We perused the Global 100 list of most sustainable corporations by Corporate Knights and stumbled upon a surprise – SMA Solar Technology AG (OTCPK:SMTGF) (OTCPK:SMTGY). This European renewable energy player, often overshadowed by the likes of Enphase Energy (NASDAQ:ENPH) and SolarEdge (SEDG), had quietly made its mark.

We were taken aback by SMA Solar’s impressive progression and astoundingly reasonable valuation, offering exposure to markets similar to Enphase and SolarEdge. Encouraged by this, we kick-started our investment journey with a small stake in the company.

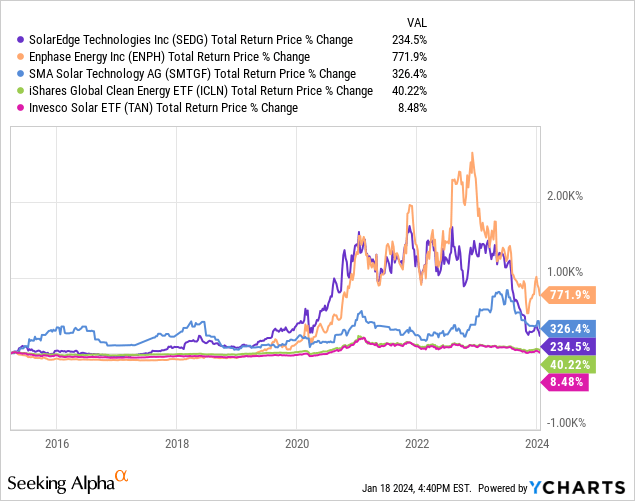

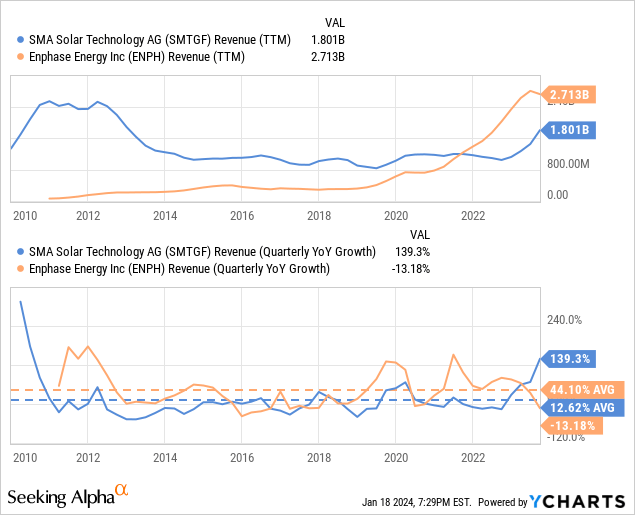

Strangely, SMA is not extolled as it deserves, even though its ten-year total return performance has been solid. It has lagged behind Enphase but outperformed SolarEdge and major clean energy ETFs.

Unearthing SMA’s Potential

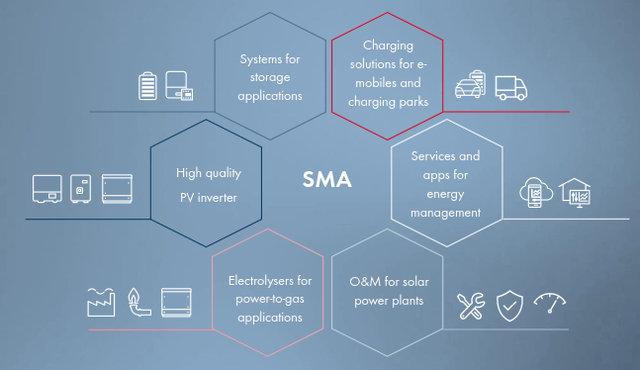

SMA defines itself as an “energy transition” company, offering a plethora of clean energy products and services. While primarily known for its solar inverters, it has been diversifying its portfolio to include energy management, boasting an installed base of over 120 GW of solar inverters across 190 countries.

The company’s strategic expansion includes ventures into electric vehicle charging solutions, hydrogen projects, and the integration of battery energy storage systems, a move that has fortified its competitive position. Moreover, SMA anticipates rapid growth across its business segments, with an average 21% CAGR through 2026.

Financial Fortitude

Although SMA’s financial results have notably improved, sustaining this upsurge remains uncertain. Yet, it’s compelling that profitability surged to 180 million Euros in the first nine months of 2023 from a meager 11 million Euros in the same period of 2022. Additionally, the company managed to reverse its free cash flow to 79 million Euros despite increased CapEx.

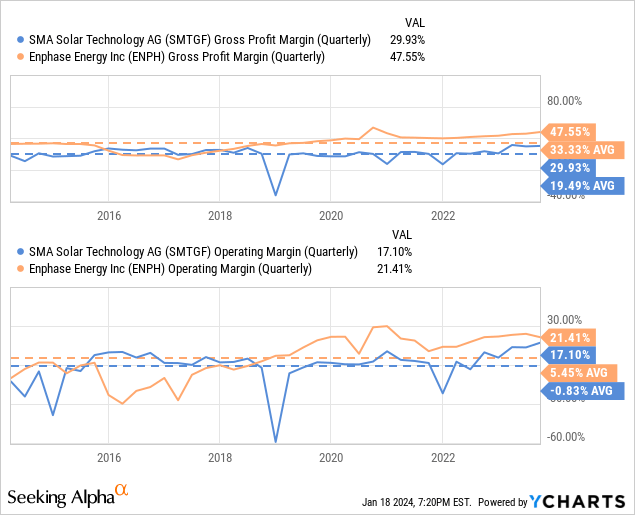

SMA’s gross margin, while showing improvement, still trails Enphase. The ascent to a gross margin 10% above its decade-long average is commendable, but it needs further progress to close the gap with its peer.

