“`markdown

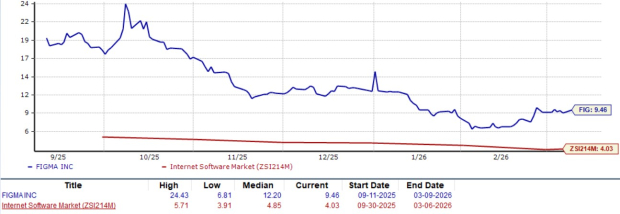

Figma, Inc. (FIG) has seen a staggering 75% decline in its stock price since going public, despite currently trading at a forward 12-month Price/Sales ratio of 9.46x, significantly higher than the Zacks Internet – Software industry average of 4.03x. The company reported a non-GAAP operating profit of $44 million for Q4 2025, marking a 22% year-over-year decline, while its non-GAAP operating margin fell to 14%, down 1,200 basis points from the previous year.

In 2025, Figma increased its acquisition activity, acquiring Weavy for over $200 million and Payload CMS to enhance its AI-related product offerings. However, these acquisitions have pushed Figma’s goodwill up from $11.38 million to $101.4 million within a year. Despite ending 2024 with 48% year-over-year revenue growth, figures for 2025 showed growth rates of 46%, 41%, 38%, and 40% across its quarters.

Analysts are recommending investors to avoid Figma, given its premium valuation against slowing revenue growth and increasing competition from larger players like Adobe, Microsoft, and Atlassian. The Zacks Consensus Estimate suggests a revenue growth rate of 29.8% for 2026, though bottom-line expectations indicate a decline of 23%.

“`