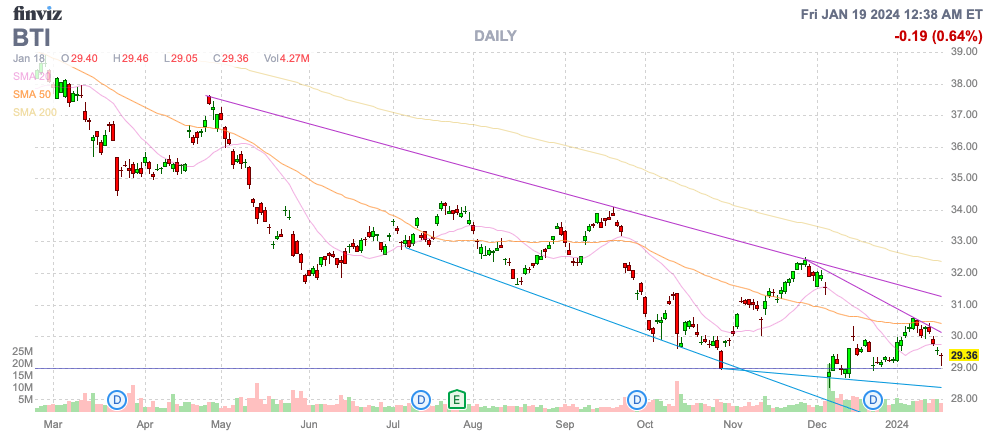

British American Tobacco p.l.c. (NYSE:BTI) has been a rollercoaster for shareholders, despite the lure of large dividend payouts. The company’s recent erratic performance can be likened to the wild swings of a pendulum, leaving investors reeling.

Curious Investments

In a surprising move, British American Tobacco has doubled down on the cannabis industry, with additional investments in Organigram (OGI), despite a previously rocky foray into the sector in March 2021. This shift raises questions about the company’s commitment to its stated goal of steering towards a smokeless world, while making moves that seem to align it back with consumers who favor traditional smoking methods.

BAT’s decision to invest a substantial amount – £74m (C$125 million) – between January 2024 and January 2025 to increase its equity position in Organigram from 19% to 45%, has left many scratching their heads. Moreover, the original investment of £126 million, priced shares at C$3.79, yet the stock now trades at C$2.25 following a rally after BAT’s cash infusion.

Additionally, as the world edges closer to making cigarettes obsolete, BAT’s recent move to write down U.S. tobacco brands to the tune of $31.5 billion, and its plans to completely write off these brands worth $80 billion on the balance sheet over the next 30 years, have only added to the confusion and skepticism among investors.

It is important to note that presently, only 12% of BAT’s sales are derived from new product categories. Therefore, the decision to write off valuable U.S. brands to zero by 2053, as well as the reliance on vape and menthol products in the new categories, has left shareholders wary.

Contradictory Messages

BAT’s CEO’s contradictory statements further added fuel to the fire. While acknowledging the declining value of the U.S. brands, the CEO expressed doubt about the disappearance of combustible cigarettes in 30 years, leaving investors perplexed about the company’s vision and strategy.

I’m not saying that we – the combustible, the cigarettes will disappear in 30 years in the US. I really don’t believe that, but you cannot justify the value of those brands equating to a number as equivalent to what we have today in the balance sheet.

Thus, the recent investments in Organigram to pivot away from combustibles, juxtaposed with the signaling of the company’s uncertainty about the decline of traditional cigarettes, have raised serious implications about the soundness of the company’s decisions.

Struggles with Dividends

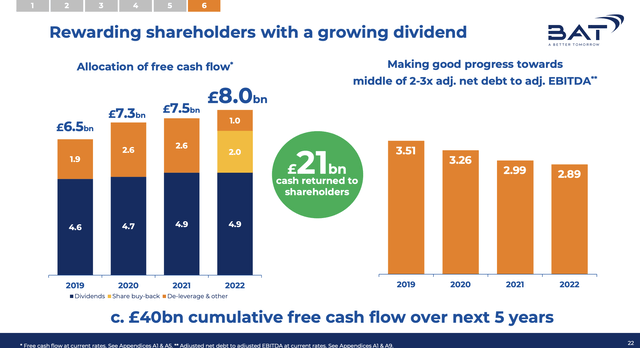

BAT’s situation reflects the broader challenge faced by companies struggling to balance large dividend payouts with high debt levels. Despite hiking dividend payouts from £4.6 billion in 2019 to £4.9 billion in 2022, the company’s leverage ratio remains relatively high at 3x. To exacerbate matters, the management allocated over $1.0 billion annually to share buybacks, instead of prioritizing debt reduction – a move that has left shareholders disillusioned.

At a time when the imperative for a business struggling to grow should be focused on debt reduction, BAT’s allocation of resources towards share buybacks has drawn criticism. The company’s current net debt of £37,259 million coupled with the unsettling message regarding the future of its valuable brands has left investors understandably concerned about its ability to restructure and manage its debt effectively.

Valuation Disparities

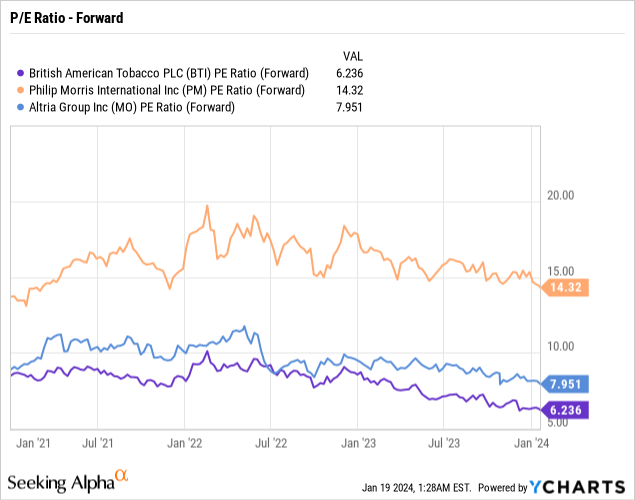

Comparatively, British American Tobacco Inc. remains at a substantial discount to Phillip Morris International (PM) and Altria (MO), primarily due to its limited non-combustible revenues and the recent unsettling disclosures. As Phillip Morris International is anticipated to register swifter growth in the future, the aggressive stance taken by BAT in the face of the burgeoning uncertainty has further weakened its standing in the market.

The relatively low dividend payout ratio of 65% should theoretically serve as a boon for BAT. However, this can only be expected to have a positive impact once the company effectively slashes its debt levels, potentially below the target of reaching 2.5x EBITDA, as per the current capital allocation strategy. The company’s projection to utilize excess cash flows for share buybacks and mergers and acquisitions when the leverage ratio hovers around 2.5x EBITDA is considerably flawed, thereby warranting a reevaluation of its capital allocation strategy.

Key Takeaway

BAT’s predicament underscores the importance of coherent communication from management to allay investor apprehensions. The recent perplexing forays into the Canadian cannabis industry, coupled with the devaluation of U.S. brands, have inadvertently projected a picture of faltering strength, not at all warranted by the company’s potential. A dividend yield as high as 10% often suggests weakness. Still, despite BAT’s recent missteps, its stock holds the promise of a substantial recovery if the company steers its ship in the direction of sound decisions and stable growth.