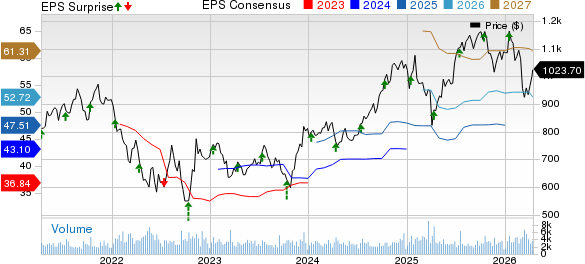

United Parcel Service (UPS) is trading at a forward 12-month price-to-earnings ratio of 13.76X, below the Zacks Transportation—Air Freight and Cargo industry’s average of 14.94X. The company is focusing on strategic shifts, particularly in healthcare logistics, aiming to double its healthcare revenues to $20 billion by 2026.

UPS plans to reduce its reliance on Amazon, targeting a $5 billion drop in Amazon-related revenue over two years and a more than 50% reduction in volume from Amazon by mid-2026. In conjunction, UPS intends to eliminate up to 30,000 operational jobs and freeze its quarterly dividend at $1.64 per share, raising questions about its short-term financial flexibility.

As of now, UPS faces challenges such as a 10.8% drop in average daily volumes in Q4 2025 and rising fuel costs, climbing over 50% in March alone due to geopolitical tensions. These factors complicate its near-term outlook, leading to a current Zacks Rank #3 (Hold).