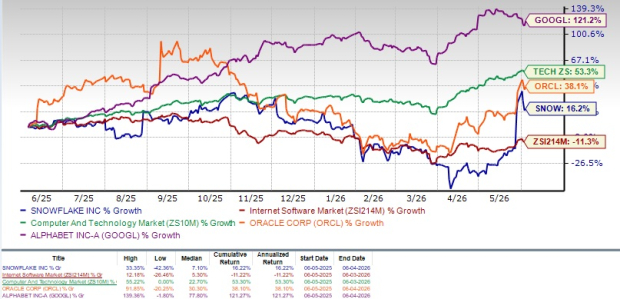

Snowflake Inc. (SNOW) reported a 16.2% increase in its share price over the past year, significantly underperforming the Zacks Computer and Technology sector’s 53.3% gain. The company’s quarterly revenue for fiscal Q1 2027 was $1.415-$1.420 billion, indicating a projected 30% growth compared to the previous year.

In the first quarter, Snowflake added 616 new customers, bringing the total to 13,912, a 38% year-over-year increase. The number of customers spending over $1 million annually increased by 29%, totaling 779, while those spending over $10 million rose to 64. The company’s net revenue retention rate stood at 126%.

Snowflake’s innovative AI product offerings, including Cortex Code, are driving customer engagement, evidenced by over 7,100 accounts using CoCo. Despite challenges such as lower gross margins on new AI products and significant competition, snowflake has a Zacks Rank of #3 (Hold), suggesting investors may want to await a better entry point. The company also maintains a forward Price/Sales ratio of 12.97X, indicating it is trading at a premium to the industry average of 3.96X.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.