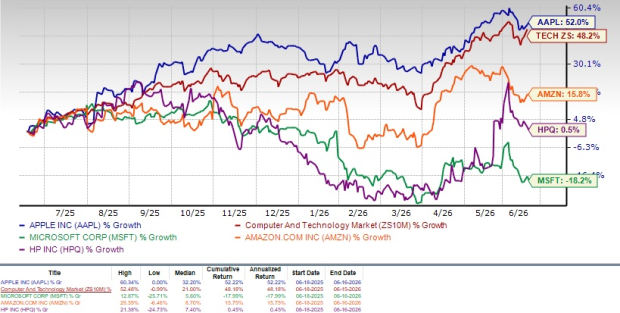

Apple Inc. (AAPL) has outperformed the Zacks Computer & Technology sector over the past year, with shares rising 52% compared to the sector’s 48.2% increase. The company’s success can be attributed to high demand for the iPhone 17 lineup, record growth in services revenues, which reached $30.98 billion in Q2 2026, and strong double-digit growth across geographical segments, including a notable performance in Greater China and India.

During the recent Worldwide Developers Conference (WWDC), Apple introduced significant updates to its AI capabilities, including enhancements to Siri and new AI-focused development tools for developers. The company’s Services division now contributes 27.9% of total net sales, underscoring its importance in Apple’s growth strategy. Looking ahead, the Zacks Consensus Estimate anticipates a 17.3% increase in fiscal 2026 earnings to $8.75 per share, with total revenues projected at $478.1 billion, marking a 14.9% growth over the previous fiscal year.

Despite strong performance, Apple shares are currently considered overvalued, trading at a forward P/E of 32.11, compared to the broader sector’s 25.36. However, the combination of sustained product demand, particularly in the iPhone and Services segments, along with the expanding AI innovations, positions Apple for continued growth and justifies its premium valuation.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.