Inspire Medical Systems, Inc. INSP is perched for upward movement in the future, credited to its relentless focus on research and development (R&D). The positive outlook, fueled by a remarkable fourth-quarter 2023 performance and its extensive global footprint, is set to bolster its trajectory. Nonetheless, there are looming concerns about relying heavily on the Inspire system and external parties.

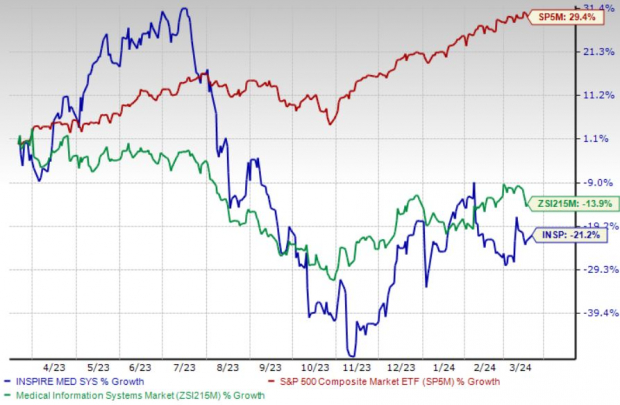

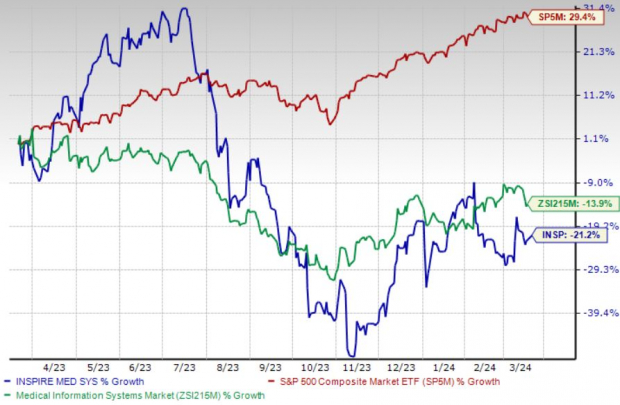

In the past year, this Zacks Rank #3 (Hold) stock has witnessed a 21.2% decline, in contrast to the industry’s 13.9% drop. Meanwhile, the S&P 500 has experienced a growth of 29.4% over the same period.

The distinguished medical technology establishment specializing in obstructive sleep apnea (OSA) boasts a market capitalization of $5.70 billion. With a projected growth of 47.2% for 2024, the company anticipates sustaining its robust performance. Impressively, Inspire Medical has surpassed earnings expectations by a staggering 353.6% over the last four quarters, on average.

Image Source: Zacks Investment Research

Let’s dig deeper.

Focusing on R&D: Inspire Medical’s core dedication to innovation and enhancing patient well-being propels its continuous product development, elevating our optimism. As management underscores, investing in existing and cutting-edge technologies is key to improving products and clinical outcomes, enhancing patient acceptance and comfort, and broadening the patient base that can benefit from Inspire therapy.

Global Reach: The management at Inspire Medical is actively strategizing to expand the company’s direct sales presence in terms of both size and geographical coverage to drive future revenue growth – a move that bodes well for the stock.

Throughout 2023, Inspire Medical activated 280 U.S. centers, bringing the total count to 1,180 U.S. medical centers conducting Inspire therapy implants as of December 31, 2023. Additionally, 62 fresh U.S. sales territories were established during 2023, tallying up to 287 U.S. territories by the end of December 31, 2023.

Robust Q4 Results: Inspire Medical’s stellar performance in the fourth quarter of 2023 fuels our confidence. The company saw significant growth in both top and bottom lines, with a notable uptick in U.S. revenues year-over-year. Despite rising product costs, there was observed expansion in gross margins.

The Downside

Heavy Reliance on Inspire System: The bulk of Inspire Medical’s revenues over recent years stemmed from sales of the Inspire system. Consequently, the company’s ability to execute its growth strategy and achieve profitability hinges on the adoption of Inspire therapy for treating moderate-to-severe OSA cases in patients unable to use or consistently benefit from continuous positive airway pressure. There’s uncertainty about the broad market acceptance of Inspire therapy among both physicians and patients.

Dependency on External Entities: Inspire Medical leans on third-party suppliers and contract manufacturers for raw materials and components used in its Inspire system, as well as for the production and assembly of its products. Some suppliers act as sole providers for specific materials and components. The reliability and supply continuity of these sole suppliers and any other suppliers or third-party manufacturers might be compromised.

Estimate Trends

Positive estimate revisions for 2024 have been noticeable for Inspire Medical. Over the past 90 days, the Zacks Consensus Estimate for its loss per share has narrowed from 70 cents to 38 cents.

The Zacks Consensus Estimate for the company’s first-quarter 2024 revenues stands at $161.3 million, reflecting a 26.1% increase from the comparative figure reported in the same quarter of the previous year.

Key Selections

Some top-ranking stocks within the broader medical domain include DaVita Inc. DVA, Cardinal Health, Inc. CAH, and Cencora, Inc. COR.

DaVita, holding a Zacks Rank #1 (Strong Buy), boasts an estimated long-term growth rate of 12.1%. DaVita has continually surpassed earnings expectations over the past four quarters, with an average surprise of 35.6%. The share price of DaVita has surged by 75.2% compared to the industry’s 23.8% uptick in the last year.

Cardinal Health, presently with a Zacks Rank of 2 (Buy), anticipates a long-term growth rate of 14.2%. The company has consistently surpassed earnings estimates over the past four quarters, with the average being 15.6%. Cardinal Health’s shares have climbed 55.5%, topping the industry’s 15.6% rise over the past year.

Cencora, currently holding a Zacks Rank of 2, projects an estimated long-term growth rate of 9.8%. Cencora has exceeded earnings forecasts in each of the past four quarters, with an average surprise of 6.7%. The share price of Cencora has surged by 54.8%, surpassing the industry’s 6.1% growth over the last year.

Infrastructure Stock Boom to Sweep America

A colossal initiative to revamp the deteriorating U.S. infrastructure is on the horizon. It’s a bipartisan effort, urgent and inevitable. Trillions of dollars will be channeled into this cause, paving the way for immense fortunes to be made.

The only query is, “Will you identify the right stocks early on when their growth potential is at its peak?”

Zacks has unveiled a Special Report to help you do just that, and it’s available for free today. Uncover 5 exceptional companies poised to reap substantial benefits from the extensive construction and renovation of roads, bridges, buildings, as well as the transformation of cargo hauling and energy on a monumental scale.

Download FREE: How To Profit From Trillions On Spending For Infrastructure >>

DaVita Inc. (DVA) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

Cencora, Inc. (COR) : Free Stock Analysis Report

Inspire Medical Systems, Inc. (INSP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.