Revival and Rivalry

Enphase’s revenue growth has been staggering in recent years, but SMA has now begun to exhibit rapid growth, coinciding with Enphase’s struggle to maintain its previous momentum. This resurgence might signal SMA’s reclamation of lost market share.

Financial Foundation

Both companies exhibit robust balance sheets, with SMA carrying virtually no long-term debt and boasting a net cash position of approximately $300 million. In contrast, Enphase holds about $1.8 billion in debt, with a significant chunk offset by cash and short-term investments of nearly $1.3 billion, rendering the net debt eminently manageable given Enphase’s current EBITDA of almost $700 million.

The Evolution of SMA Solar Technology and Enphase Energy: A Valuation Comparison

Amidst the wax and wane of the energy management industry, SMA Solar Technology and Enphase Energy have found themselves riding the crest of a wave. Akin in some regards, yet disparate in others, these companies are expanding their dominion from simple solar inverter enterprises to comprehensive energy management juggernauts. The expansion has availed them the opportunity to augment their project revenues by integrating high-margin software and management services into their repertoire.

Enphase has opted for a CapEx-lite approach, eschewing large factories and diversifying its employee base to include a significant portion located in countries with lower average wages, such as India. While this strategy has been advantageous thus far, it is not without its perils. Some emerging economies are now tying clean energy incentives to local manufacturing, and with wages on an upward trajectory, the wage arbitrage advantage could be imperiled in due course.

Outlook and Industry Evolution

The prevailing outlook for both companies is bullish, buoyed by a robust global and local impetus for renewable energy. SMA Solar, in particular, stands to gain substantially from German and European initiatives. The United States is also incentivizing renewable energy through the Inflation Reduction Act.

Projections indicate an approximate twofold expansion in their end markets by 2026 when compared to 2022. According to SMA Solar, the industry is entering its fifth phase of evolution – a phase typified by more sustainable and lucrative growth, diverging from the initial solar boom that was excessively reliant on subsidies. This was followed by a trying period of industry-wide losses and consolidation post the financial crisis. A phase of steadier growth followed, albeit with caution. If SMA Solar’s prognosis is accurate, the dawn of a new era characterized by reduced production costs, augmenting production capacity, and skyrocketing demand could be upon us.

Encouragingly, there have been positive signals, such as SMA’s thrice-heightened full-year 2023 guidance. The fourth quarter is also anticipated to witness ongoing robust revenue growth and profitability, although the moderation of the order backlog in the third quarter does serve as a salutary note of caution.

Valuation Metrics

The most compelling reason to scrutinize SMA Solar Technology is its conspicuously attractive valuation, notwithstanding the magnitude of the prospective opportunities. Its price/book multiple currently stands lower than its five-year average, despite recent upswings in profitability. Furthermore, it pales in comparison to the price/book multiple at which Enphase is trading.

Of greater import, its price/earnings multiple is remarkably low, hovering around 7.7x, juxtaposed with Enphase’s ~27x. This acutely low price/earnings multiple precipitates profound skepticism among investors regarding the company’s capacity to grow, or even sustain its extant profitability.

This skepticism endures despite a sanguine stance from management about growth prospects, propitious industry tailwinds, and manifest gross margin improvements.

Another metric indicative of substantial undervaluation is the EV/Revenues multiple, which lingers at approximately 0.86x for SMA, a substantial discount to its historical average, and significantly inferior compared to Enphase’s multiple exceeding 5x.

Lastly, the price to cash flow from operations is below 12x for SMA, while Enphase stands at around 17x. Notably, both companies are trading at substantial discounts to their historical averages, despite the prevailing tailwinds in their sector.

Renewable Energy Industry Positioned for Growth

The solar industry has seen its fair share of sunny days and rainy spells. It has danced to the rhythm of subsidies, and swayed to the tune of market fluctuations. However, a remarkable shift is taking place – the cost of wind and solar energy is currently often lower than that of electricity from natural gas-powered plants. Such a transformation is no ordinary feat; it is akin to a caterpillar metamorphosing into a butterfly. This change has not only fortified the industry but compelled it to become more resilient and adaptable in challenging times.

Risks and Rewards

The renewable energy industry, while promising, has historically been subject to market fluctuation, heavily reliant on subsidies, and prone to cyclicality. However, with the cost of wind and solar energy now often trumping that of natural gas-powered electricity, the sector is carving out a more stable niche for itself. This transition has led to industry consolidation, strengthening the remaining companies, and inducing a heightened level of efficiency and adaptability. The risks, though not to be discounted, are mitigated by the companies’ robust brands and solid financial foundations. As the industry looks set to bask in its newfound prominence, the biggest risk beheld by companies such as Enphase is the elevated valuation despite a significant share price decrease. On the other hand, for SMA Solar Technology, the threat arises from considerably lower gross margins compared to Enphase, rendering it susceptible to a pricing war for market share.

The Path Ahead

Investors should take heed of SMA Solar Technology, which is displaying clear indications of a resurgent comeback and reigniting growth. The global market projection for PV inverters and complementary energy solutions indicates a doubling by 2026 compared to 2022. This fertile ground sets the stage for both Enphase and SMA Solar to substantially escalate their sales volumes. Their strategic shift towards offering complete energy solutions, as opposed to solely solar inverters, heralds a promising era. This new direction not only sets them apart in the market but also unlocks doors to high-margin prospects in software and services. As such, our appraisal maintains a ‘Hold’ rating for Enphase, given its relatively high valuation. However, we are initiating SMA Solar Technology with a ‘Buy’ rating, given its undervalued trading multiples coupled with visible signs of enhanced profitability.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.