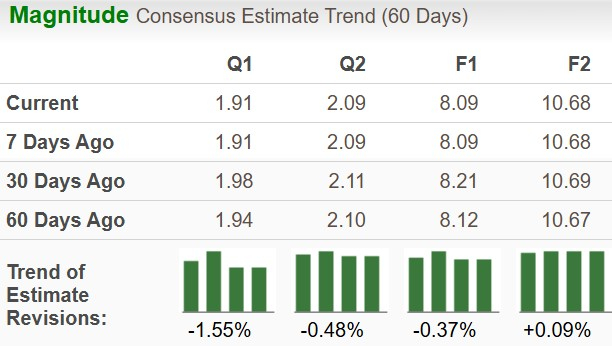

AXON’s earnings Estimate Revision

The company’s earnings estimates for 2026 have inched down 0.4% to $8.09 per share over the past 60 days. However. the figure indicates year-over-year growth of 18.1%.

earnings estimates for 2027 have moved up 0.1% to $10.68 per share. The figure also indicates year-over-year growth of 32%.

Image Source: Zacks Investment Research

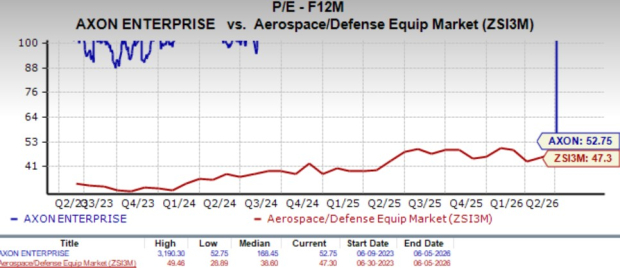

Valuation Remains an Overhang

The Stock is trading at a forward 12-month price-to-earnings (P/E) ratio of 52.75X, higher than the industry average of 47.30X. This elevated valuation could make the Stock vulnerable to further pullbacks if market sentiment sours.

While its peer, Teledyne Technologies, is trading cheaper compared with AXON, Kratos Defense is trading at a premium. Notably, Teledyne Technologies and Kratos Defense are trading at 24.23X and 67.72X, respectively.

Image Source: Zacks Investment Research

Should You Buy AXON Stock Now?

Robust momentum across Axon’s TASER and Software & Sensors segments, along with its investments in AI products, drones and robotics, positions it favorably for impressive growth in the quarters ahead. The company’s strategic acquisitions and collaborations with other companies to expand product offerings should also support its top-line performance.

Despite its expensive valuation, positive analyst sentiment and robust growth prospects indicate it is the right time for potential investors to bet on this Zacks Rank #1 (Strong Buy) company. You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI’s Second Wave Is here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

see Stocks Now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Teledyne Technologies Incorporated (TDY) : Free Stock Analysis report

Kratos Defense & Security Solutions, Inc. (KTOS) : Free Stock Analysis report

Axon Enterprise, Inc (AXON) : Free Stock Analysis report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.