Salesforce (NYSE: CRM) and Veeva (NYSE: VEEV) are two giants in the cloud-based customer relationship management (CRM) industry. According to Gartner, Salesforce boasts a significant market share, far surpassing that of its competitors, while Veeva caters primarily to life science companies.

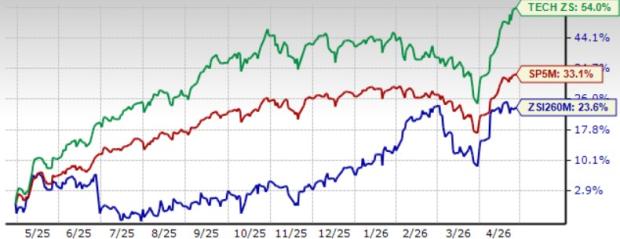

Despite its smaller size, Veeva owes its existence to Salesforce, as it was founded by Salesforce’s former senior VP of Technology, Peter Gassner, who continues to lead as its CEO. The relationship between the two companies remains intertwined, with Veeva relying on Salesforce’s platform for some of its operations. However, recent stock performance tells a diverging tale – over the past year, Salesforce’s stock surged 74%, outshining Veeva’s more modest 39% rally. Let’s delve into why the market leader outpaced its niche counterpart by such a considerable margin and assess which is the more promising investment.

Image source: Getty Images.

Salesforce’s Margin Evolution Amid Shifting Growth Trajectory

In addition to its CRM platform, Salesforce offers various other cloud-based services spanning sales, marketing, e-commerce, analytics, collaboration, and data visualization. These segments faced challenges due to macroeconomic headwinds that constrained software expenditures.

While Salesforce witnessed a 25% revenue increase in fiscal 2022, subsequent years saw a slowdown with growth rates of 18% in fiscal 2023 and 11% in fiscal 2024. Projections for fiscal 2025 suggest a moderate 8%-9% growth, unsettling growth-focused investors. However, the company implemented strategic measures such as workforce reductions, cost reductions, halted major acquisitions, initiated share buybacks, and launched its inaugural dividend to bolster margins.

This transformation led to a remarkable expansion in Salesforce’s adjusted operating margin, which surged from 18.7% in fiscal 2022 to an impressive 30.5% in fiscal 2024. Adjusted EPS followed suit by rising 10% in fiscal 2023 and skyrocketing 57% in fiscal 2024 post a 3% dip in the preceding year. Analysts forecast a further 19% growth in adjusted EPS for fiscal 2025.

While Salesforce is transitioning towards earnings-driven growth, the evolution of its Einstein AI services is expected to fortify customer retention and widen its competitive moat. Despite these promising prospects, the stock’s valuation at 31 times forward earnings and a modest 0.5% forward dividend yield might deter income-minded investors.

Veeva’s Resilience Amid Market Challenges

Veeva holds a pioneering position in the life sciences CRM landscape, offering cloud services in storage and analytics. However, it encountered headwinds in the past year as macro factors led clients to downsize sales operations, curtail spending on new projects, and focus on lengthier R&D ventures, impacting revenue recognition. Additionally, soaring interest rates constrained smaller biotechs from expanding through fresh capital infusion.

With a revenue surge of 26% in fiscal 2022, Veeva’s growth slowed to 16% in fiscal 2023 and 10% in fiscal 2024. The company anticipates a rebound with revenue growth projected at 15%-16% this year, driven by a more favorable economic backdrop and the implementation of enhanced AI capabilities.

Unlike Salesforce, Veeva’s deceleration did not attract attention from activist investors. Opting not to aggressively slash costs, initiate significant buybacks, or introduce a dividend during the growth slowdown, Veeva observed a contraction in its adjusted operating margin from 41% in fiscal 2022 to 35.6% in fiscal 2024. The company’s adjusted EPS expanded by 27% in fiscal 2022, but growth rates tapered to 15% in fiscal 2023 and 13% in fiscal 2024. Analysts project a resurgence in fiscal 2025 with a 27% growth expectation as revenue acceleration kicks in. Despite the positive outlook, Veeva’s valuation at 38 times forward earnings suggests it may not be a budget-friendly choice.

The Verdict: Salesforce Reigns Supreme

While the decision may seem challenging, my conviction lies in Salesforce’s potential to outshine Veeva this year, driven by its diversified business model, robust earnings growth, and relatively attractive valuation. Veeva remains a solid long-term bet in the life sciences CRM arena but requires accelerated growth to justify its premium price tags.

Considering an investment in Salesforce? Here’s a tip:

As you ponder over investing in Salesforce, bear in mind that the Motley Fool Stock Advisor team has identified what they believe are the 10 best stocks for investors at present – with Salesforce not making the cut. The recommended stocks have the potential to yield significant returns over the coming years.

The Stock Advisor service offers a user-friendly roadmap to success, featuring portfolio building guidance, regular analyst updates, and two fresh stock picks each month. Since 2002, the Stock Advisor service has outperformed the S&P 500 by more than triple.*

Explore the top 10 stocks today

*Stock Advisor returns as of March 11, 2024

Leo Sun holds positions in Veeva Systems. The Motley Fool holds positions in and recommends Salesforce and Veeva Systems. The Motley Fool endorses Gartner. The Motley Fool upholds a disclosure policy.

The author’s views expressed herein are personal and not necessarily representative of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.