The Evolution of General Electric

Throughout history, the aviation industry has held a captivating allure for investors and enthusiasts alike. In the case of General Electric (NYSE: GE), the past year has seen its stock skyrocket by an impressive 85%, showcasing a renewed confidence in the imminent restructuring within the organization. As GE Vernova, the power, renewable energy, and electrification arm, readies itself for its debut on April 2nd as an independent entity, the spotlight shifts to GE Aerospace, brimming with potential.

Despite the remarkable uptick in stock performance, the pertinent question looms: Is General Electric still a sound investment choice? Let’s embark on a journey to dissect the intricacies.

General Electric’s Breakup: A Divestiture Odyssey

Previous analyses have approximated GE Vernova’s market cap at a modest $27.3 billion. However, juxtaposed against the current $183 billion valuation, a lingering query emerges. Is the implied $155.7 billion valuation for GE Aerospace a realistic figure?

Decoding the Surge in General Electric’s Stock

The adrenaline-fueled surge in GE Aerospace’s valuation over the past year can be attributed to several factors:

- GE Aerospace’s operational prowess outshining competitors like RTX and Boeing in the commercial aerospace domain.

- Reduced exposure to margin and supply chain challenges that have plagued industry peers like RTX, Lockheed Martin, and Boeing.

- Investor sentiment veering towards valuing GE as “GE Aerospace+GE Vernova” distinct entities, hence imputing a corresponding valuation.

Amidst the tumultuous landscape, GE Aerospace has emerged unscathed, with competitors grappling with issues like engine contamination and operational snags. The pristine performance of GE Aerospace has elevated it to a favored position within the large-cap aerospace sphere.

GE Aerospace’s contender, RTX, grappled with a turbulent 2023 due to powder coating concerns, leading to profit erosion. In contrast, Boeing faces a multitude of production woes, casting shadows on its profitability outlook. GE Aerospace’s serene trajectory stands in stark contrast amidst the turbulence engulfing its peers.

Image source: Getty Images.

Judging the Worth of GE Aerospace

Companies within the aerospace realm command premium valuations owing to their long-term earnings potential. Engines are often sold at a loss upfront, with substantial revenue streams emanating from services over time.

As GE Aerospace wades through a period of heightened engine deliveries, profitability may be subdued in the short term. However, the adoption of a forward-looking lens reveals a verdant future beckoning GE Aerospace. Despite current valuation metrics indicating a lofty figure of $155.7 billion, the focus remains fixed on the anticipated free cash flow (FCF) projections for 2024.

|

GE Aerospace |

2023 |

2024 |

2025 |

|---|---|---|---|

|

Adjusted revenue |

$32 billion |

Anticipated growth in low double digits |

Anticipated growth in low double digits |

|

Operating profit |

$5.6 billion |

$6 billion to $6.5 billion |

$7.1 billion to $7.5 billion |

|

Free cash flow |

$4.7 billion |

$5 billion |

Exceeding 100% conversion from net income |

Data source: GE Aerospace presentations.

While current valuations may seem lofty, they align with industry standards for aerospace-centric entities. As GE Aerospace braces for a surge in engine deliveries and an evolving revenue mix, marginal pressures may ensue. Essentially, the current financial snapshot of GE Aerospace belies its latent potential and the propitious outlook that awaits.

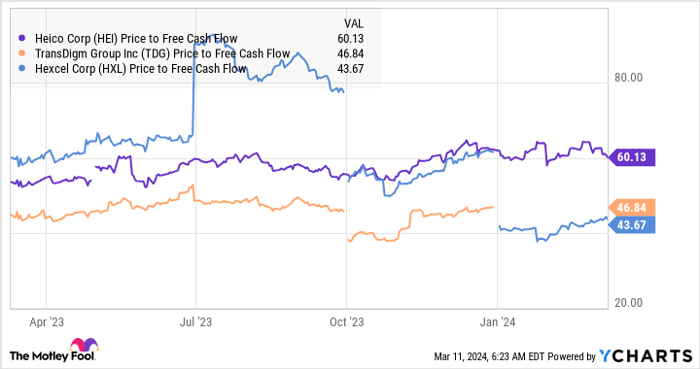

HEI price to free cash flow; data by YCharts.

Pondering General Electric’s Investment Appeal

With the numbers laid bare, General Electric stands at a pivotal juncture in terms of valuation. Analysts are cautiously optimistic, foreseeing a marginal upside potential in the stock price.

General Electric’s allure as a stalwart in the aerospace and defense domain has enhanced its valuation amidst the turbulent environments enveloping Boeing, RTX, and Lockheed Martin. However, the operational resurgence of these competitors could usher in a new narrative.

Envisioning the investment landscape post-spin, a valuation lower than $27.3 billion for GE Vernova presents an enticing prospect, while a figure below $155.7 billion for GE Aerospace may offer a semblance of upside potential.

Considering an investment in General Electric?

Before taking the leap, a comprehensive evaluation is prudent.

The Motley Fool Stock Advisor team has unearthed what they deem the 10 best stocks for prospective investors, with General Electric conspicuously absent from the list. These chosen stocks harbor the promise of colossal returns in the foreseeable future.

Stock Advisor extends a roadmap to success for investors, complete with portfolio-building strategies, expert insights, and bi-monthly stock recommendations, boasting returns that have outshone the S&P 500 by threefold since 2002*.

Explore the 10 stocks

*As of March 11, 2024, Stock Advisor returns have thrived.

Lee Samaha takes no financial stance on the stocks referenced. The Motley Fool endorses Heico, Hexcel, Lockheed Martin, RTX, and TransDigm Group. The Motley Fool upholds a transparent disclosure policy.

Author’s viewpoints do not reflect Nasdaq, Inc.’s views.